Aaron Hawkins/iStock via Getty Images

Investment Thesis

Snowflake (NYSE:SNOW) continues to be richly priced for what it offers investors. I believe that Snowflake at 45x forward free cash flow is already pricing in the best-case scenario.

Or perhaps, better put, I can understand why investors that are long this stock may continue to buy more of a stock with such an alluring narrative on Wall Street, but for new investors looking at the stock with fresh new capital, I do not see the appeal.

Simply put, Snowflake isn't worth its premium.

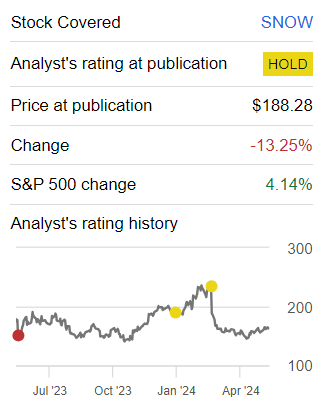

Rapid Recap

In February, I titled my analysis of Snowflake as Don't Buy This Dip.

Author's work on SNOW

Since that time, this stock has moved lower and has underperformed a very strong tech-led market that practically any boat got lifted. And now, as we look ahead, I'm once again of the same opinion that this stock isn't worth chasing.

Snowflake's Near-term Prospects

Snowflake is a cloud-based data platform that allows businesses to store, manage, and analyze large amounts of data efficiently.

It combines the capabilities of data warehousing, data lakes, and big data platforms, enabling companies to consolidate their data into a single, scalable system. Snowflake's platform supports advanced data analytics and AI, helping businesses gain valuable insights from their data and make better decisions. Its user-friendly interface and powerful tools make it easy for organizations to share and collaborate on data securely.

The bull case for Snowflake is that under the new CEO, Sridhar Ramaswamy, Snowflake has been focusing on customer-centric strategies.

The company's integration of AI into its platform is a significant growth catalyst, enabling broader access to enterprise data and enhancing capabilities across data management, collaboration, and applications. This has already led to substantial increases in usage among some of Snowflake’s largest customers. The financial performance in Q1 reflects this narrative, with its remaining performance obligations up 46% y/y.

However, Snowflake faces several headwinds too. One significant issue is the increasing costs associated with AI initiatives, particularly GPU-related expenses. While investing in AI is crucial for staying competitive, it impacts Snowflake’s profit margins (a topic we'll address soon).

This trend is expected to continue; Snowflake seeks to invest further in AI capabilities, including the acquisition of TruEra’s technology assets. These costs, while necessary for long-term competitiveness, place pressure on underlying free cash flow margins.

Another challenge for Snowflake is its highly contentious consumption model. I've discussed this numerous times in the past, so I won't repeat it now. But the short of it is this, consumption models work wonders when they work, but when there's a speed bump, it can truly change the operating leverage of the business.

For instance, during the earnings call, it was noted that there was a noticeable moderation in April, which Snowflake attributes to seasonal factors like holidays in Europe.

Next, see if you spot a pattern in the following illustrations:

SNOW Q1 2024 SNOW Q2 2024 SNOW Q3 2024 SNOW Q4 2024 SNOW Q4 2024

Above we see that with time, Snowflake's total customer growth rates, or its customer adoption curve, is flattening out. For me, that's a red flag and I wouldn't even consider anything further.

Nevertheless, let's press ahead to discuss its financials.

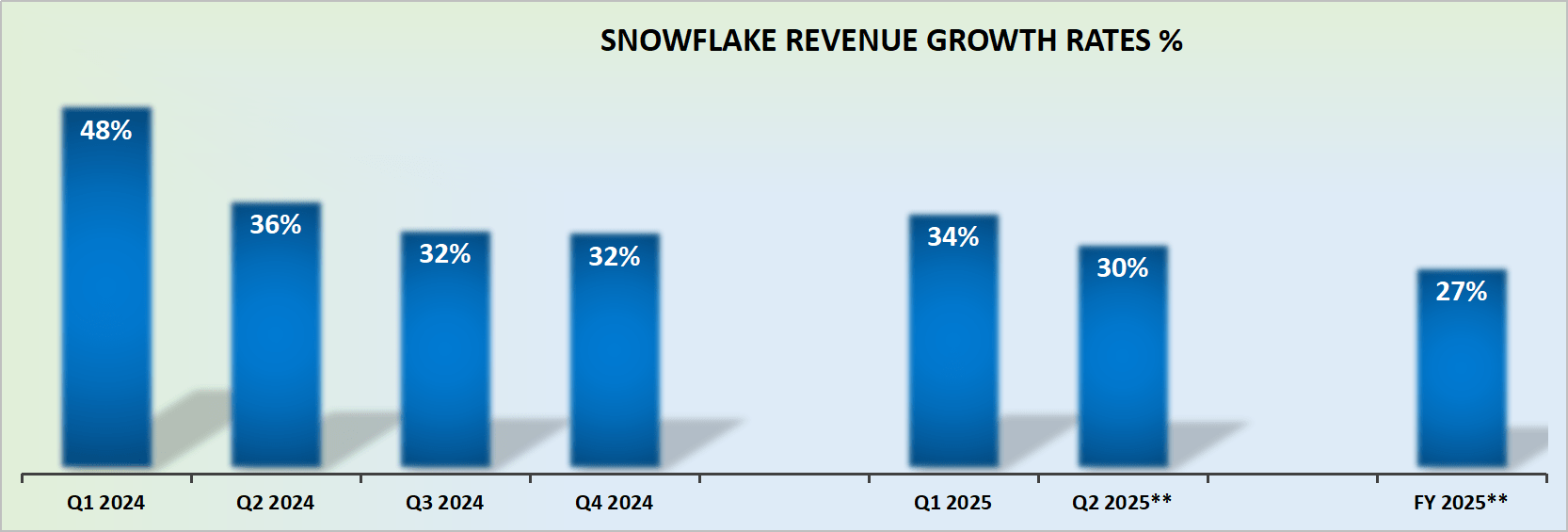

Revenue Growth Rates Point to Around 27% CAGR

SNOW revenue growth rates

Snowflake is presumed to be one of those companies that is always lowballing their revenues to allow for an easy beat later when the quarter gets reported. After all, that's the game, right?

And yet, the fact of the matter is that for all its future narrative, the business is delivering mid-30s% growth rates. That's clearly a meaningful growth rate, but hardly something that is commensurate with the praise that Snowflake gets.

Now, consider what I wrote about Snowflake last time:

Snowflake put out guidance that points towards mid-20s% growth rates. Naturally, the company apparently is lowballing estimates to allow the new CEO to come in and stamp his mark on the company. I get that.

Here's the thing, along the lines of my contention above, now, for the quarter ahead, Snowflake is guiding for approximately 30% y/y revenue growth rates. These growth rates may come in stronger than this, but I've already factored in 300 basis points higher than the high end of its guidance.

Essentially, Snowflake's revenue growth rates are slowly, but steadily, decelerating.

Now, this is where matters become more complex. It's certainly possible for Snowflake to continue delivering 30% CAGR for a considerable number of years. That being said, I believe that Snowflake must deliver a 30% CAGR simply to match investors' expectations. Meaning that this is what's being priced in already, as we'll discuss next.

SNOW Stock Valuation -- 45x Forward Free Cash Flow

Previously, I demonstrated how Snowflake's customer adoption is moderating. That's an important insight. Because Snowflake is taking significant sums of cash upfront from customers as deferred revenues, making its free cash flows look mighty strong. Although, a few of its customers do now pay in arrears.

To my point, those free cash flows will struggle to continue growing at a rapid pace if you are just hiking prices on your customers. No customer wants to see their bill rapidly increasing every year for consumption. At some point, even its deep-pocketed Fortune 2000 customers will push back. That's just common sense. It's the whole argument of binge-watching on Netflix (NFLX) versus pay-per-view. What offering has more success?

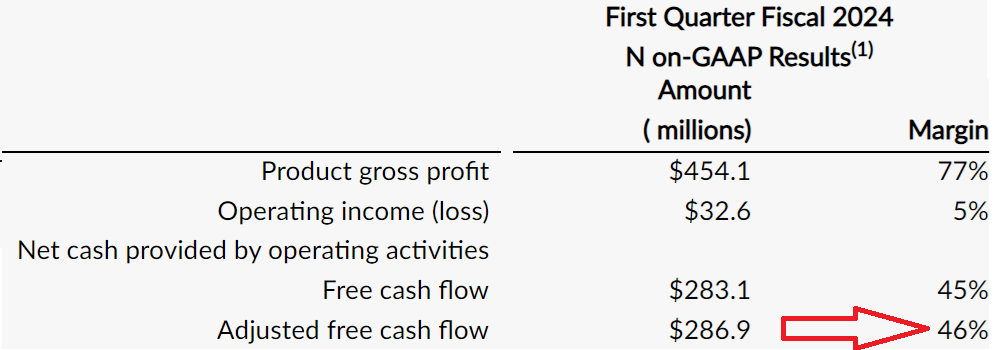

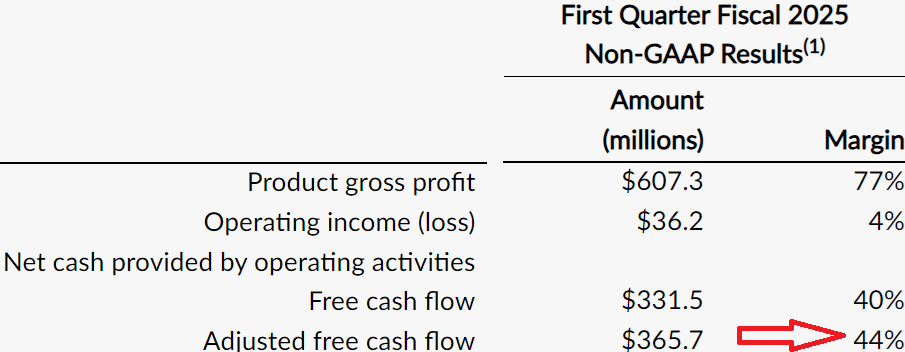

Along these lines, consider the following:

SNOW Q1 2024

What you see here is that Snowflake's free cash flow margin stood at 46% in fiscal Q1 of the prior year.

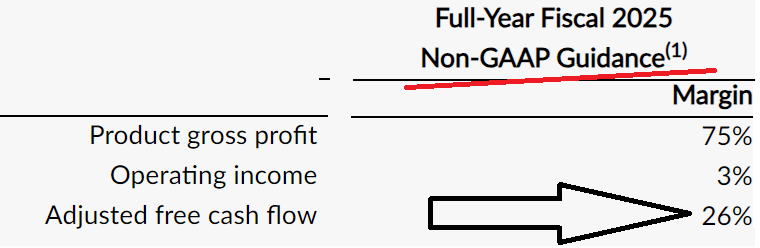

SNOW Q1 2024

And if you compare this with its most recently reported results, its free cash flow margin has compressed by 200 basis points y/y.

All in all, this reinforces my argument. You can only squeeze your customers so far, for so long. At some point, your customers start to look for alternatives.

With that in mind, now consider Snowflake's full-year fiscal 2025 guidance below:

SNOW Q1 2025

Even if Snowflake's adjusted free cash flow margin figure gets upward revised throughout the year, it's unlikely to surpass the 29% free cash flow margin that Snowflake reported last fiscal year.

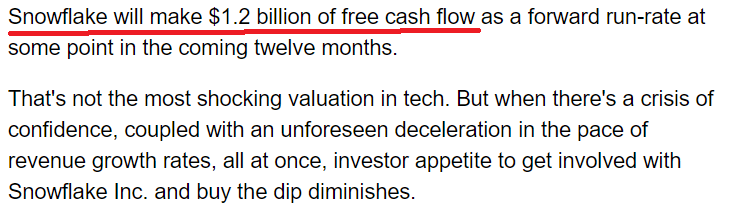

In my previous analysis, I said:

Author's work on SNOW

I continue to believe that Snowflake's fiscal 2025 will deliver around $1.2 billion of free cash flow this year. This would be a 50% increase compared with the same period a year. This means that Snowflake is already maximizing its free cash flows as much as possible, given that its free cash flows are outpacing its topline growth.

All in all, I find that paying 45x this year's free cash flow for Snowflake, while it's facing substantial topline deceleration, to be a price that doesn't leave me with any room for error. Therefore, I'll pass.

The Bottom Line

I’m giving Snowflake’s stock a pass because, despite its promising technology and customer-centric strategies, its financials just don’t justify the high price.

The company is trading at 45x forward free cash flow, which already assumes the best-case scenario for its growth.

Although Snowflake has seen significant increases in usage and remains a strong player in the tech market, its growth rates are decelerating, and customer adoption is flattening out.

Additionally, the increasing costs associated with AI initiatives are pressuring its free cash flow margins.

Given these factors, along with the fact that its free cash flow margins are compressing, I don’t see enough upside. Therefore, I'll pass on SNOW.

Strong Investment Potential

My Marketplace highlights a portfolio of undervalued investment opportunities - stocks with rapid growth potential, driven by top quality management, while these stocks are cheaply valued.

I follow countless companies and select for you the most attractive investments. I do all the work of picking the most attractive stocks.

Investing Made EASY

As an experienced professional, I highlight the best stocks to grow your savings: stocks that deliver strong gains.

- Deep Value Returns' Marketplace continues to rapidly grow.

- Check out members' reviews.

- High-quality, actionable insightful stock picks.

- The place where value is everything.