Sundry Photography

Q3 Earnings Were Weak

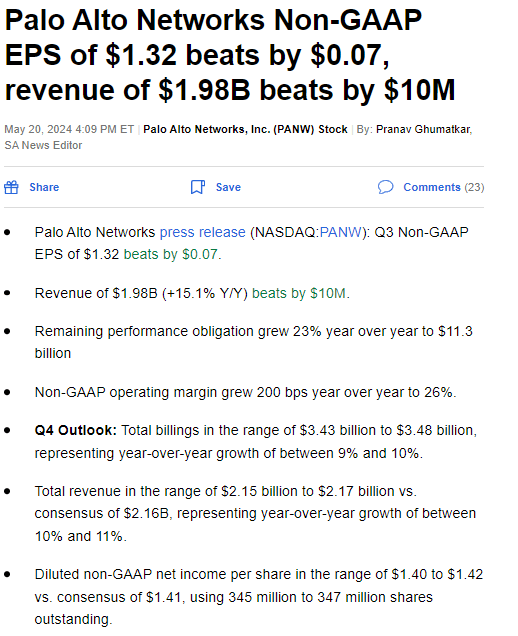

Palo Alto Networks (NASDAQ:PANW) reported its Q3 results on May 20, 2024. Revenue beat expectations by $10 million and EPS was a beat by $0.07. The company delivered revenue of $1.98 billion (+15% YoY), and non-GAAP EPS of $1.32.

However, the market reacted very negatively to the billings metric. In Q3, billings grew only 3% YoY, and guidance for Q4 came in below expectations (9% - 10% YoY). RPO showed improvement from the last quarter and increased 23% to $11.3 billion. See the Q3 results below:

PANW Q3 results (Seeking Alpha)

Our goal for this article is not to speculate on the company's short-term results. Instead, we want to share our broader concerns about the company's platformization strategy and its ability to respond effectively to the changing cybersecurity landscape. In an increasingly competitive and disruptive market environment, we believe Palo Alto Networks is facing competitive challenges from both established players and emerging disruptors. Our long-term view for the company is concerning.

Cybersecurity Platformization is Likely Mission Impossible

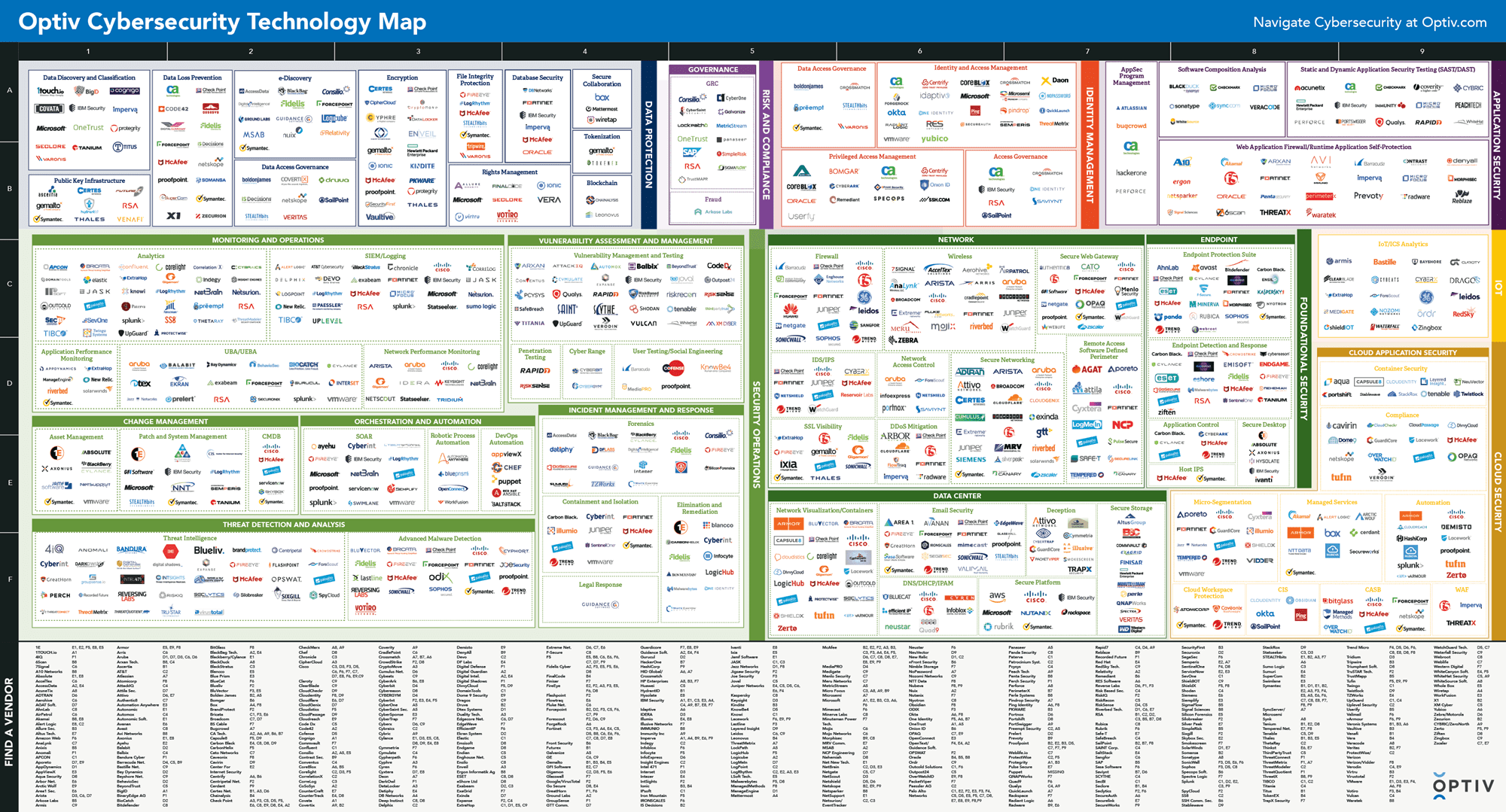

Palo Alto Networks continues to push its "platformization" strategy, saying that a consolidated and simplified environment will lead to a more secure environment (vs having best of breed point solutions). The company has a blog post on the topic, defending its approach. However, we have doubts about this strategy as this approach has been tested many times in the past without any success. The reason is that the cybersecurity ecosystem is too big and diverse for any single vendor to suggest a consolidation approach (see below).

Cybersecurity Technology Map (Optiv)

Palo Alto only covers a few of the categories. Therefore, we find it unrealistic to push for platformization-type strategies in such a complex and dynamic ecosystem. Even if Palo Alto Networks were to acquire or develop capabilities across the entire spectrum, customers would likely prefer best-of-breed solutions from specialized vendors in each category, in our opinion.

Customers Prioritize Risk Mitigation over Simplicity in their Security Investments

The cybersecurity market is one of the most dynamic in the IT industry, with bad actors continuously evolving new tactics, strategies, and tools. In response, customers try to mitigate these emerging threats by adapting their defense strategies and invest in specialized security solutions. Each industry faces unique threat vectors and regulatory requirements, which requires a risk-driven approach to security. Relying on a one-size-fits-all platform from a single vendor can create critical security gaps.

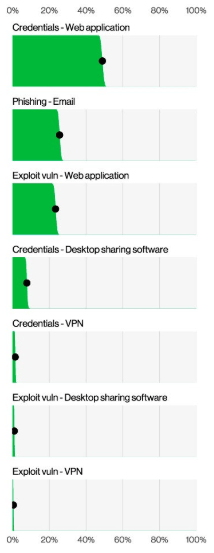

For instance, currently the most trending issue in cybersecurity is the surge in identity attacks, (as highlighted by multiple sources including Crowdstrike, Cyberark and Proofpoint). Verizon 2024 Data Breach research shows that 80% of breaches start with compromised identities (see below)

Top attack vectors (Verizon Data Brach Report)

Gartner states that the customer focus is currently shifting from network security towards Identity and Access Management (IAM) solutions. As a result, customers will look for specialized IAM vendors to mitigate the increased identity risk. The point we are making is that cybersecurity spending is driven primarily by evolving risk factors, rather than the need for simplicity or cost savings. We believe Palo Alto's platformization approach is not aligned with the market realities.

Palo Alto Is Facing Fierce Competition

Palo Alto assumes that AI will increase cyber-attack activity and fuel cybersecurity spending. This is a valid observation, but the reality is that AI is not only disrupting customers, but also the cybersecurity market itself. The SaaS players from adjacent markets are entering the cyberspace rapidly due to its growth potential, while new AI startups are further fragmenting the market. Palo Alto already faces competition from rivals like CrowdStrike (CRWD), Zscaler (ZS), and Cloudflare (NET), which have way better strategies in our view, and market positioning (all growing revenue at 30%+). The other concern for Palo Alto Networks is, of course, the hyperscalers, which are rapidly expanding their cybersecurity offerings. They have vast AI capabilities and are developing comprehensive security solutions as part of their cloud platforms. If anyone can push platformization, it's the hyperscalers, not Palo Alto Networks, we think.

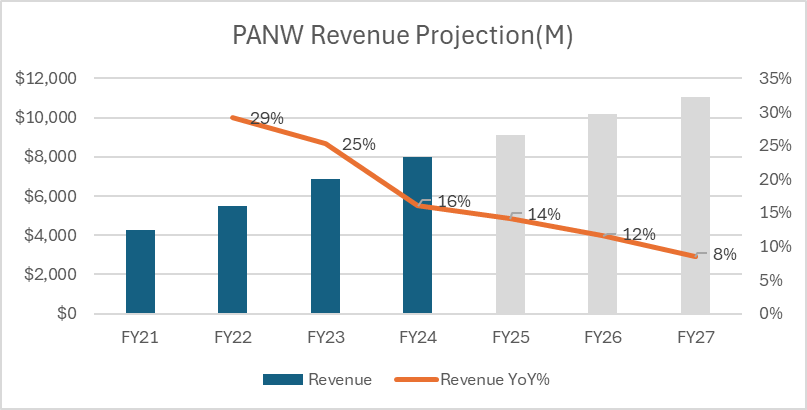

The cybersecurity market is getting more sophisticated and industrialized, and as new security companies emerge, the landscape becomes increasingly crowded. Therefore, we expect market fragmentation to intensify, rather than consolidate. We believe that Palo Alto’s response to these market changes is misguided and will have consequences for its future growth and market position. As a result, we predict that Palo Alto’s revenue growth will continue to slow, and fall below 10% in the next few years (see below).

PANW Revenue Projection (Author)

Valuation Too High

Despite the market risks and decelerating growth, Palo Alto's valuation remains very high. Interestingly, it appears the market believes in the company’s “platformization” story. The company trades at a premium sales multiple, despite growing in the mid-teens and facing billings deceleration.

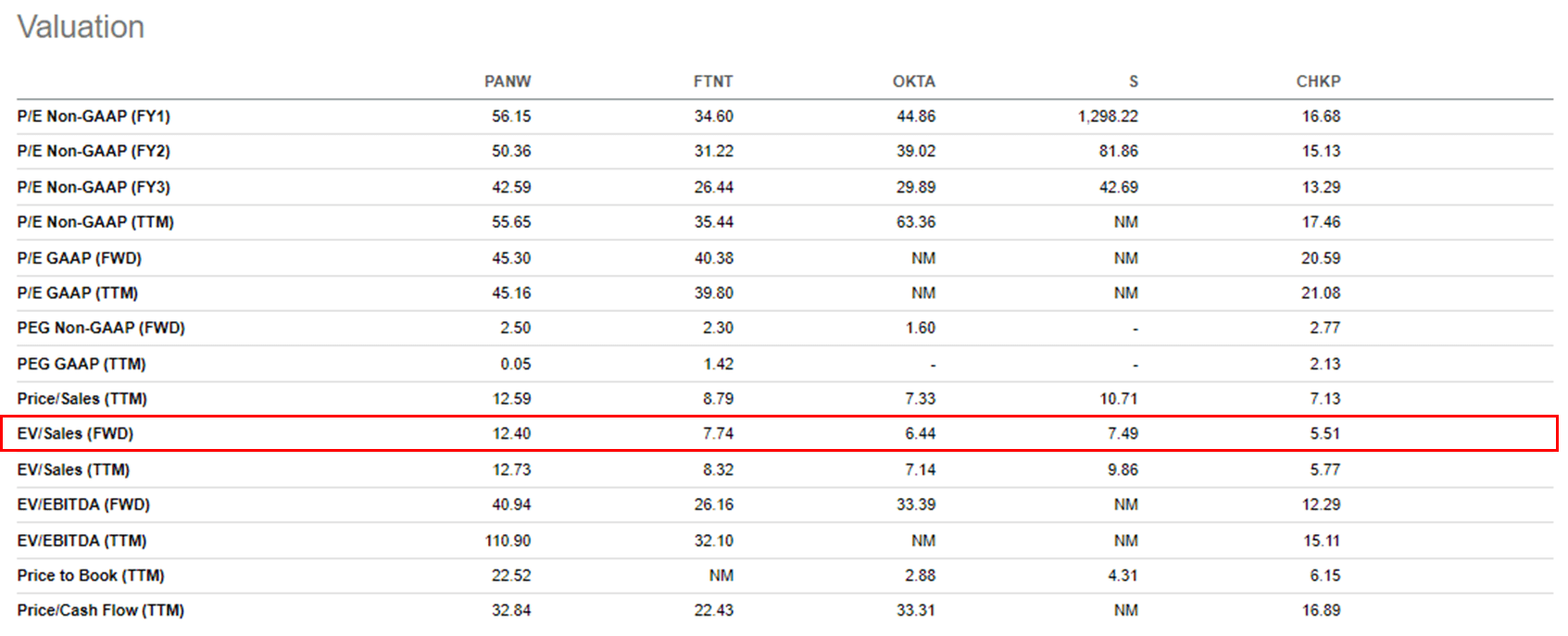

With low growth rates and significant competitive threats, we don't think that Palo Alto deserves such a high valuation. The company's forward P/S ratio is around 13, significantly higher than its low-growth cyber peers (see below)

Valuation Comparisons (Seeking Alpha)

These companies above have growth rates between 5% to 20%, but their sales multiples are significantly lower than Palo Alto. We have excluded high-growth companies such as CRWD, ZS and NET from the comparison.

The 13x fwd P/S valuation is difficult to justify given the company's slowing growth and the intensifying competition it faces. Our view is that the company should be valued as a low-growth cybersecurity company in alignment with its low-growth industry peers. Even if we apply an above average multiple of 9x to the FY25 revenue, we get a 2025 price target of $251. This represents a 19% downside potential from the current price.

Conclusion

Palo Alto’s decelerating growth rate is concerning, but its platformization strategy is a red flag for us. When we look at the big picture, we see the company is losing its strategic direction, competitive advantages, and struggling to respond effectively to the cybersecurity market changes. The market still believes it will succeed with its platformization strategy, but we have serious doubts.

When we value the company, we think there are many negatives. The company faces high market risks, growth deceleration, and a premium valuation compared to its peers.

In conclusion, Palo Alto Networks is overpriced. We issue a Sell rating.