Jeremy Poland

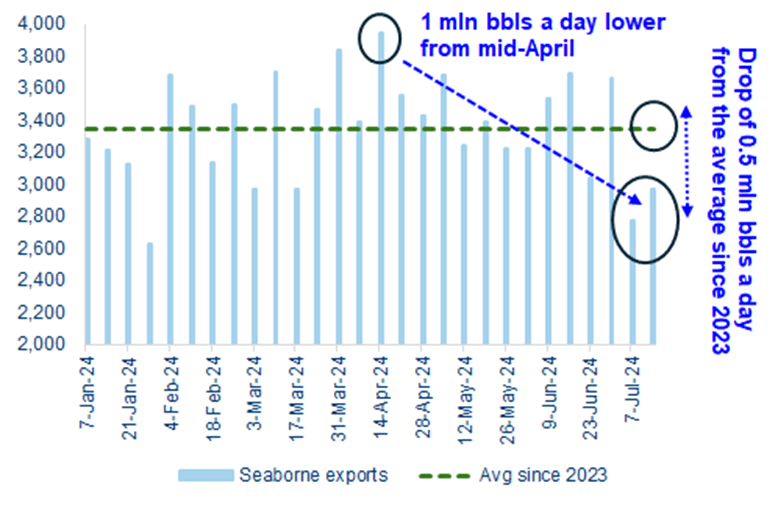

Notable drop in Russia’s crude oil production and exports since April

Russia’s production and exports have dropped since April on improving compliance with OPEC+ output quotas. There is also evidence on improvement in the country’s refinery run rates on an end to planned and emergency repairs. This is to translate into higher crude processing volumes. It is relevant to note that from end-May, Russia has aligned with OPEC+ partners in terms of restricting crude oil production vis-à-vis simply stipulating export targets.

During the first two weeks of July, Russia’s seaborne crude exports have dropped to the levels of 2.8-2.9 mln bbls a day. This is without any weather disruptions or reported maintenance activities at the ports. This indicates a major drop of up to 500 kb/d from the average since 2023 and is, in fact, one million barrels a day lower than nearly 4 mb/d shipped during the week of April 16th.

Russia’s Seaborne Crude Exports (kb/d)

Bloomberg

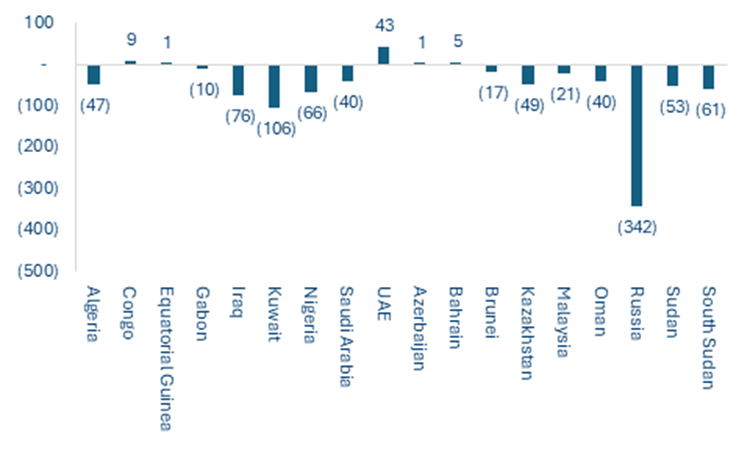

Russia leads higher compliance by OPEC+ in 2024

Russia’s lower exports have been surely contributed by its production decline in the last few months. As a matter of fact, Russia is on the forefront of the higher compliance exhibited by OPEC+ recently. During 2024, cumulative production of OPEC+ producers is down by around 865 kb/d. Out of this, more than a third, i.e., 350 b/d has come from Russia, followed by Kuwait at 106 kb/d and Iraq at 76 kb/d. Additional countries that have chipped-in include Algeria, Nigeria, and Kazakhstan.

OPEC+ Producers – Output changes during 2024

Bloomberg

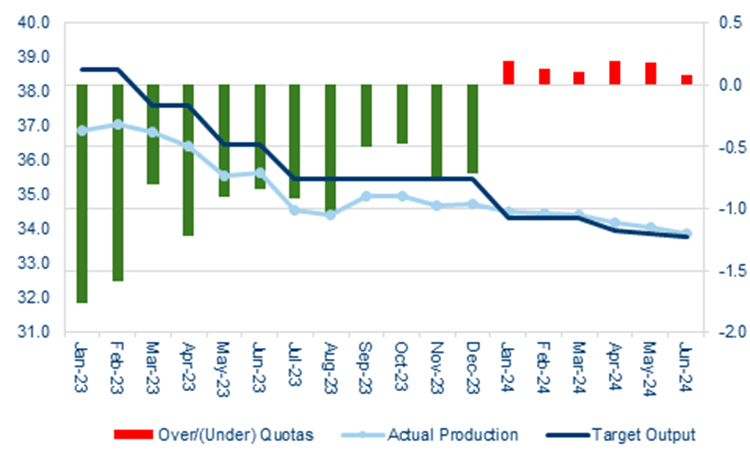

Steady compliance to quotas despite ongoing production target cuts

On an overall basis, OPEC+ countries continue to show high rates of compliance with their quotas. Literally speaking, during 2024, OPEC+ has produced on average 150-200 kb/d above quotas. This gives the illusion of lower compliance, as during 2022-23 the monthly underproduction ranged between 1-2 mb/d. The fact of the matter is that since Jan 2023, the cumulative production of OPEC+ has dropped by 3 mb/d emanating from a decline in the target of almost 5 mb/d. Saudi Arabia and Russia, for sure, have borne the brunt of the cuts. However, the alliance has managed to restrict leading producers such as the UAE and Nigeria from making output increases. Moreover, during the last two months, we see signs of production slowdown from Iran and Kazakhstan. Even though theoretically speaking, these two countries continue to “over-produce” against their quotas that have been reduced over time.

OPEC+ – Target, Production and Deviation from Quotas

Bloomberg

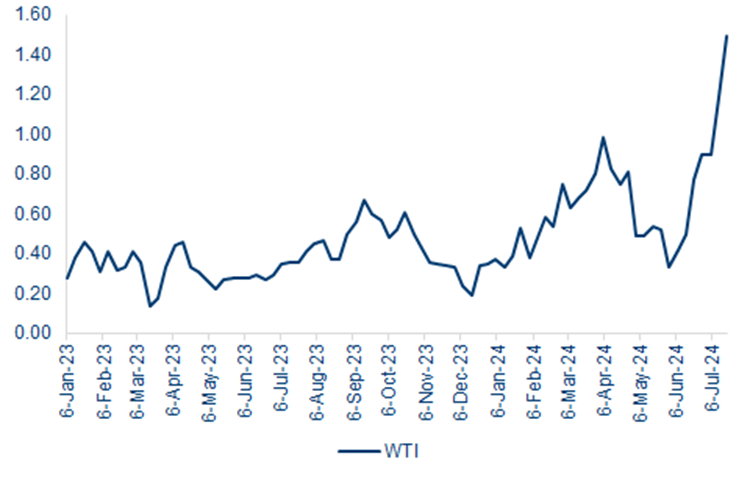

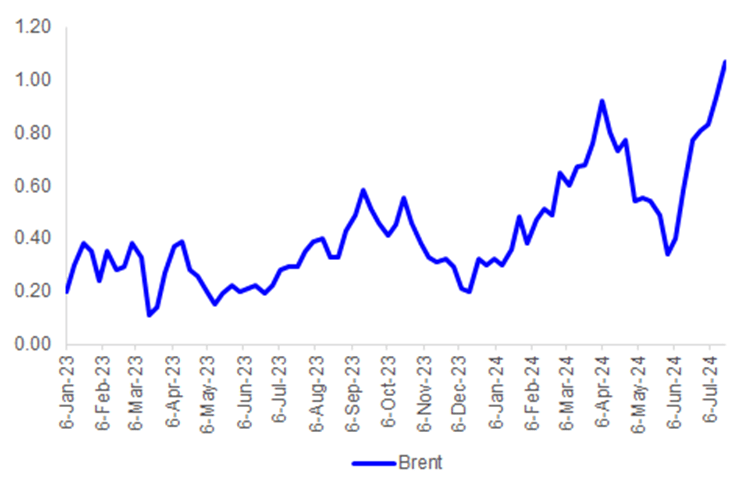

Crude prompt spreads have soared to the highest levels since 2023

The oil market has indeed tightened considerably in the past six weeks. Crude prompt spreads have soared to the highest levels, at least since 2023. Brent spread has shot-up from $0.34 on May 31st to $1.07 currently. WTI spread increase has been steeper, escalating from $0.33 to almost $1.5. This level of near-term backwardation is a clear sign of supply constraints in the oil market.

WTI Prompt Spreads ($/bbl)

Bloomberg

Brent Prompt Spreads ($/bbl)

Bloomberg

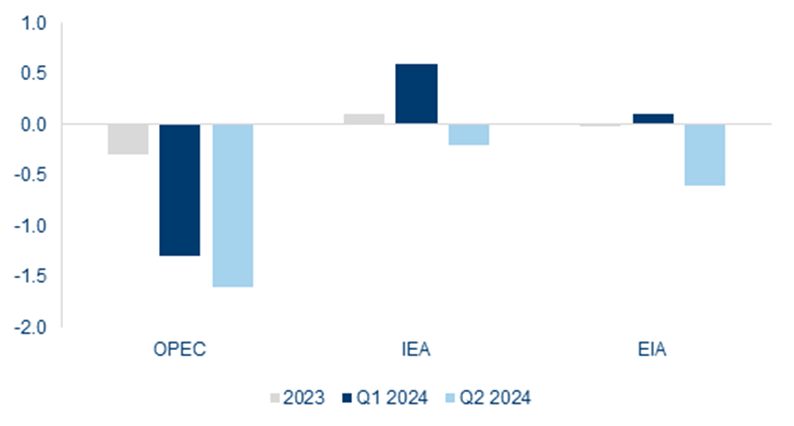

Consensus among energy agencies that the supply deficit has widened in Q2 2024

Another way to look at this is that there is clear consensus amongst energy agencies that the supply deficit has widened in Q2 2024 compared to 2023 levels. OPEC is the most aggressive, wherein it estimates the Q2 deficit at 1.6 mb/d. IEA and EIA estimate the Q2 deficit at 0.2 and 0.6 mb/d, respectively. Earlier, all the three agencies had calculated the oil market to be pretty much balanced in 2023.

Oil Market Balance through Q2 2024 - mb/d (OPEC, IEA & EIA)

Bloomberg

Loosening in OPEC+ supply from October is likely to be lower than the proposed quotas

OPEC+ has announced increase in quotas from October 2024 onwards. This envisages a monthly augmentation in production by roughly 200 kb/d till December 2025. This means that the total increment in production is proposed at nearly 2.5 mb/d from existing levels. There is already skepticism whether OPEC+ will go ahead with these output increases. As a matter of fact, the Saudi Ministry of Energy has also issued a statement saying that “the relaxation of the voluntary cuts can be paused or reversed subject to market conditions.”

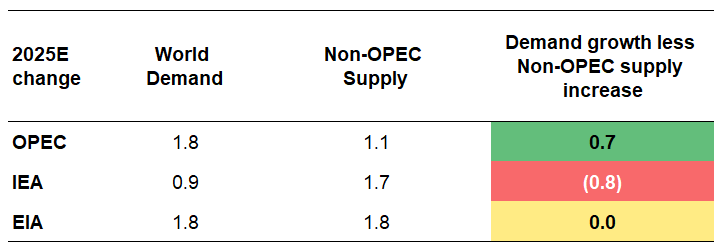

Energy Agencies – 2025 Demand and Non-OPEC Supply Estimates

Source: EIA, OPEC, IEA, Bloomberg, Analyst calculations

A look at the 2025 demand and non-OPEC supply estimates by the three energy agencies reveals an unsurprising deviance. OPEC is again the most aggressive wherein it expects demand growth to outstrip non-OPEC supply increase by 0.7 mb/d. IEA seems to be very conservative as it projects non-OPEC supply increment to exceed demand growth by 0.8 mb/d. EIA’s numbers seem to be the most realistic. With oil firming up in the $80-85 range, it is safe to say that OPEC+ would not be comfortable with a market surplus of over 500-600 kb/d in the coming quarters. This means that the actual output increments over the course of Q4 2024-2025 would be less than the proposed.

The best-case scenario would be to loosen supply in tandem with incremental demand, i.e., demand growth less non-OPEC+ (not non-OPEC) supply increase. It could be that the alliance announced an aggressive increase in production targets simply to appease members or to cajole them to maintain the existing levels. At the very least, it seems that OPEC and allies will not have to deepen the cuts unless numbers on the demand side considerably disappoint. We are of the view that given the resilience and discipline demonstrated by the cartel, the oil market will continue to remain tight in the medium term. This, of course, assumes that the renewed enthusiasm by Russia persists.