benjaminalbiach

Warren Buffett has famously said that he wants for his assets to be put into the S&P 500 (SPY) after his passing, as he recognizes the power of compounding capital invested in the 500 biggest U.S. companies and the passive nature of this approach.

However, he and many investors don’t adopt that strategy, as getting the average market return is simply boring, for lack of a better word. The same goes for intelligence, beauty, performance, and income, as you’d be hard-pressed to find someone who relishes being average.

That’s what can make investing in individual stocks a potentially rewarding experience as investors seek to obtain better than average total returns, income, downside protection, or any combination thereof.

Great investment asset classes for the above attributes could be real estate and infrastructure, and while some investors may opt for buying properties on their own, it’s simply hard to obtain meaningful returns without taking on leverage, as SA Analyst Lyn Alden Schwartzer so aptly put it in a recent brilliant piece.

Plus, in this high interest rate environment, high mortgage rates break the investment thesis for many private real estate investors, particularly those who seek positive cash flow.

That’s why it pays to invest in publicly-traded companies, which carry institutional quality assets that enable them to obtain unsecured debt (vs secured mortgage debt) at favorable rates that individual investors simply can’t get.

This brings me to the following 2 dividend stocks that I consider to be cash cows, given their well-supported dividends with current yields ranging from 8-10%, with diversified business segments. Let’s explore what makes each of them attractive for income and value!

#1: Energy Transfer

Energy Transfer (ET) issues a Schedule K-1 and has become a sizable energy midstream company through recent acquisitions. It benefits from steady and growing cash flows, with 90% of earnings coming from fee-based contracts.

Its assets are well-balanced with equal weighting across oil, natural gas, and NGLS. This includes 125K miles of pipeline transport of natural gas, crude oil, and refined products, as well as storage terminals and gas processing facilities.

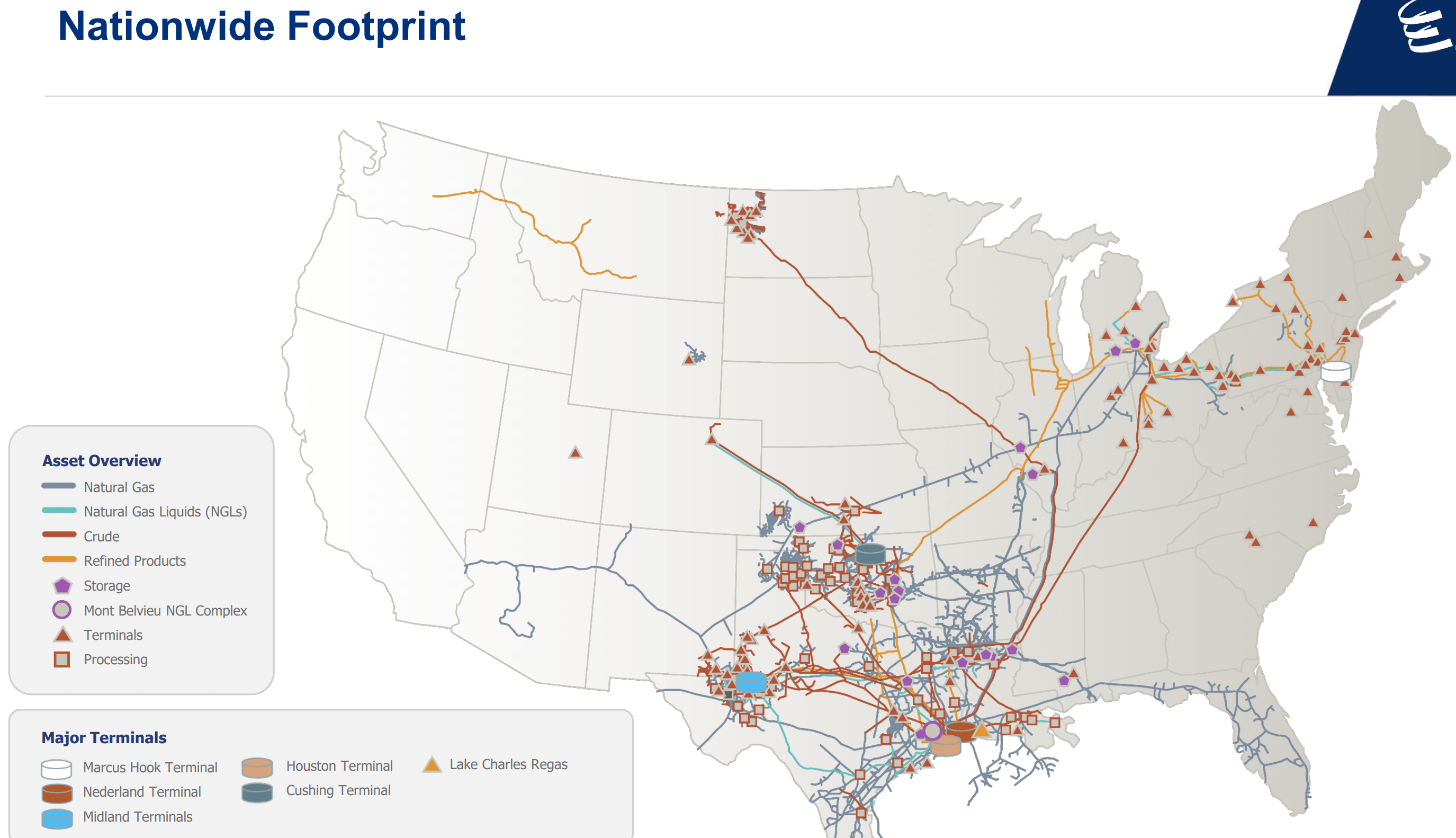

ET’s assets serve as critical links in the energy value chain, with heavy presence in the Permian Basin, as well as Marcellus in Appalachia and the Bakken shale formation in North Dakota. ET also has a significant export presence along the U.S Gulf Coast, as shown below.

Investor Presentation

ET has closed on a number of investments to bolster its presence in energy producing regions. This includes the acquisition of Enable Midstream in late 2021, which added complementary assets to ET’s pipeline system as well as increased gathering and processing footprint in the Mid-continent. Most recently, as shown below, ET acquired WTG, which further expands its natural gas presence in the Permian Basin and adds incremental revenue from downstream NGL transport and fractionation fees.

Investor Presentation

Meanwhile, ET continues to execute well operationally, with Adjusted EBITDA growing by 13% YoY to $3.9 billion in Q1 2024. This was supported by strength across the board, not least of which includes 44% YoY increase in crude oil transport volumes, setting a new partnership record. Moreover, NGL was also a growth driver for Energy Transfer with transport and export volumes up by 5% an 6%, respectively, and fractionation volumes up 11%.

Management is guiding for 11% Adjusted EBITDA growth this year to $15.2 billion at the midpoint of range. This is supported by contributions from recently acquired WTG Midstream, as well as other projects. Over the medium term, ET is expanding its NGL facility in Texas and debottlenecking of its Lone Star Express pipeline, which his expected to provide more than 90K barrels of incremental NGL capacity by 2026.

Importantly, S&P and Fitch both raised ET’s credit rating to BBB in 2023, and ET carries a safe amount of leverage with a net debt to TTM EBITDA ratio of 3.96, sitting below the 4.5x market that ratings agencies consider safe for midstream companies.

ET currently yields an appealing 7.8% and the distribution is well-covered by a 2.3x DCF/Distribution coverage ratio. ET raised the distribution by 3.3% this year, and targets 3-5% annual distribution growth going forward.

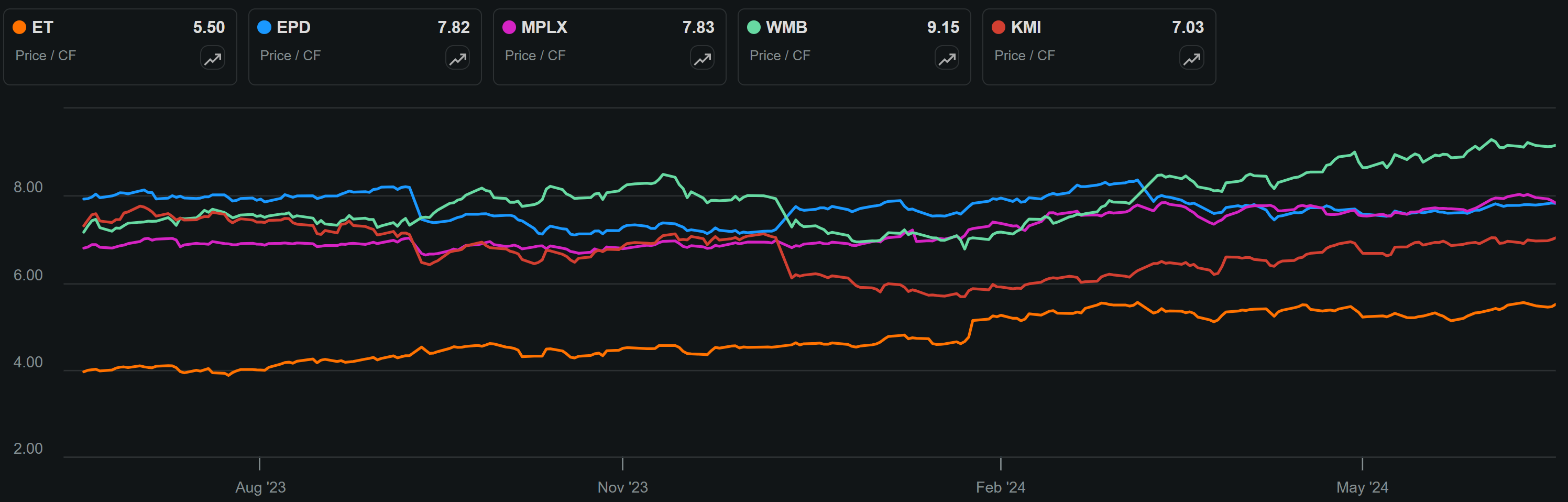

ET remains a bargain at the current price of $16.28 with a Price-to-Cash Flow of just 5.5x. As shown below, this sits well below the 7-9x range of peers Enterprise Products Partners (EPD), MPLX LP (MPLX), Williams Companies (WMB), and Kinder Morgan (KMI), as shown below.

ET vs Peers' P/CF (Seeking Alpha)

With a BBB investment grade credit rating, plenty of retained capital after paying the distribution, and a growing asset base, I believe ET is deserving of a higher valuation at least on par with that of Kinder Morgan, which carries a similar leverage profile. This could mean potential for market beating total returns, including the enticing 7.9% yield.

#2: Starwood Property Trust

Starwood Property Trust (STWD) is my second dividend cash cow pick given its 10% dividend yield that’s well-covered by cash flows. STWD is an externally managed commercial mortgage REIT that’s well-diversified, also carrying residential and infrastructure loans and physical real estate.

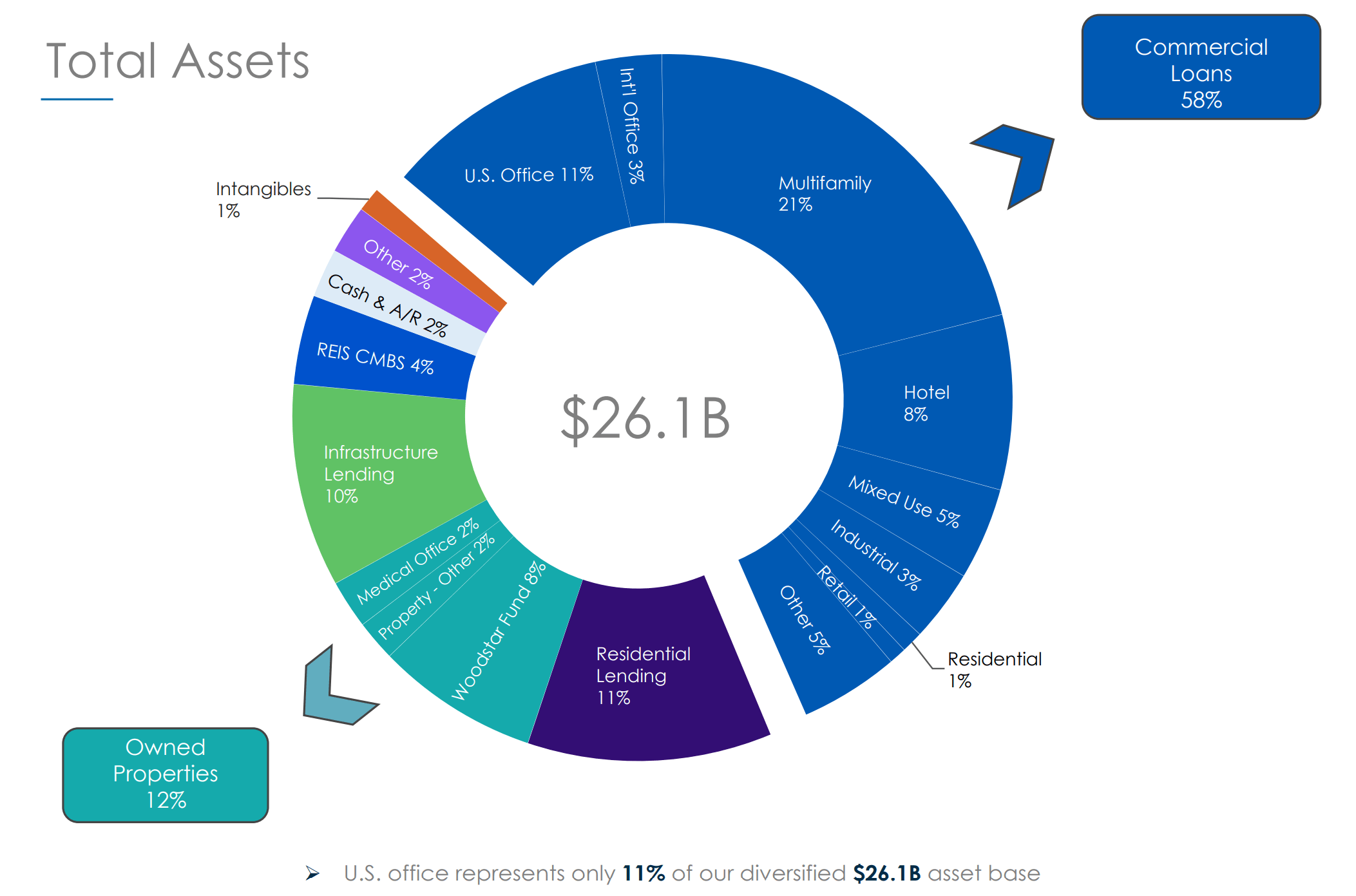

Since inception in 2009, STWD has deployed $97 billion of capital, and its current portfolio has a fair market value of $26.1 billion. Commercial loans make up 58% of the portfolio, with multifamily being the biggest segment, and another 12% of total assets are invested in physical properties. As shown below, U.S. office makes up just 11% of the portfolio total.

Investor Presentation

Meanwhile, STWD carries a conservatively run portfolio with 92% of the commercial lending portfolio being first mortgage loans, which sit at the top of the capital stack. It’s also benefitting from higher interest rates as 98% of the loan portfolio is floating rate.

With the Federal Reserve forecasting just 1 rate cut this year, STWD should continue to see solid earnings. This includes high distributable EPS of $0.59 achieved during Q1 2024, which is materially higher than that of pre-2022 before interest rates started rising. This resulted in a strong dividend coverage ratio of 123%.

Management is guiding for robust funding this year, given that the deal pipeline sits at the highest level in 2 years. This is supported by ample dry powder of $1.5 billion, driven in large part by $909M worth of loan repayments during Q1, far outpacing the $128M worth of loan funding during the same quarter.

STWD also carries a modest amount of leverage, with a debt-to-equity ratio of 2.3x. This is down from 2.5x from the end of 2023, supporting STWD’s BB credit rating, which compares favorably to peer Blackstone Mortgage Trust’s (BXMT) B+ rating due to higher leverage.

Lastly, STWD yields an appealing 10% and is attractive at the current price of $19.29, which equates to a Price-to-Undepreciated Book Value of 0.93x. With the current dividend yield, STWD could produce market-level returns and a potential return to 1.0x undepreciated book value could provide a total return kicker beyond that.

Investor Takeaway

Energy Transfer and Starwood Property Trust are two high-yield stocks that offer well-supported dividends and diversified business segments. ET, a sizable energy midstream company, benefits from steady and growing cash flows from fee-based contracts and a significant presence in key energy-producing regions, while maintaining a strong balance sheet and attractive valuation compared to peers.

STWD, a commercial mortgage REIT, boasts a diversified portfolio with a strong focus on first mortgage loans and benefits from the current rate environment, leading to robust earnings and dividend coverage. It also trades at a meaningful discount to book value. Both stocks present attractive value propositions for investors seeking reliable income and potential for market-beating total returns.

Gen Alpha Teams Up With Income Builder

Gen Alpha has teamed up with Hoya Capital to launch the premier income-focused investing service on Seeking Alpha. Members receive complete early access to our articles along with exclusive income-focused model portfolios and a comprehensive suite of tools and models to help build sustainable portfolio income targeting premium dividend yields of up to 10%.

Whether your focus is High Yield or Dividend Growth, we’ve got you covered with actionable investment research focusing on real income-producing asset classes that offer potential diversification, monthly income, capital appreciation, and inflation hedging. Start A Free 2-Week Trial Today!