Wirestock/iStock Editorial via Getty Images

Above: Sony Pictures, massive potential to expand IP blending its TV and film base with scale up matching close to Disney.

If you look at the present candidates and would be contenders in the Paramount (PARA) free for all dead end, it is not hard to conclude that logic must bring you to a close for Sony (NYSE:SONY). As we have noted, the price might need a bit sweetening above the $26 on the table to put a smile button on everyone's chest, including Shari, and all holders of all classes. But the nice kicker we see in such a potential deal would be the change to a cash/stock deal using SONY shares as currency. What that would do is give holders a stake in the post deal SONY prospects.

We think CNBC's David Faber may be jumping the gun by concluding that SONY/Apollo might be getting second thoughts about the PARA deal. One can smell cold feet when deal pursuit suddenly attracts a school of feeding sharks. That usually means the premium could skyrocket. So it becomes a thanks, but no, thanks response from early bidders. SONY will stay in the game as long as no one else raises a hand.

google

Otherwise, holders face a take the money and run scenario which if all cash limits, a premium and gives zero in the forward potential of the deal. So many holders are underwater at this stage that it would take a quantum leap in the best-case premium to match a smart cash/stock SONY forward return scenario.

SONY: The SONY business model has worked to date and will gain considerable depth and reach with the PARA

The SONY Pictures unit of the group this year to date has launched a raid of recent bombs at the box office. But historically, its Columbia track record has produced many hits. Yet to Q3 its film revenue hit $2.47b showed a rise of 57% yoy. This opens two key points: One, the size and scope of SONY can bear the inevitable flops that come with the territory for all studies and two, the clear need for film and TV IP of the quality PARA could contribute to merged depth of offerings to buyers. In other words, a deeply enriched IP if PARA is blended into SONY reinforces the strategy of "content only:" bypassing streaming but selling product to all comers.

The SONY IP treasure chest now is competitive. Bear In mind, SONY bought Columbia Pictures merged with Screen Gems TV IP and its big music division in 1989, bringing legacy IP as well as setting the stage for expansion by dipping into the parent's mighty bankroll:

Peers with heavy steaming production needs will be bound by financial discipline, going forward. Without a steaming drain, SONY can make more content, they can innovate. They might really consider spinning off the PARA streaming service and just be a supplier. They would avoid the death spiral of the streamers for years. And just keep spinning out product.

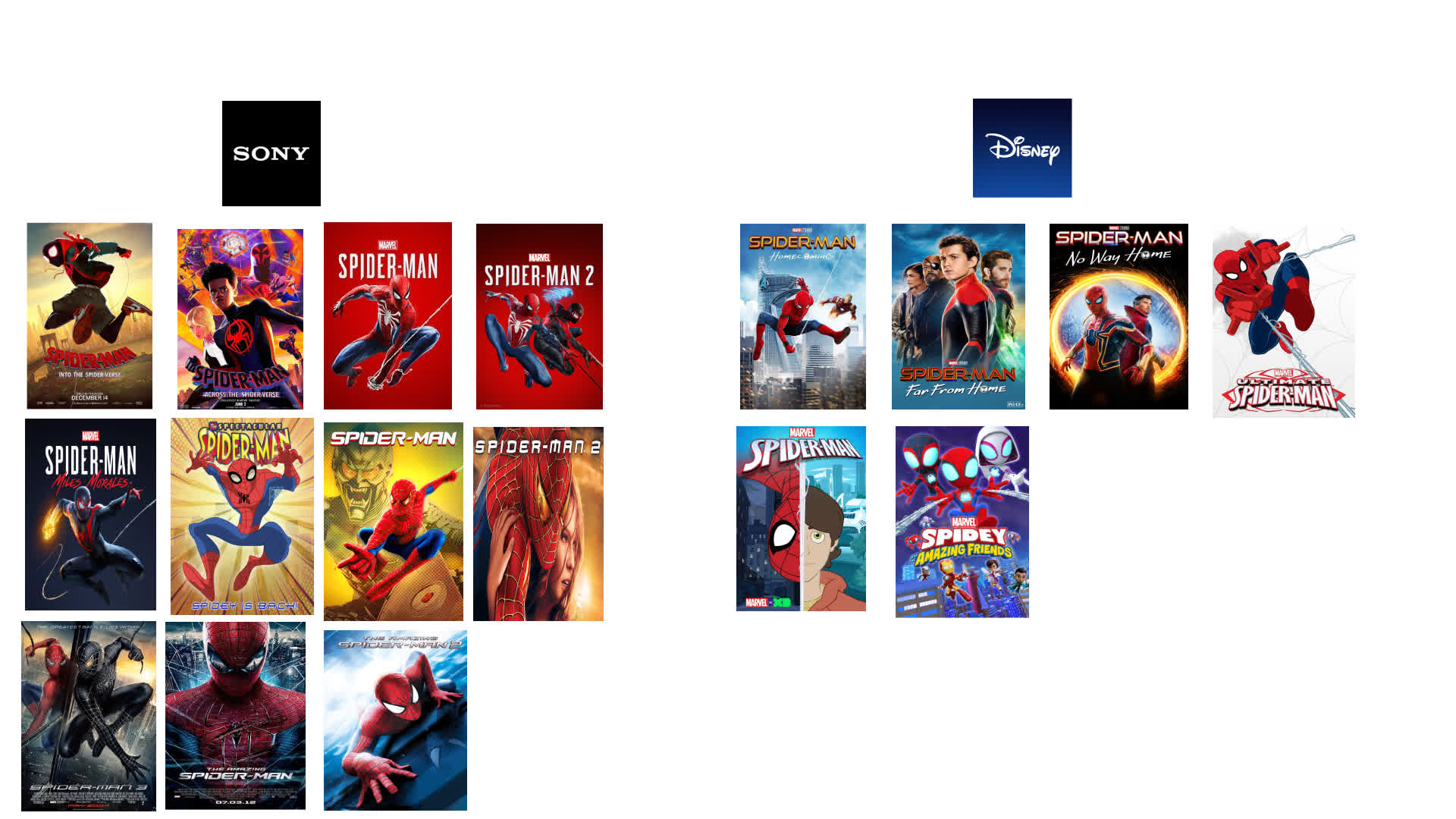

SONY IP is viable: but could use scale: Just a few, Breaking Bad, Dragon Tattoo, The Karate Kid, Spider-Man universe, Charlie's Angels, Ghostbusters, Men In Black, Rambo, Smurfs, and dozens of others, not to mention the Flintstones and legacy content from the old Columbia like On The Waterfront, Lost Horizons, Mr. Smith Goes to Washington and many intergenerational beloved movies.

google

Above: Comparison between SONY Spider-Man output vs Disney

The existing scale of SONY compared with many peers from the get-go makes its currency a great starting point for holders post cash out to which the PARA treasury will bring heft:

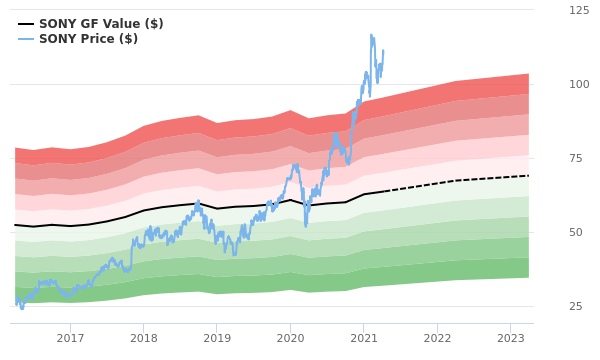

A presently flat SONY will resume growth post PARA

Price at writing: $80

Market Cap:$98.41b

TTM;

Revenue: $86b

Operating income: $7.49b

Basic EPS: $5.21

EBITDA: $15.4b

Payout ratio: 10.6%

Revenue 5 year growth: 1,82.95% vs. sector median: 1.20%. Yes, kudos to PlayStation, of course.

But the pictures unit did only $2.47b in revenue for 2023, a 57% yoy rise. The takeaway here: SONY needs PARA IP if it intends to keep the streaming business post deal. If not, its IP combined with PARA does make it a formidable arms dealer operation. It can sell or license IP new or legacy at will without bringing in the cash burn that has now become the signature of streaming. The PARA studio production capacity may be moot in the sense that their studio, fully financed, can make more movies in a market where total releases will shirk dramatically over the next five years, according to the industry's gossip site, The Ankler.

SONY could make one phone call post closing, to Skydance: You still want the PARA studio? Here's the price and it's yours. The key here is that SONY goes into battle with more weapons than anyone save Disney. Some weapons even better: Games, PlayStation, Music, consumer products and pictures.

Risks

SONY's financial picture may not satisfy PARA holders as it shows a 0.66, current ratio, giving a few grey hairs to bankers looking to do a SONY/PARA deal now. Their cash pile is still up around $184b, with long-term debt lingering around $31b. But the total valuation runs above $100b. That is why I believe the numbers dictate a cash/stock deal. SONY's immediate outlook indicates that 2024 revenues will be flat with unimpressive earnings. Also leaning to the bear side is what if recession changes that could damage growth in its consumer sections?

The takeaway of this endgame idea;

Yet, there is little question that SONY could breeze through a financing for the deal at a price we see as under $30. The cash component that will work IMHO would be ~$20 with the rest in Sony shares. And here's the final question to all holders:

1. Shari and all her holders get what Skydance offered, perhaps with a little spike.

2. Common holders get a cash dominant pay off and wind up with SONY shares. The alternative will be the continuing charade of a dead-end street with PARA stock twisting in the wind between nickel and dime upside based on earnings, or worsening financial risk.

The new management troika appointed by Shari are competent, but not magicians.

Close the SONY deal and end the madness.

The only magic forward is a cash/stock deal that can close with giving holders a good shot at a SONY future.

The House Edge is widely recognized as the only marketplace service on the casino/gaming/online sports betting sectors, researched, written and available to SA readers by Howard Jay Klein, a 30 year c-suite veteran of the gaming industry. His inside out information and on the ground know how benefits from this unique perspective and his network of friends, former associates and colleagues in the industry contribute to a viewpoint has consistently produced superior returns. The House Edge consistently outperforms many standard analyst guidance with top returns.

According to TipRanks, Klein rates among the top 100 gaming analysts out of a global total of 10,000.