Fabian Gysel/iStock Unreleased via Getty Images

While the big aerospace and defense suppliers are part of my coverage, I am also covering smaller aerospace companies. Those that have been following my work know that some of the buy ratings on smaller companies such as Park Aerospace (PKE) and Astronics (ATRO) have performed rather well, although it should be noted that the former saw its outperformance evaporate earlier this year. It shows that smaller aerospace names do have significant potential, but at times might also start underperforming.

In this report, I am adding Innovative Solutions and Support, Inc. (NASDAQ:ISSC) to my coverage to assess whether this is the next aerospace play that could generate outsized returns.

What Does Innovative Solutions and Support Do?

Since this is the first time covering Innovative Solutions and Support, it is worth providing a brief overview of the company’s activities. IS&S presents itself as a leading systems integrator of cost-effective flight navigation systems and precision flight instrumentation equipment.

The company provides integrated flat panel display systems, the ThrustSense autothrottle, flight management systems, engine and fuel displays and air data products.

The company provides equipment for the Boeing 737 Classic, Boeing 757, Boeing 767, (K)DC-10, KC-46A and T-7A. This already gives the company exposure to commercial and defense platforms, while it also has exposure to Lockheed Martin’s C-130 and several general aviation platforms.

Innovative Solutions and Support

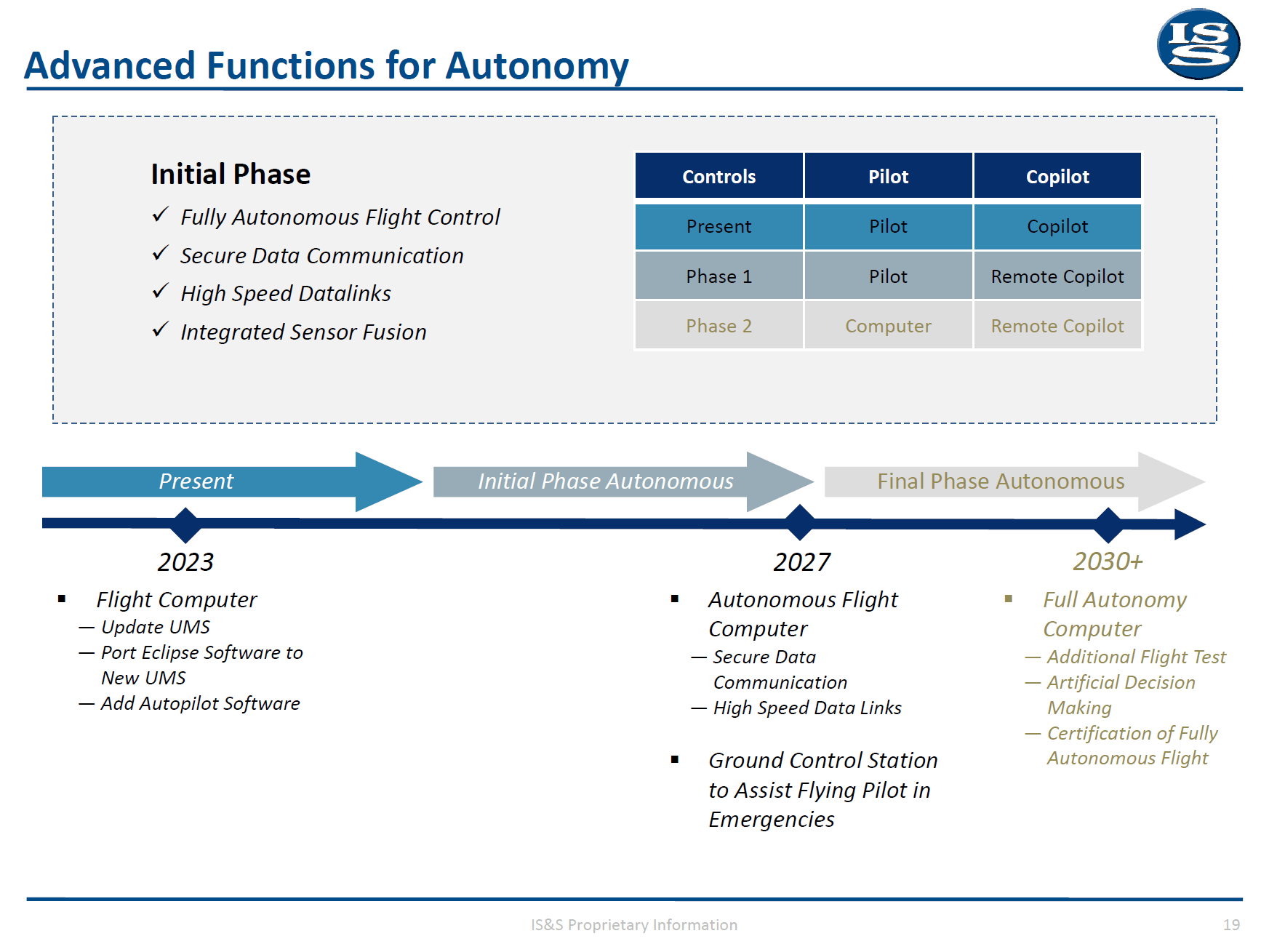

While IS&S appears to be a simple provider of avionics, the company is very ambitious, as its product line up should ultimately enable autonomous flight somewhere in the 2030s. Don’t expect to see autonomous flying Boeing jets by that time, but one can certainly expect strong progress on autonomous general aviation airplanes, and I believe there eventually could be some role for the company in the eVTOL market.

Innovative Solutions and Support

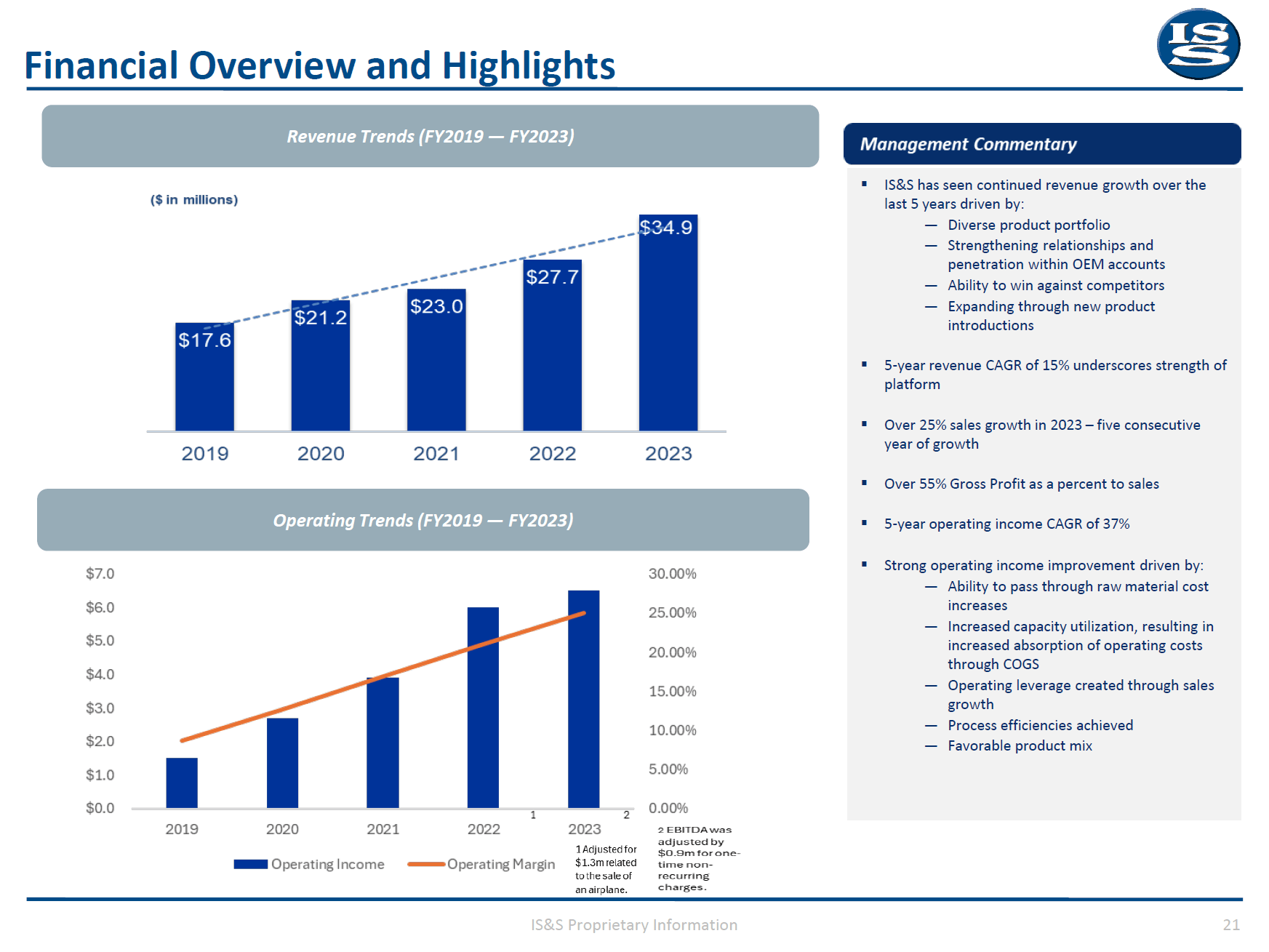

IS&S is not a huge company, and that is also evident from the $34.9 million in annual revenues. However, the company has a 15% CAGR on revenues and its operating income has been growing at 37%, pointing to strong operating margin improvement driven by the ability to pass through costs and economies of scale. In 2023, IS&S acquired several product lines from Honeywell (HON) Aerospace supporting military platforms as well as business aviation. While the integration of those product lines and the chain behind those product lines will pressure margins, it can be seen as a next step to bolster future growth.

Honeywell Transaction Pressures Q2 Earnings

Innovative Solutions and Support

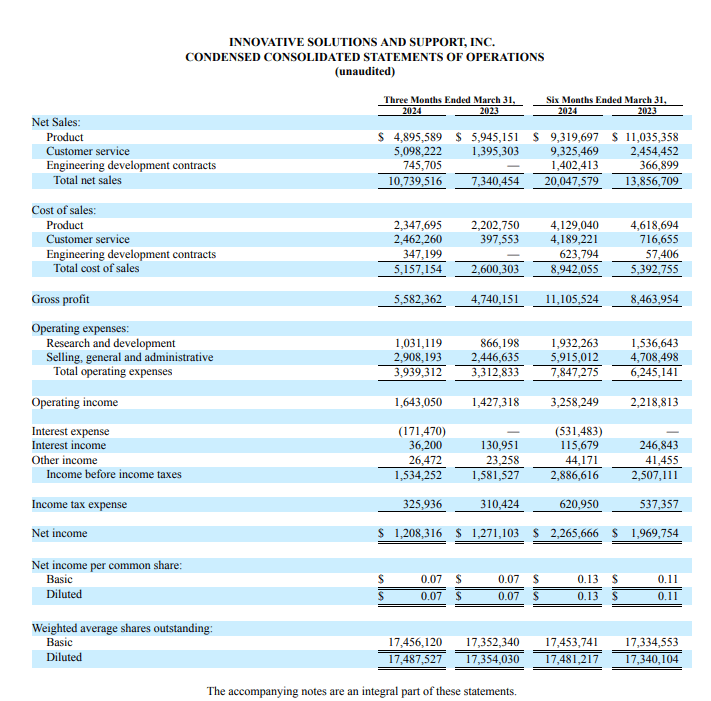

For the second quarter, revenues were up 46.3% with product sales down 17.7% on lower display retrofit shipments while customer services revenues increased $3.7 million reflecting the acquisition of the Honeywell product lines and engineering development contract revenues were $0.7 million. While I do believe that IS&S has an attractive line-up for the future, the results being driven by the Honeywell product line acquisitions do show that the business without the Honeywell product acquisitions would produce little to no growth. It indicates that the Honeywell product line acquisition is not a “nice to have” but absolutely necessary to continue growing revenues.

Gross margins during the quarter were 52% compared to 64.6% a year ago as the integration of the Honeywell product line is creating some inefficiency. Over time, as the Honeywell products get better integrated and IS&S brings more subassemblies in-house, thereby eliminating the excess cost in the process, we should see the margins go up.

However, as it stands now, we see revenues growing but due to margin erosion the translation to operating income is less favorable. SG&A grew by 18.9% due to higher sales and marketing costs as well as amortization expense in the amount of $268,500 as part of the Honeywell transaction. We also see that whatever limited operating income growth in the company had been further eroded by $171,470 in interest expenses as the company entered into a term loan in the amount of $20 million to finance the Honeywell transaction.

I wouldn’t say that the acquisition of the Honeywell product lines is not a success, it is far too early to draw any conclusions and having inefficiencies in the early stages is more rule than exception. However, the current results do show that an acquisition was necessary to bolster top-line growth, and it also shows the need for progress on integration of the product line, as the margins are under significant pressure at current standing.

Innovative Solutions and Support Stock Is A Strong Buy

The Aerospace Forum

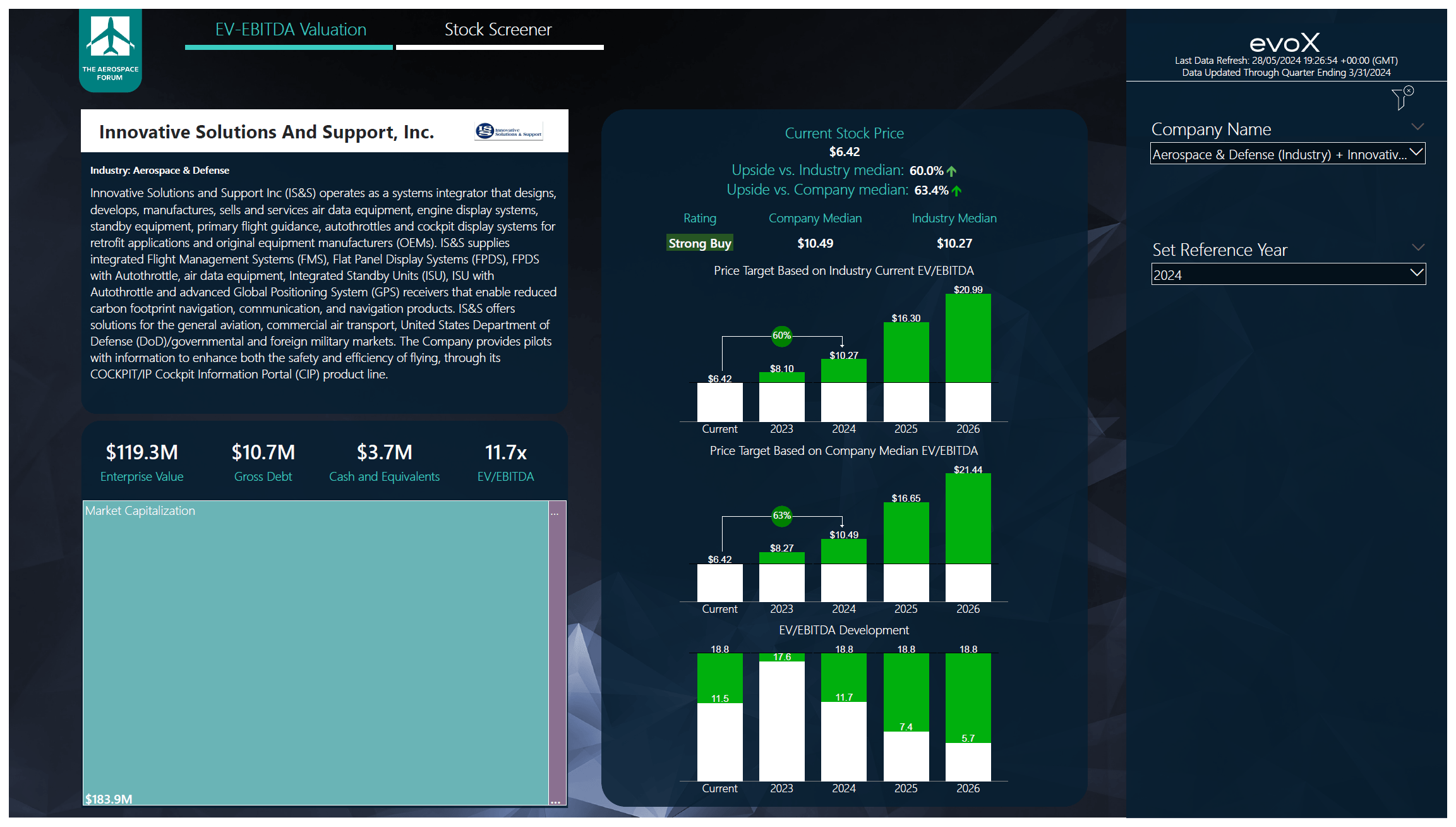

Innovative Solutions and Support does not have any Wall Street coverage, so any projections made can be extremely useful to investors as it generates some insight in a company that currently has little to no coverage. The company expects 75% EBITDA growth from the Honeywell product line adoption and while I think that is indeed achievable, I have delayed the 75% EBITDA growth in my model by one year to account for the integration delays and in-house manufacturing of the subassemblies which should truly bolster margins. When doing so, we still get to a very compelling 60-65 percent upside. As a result, I am marking the stock a Buy, noting that apart from the debt to finance the transaction, IS&S has no debt.

Conclusion: Innovative Solutions and Support Has Huge Potential

I believe that IS&S stock has huge potential. The company is currently experiencing some delays in integrating the Honeywell product line and that is pressuring margins, while interest expenses are also elevated. However, I do believe that as integration progresses and margins snap back, there is significant upside for Innovative Solutions and Support, Inc. stock. As a result, I am initiating coverage for Innovative Solutions and Support stock with a Strong Buy.

If you want full access to all our reports, data and investing ideas, join The Aerospace Forum, the #1 aerospace, defense and airline investment research service on Seeking Alpha, with access to evoX Data Analytics, our in-house developed data analytics platform.