ryasick/E+ via Getty Images

Introduction

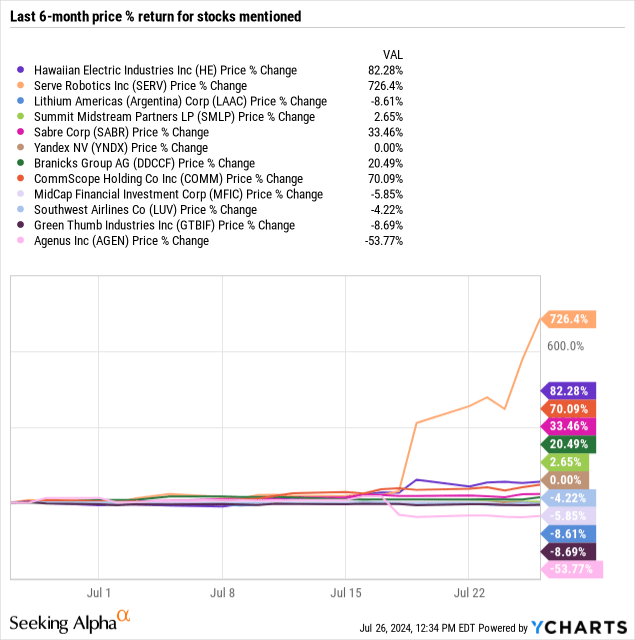

The 'Undercovered' Dozen series highlights undercovered stocks on our platform for you to have another source for idea generation.

This time we're looking at ideas published July 19th - 25th.

Take a look at what these less covered ideas might hold for you. And please join the conversation below to share what you think: are any of these worth following up on?

Hawaiian Electric Industries: Projecting Maui Fire Settlement

| Ticker | Rating | Analyst |

| HE | Sell |

"As long as a piece of string,” is an answer you might get to a question that cannot be specifically answered. It has been a bit like that with the question of how much Hawaiian Electric Industries, Inc. (HE) might have to pay as its share of compensation for victims of the Maui wildfires back in early August 2023. Figures as high as $5.5 to $6 billion have been floated. Recent announcements on plans for a settlement with a possible much lower liability for Hawaiian Electric have caused the company's share price to surge.

The measure of the piece of string, the amount potentially payable by Hawaiian Electric, is now a little more definite. The question on everyone's mind will be does the increased share price represent fair value based on this latest information? I am not prepared to forecast where the share price will go from here, but I will provide some comments and projections of what might unfold and impact on the Hawaiian Electric share price.

Serve Robotics Served Up A Big Nothingburger

| SERV | Sell |

July 19th ended up being a really great day for shareholders of Serve Robotics Inc. (SERV). Shares of the robotics company closed up 187.1%. This came after news broke of an investment by semiconductor giant NVIDIA (NVDA). At first glance, this kind of maneuver might seem to indicate that there is something of tremendous value at Serve Robotics that could warrant significant upside. And it is true that the company is making some pretty good strides toward its goal of deploying food delivery robots. But when you consider how the company is priced after this step up, and you consider just how much further the company needs to progress in order to justify its valuation, this comes across to me as a better selling opportunity for shareholders of the business than a buying opportunity.

Serve Robotics' food delivery robots could have great potential, but financials show significant losses and cash flow issues. Add on top of this the prospect of meaningful shareholder dilution just to get to market, and there are better opportunities that can be had.

Lithium Americas (Argentina) Stock: A Winner Even With Low Lithium Prices

| LAAC, LAAC:CA | Strong Buy |

Many lithium companies have gotten hammered as underlying commodity prices have come down, presenting investors in Lithium Americas (Argentina) Corp. (LAAC) an opportunity to acquire two world-class assets at a steep discount. With poor market sentiment, investments into lithium projects have ground to a halt, allowing the industry to gradually shift toward an undersupply and positioning prices for recovery.

Even in this “weaker” lithium market, LAAC is well-positioned to generate significant profitability given its position at the bottom end of the production cost curve. With a major partner in Ganfeng (OTCPK:GNENY) and its production ramp already significantly underway, LAAC is already materially de-risked and on its way to becoming a major lithium producer. Without any recovery in lithium prices, LAAC shares still have near-term upside in excess of over 100% - or 700% if lithium prices reach $35,000/tonne.

Summit Midstream: Refinancing And Conversion To C-Corp Could Mean A Double In Stock

| SMLP | Strong Buy |

Summit Midstream Partners, LP (SMLP) has had a busy couple of months. Following the asset sales in the Marcellus Basin, the company has completely restructured its debt, thereby lowering interest expense and boosting future cash flows. I believe the lower and now extended maturity debt plus higher cash flows will allow the company to pay accrued preferred distributions and then recommence common distribution. Also, yesterday (Thursday July 18th), the company's shareholders voted to convert from an MLP to a c-corp, which will broaden the possible shareholder base. A dividend and a broader base that can buy the stock in addition to a cheap valuation should lead to material moves higher in the units (soon to be converted into shares).

With a new capital structure, lower interest rates, and potential for higher multiples as a c-corp, SMLP stock could double in the next twelve months.

Sabre Is Being Disrupted By New Distribution Capability

| SABR | Hold |

American Airlines (AAL) built Sabre Corporation (SABR) in the 1960s to give travel agents access to airline price and availability data. Roughly 70% of Sabre’s revenue comes from its global distribution system ("GDS")—software that sits between travel agencies and airlines, allowing travel agents to see flight inventory, prices, and availability. The GDS business has historically been good because contracts are 3-5 years, and customers typically renew

Also, the GDS market is an oligopoly because Sabre, Amadeus, and Travelport control nearly the entire market. Sabre has the strongest presence in the US, whereas Amadeus has the strongest presence in Europe. Travel buyers will often pick the GDS with the most flights in their region, so each GDS has a competitive advantage in its regions.

That said, Sabre's Global Distribution System business, which accounts for 70% of its revenue, is threatened by the implementation of New Distribution Capability. The airline industry has long disliked GDSs, and some airlines are trying to push Sabre out of the value chain. Although Sabre is adapting by offering NDC-enabled GDS bookings, they are likely less lucrative than typical GDS bookings.

Yandex: Valuation After The Sale Of Assets

| YNDX | Hold |

The spin-off of the Russian and part of the international businesses from Yandex N.V. (YNDX) was completed this week, allowing Yandex to focus on the development of the remaining businesses, primarily Nebius AI's cloud business. Yandex N.V. also plans to rename the company to Nebius Group. YNDX's shareholders are expected to vote on these and a number of other issues at the AGM, which will be held on August 15. A complete list of the voting questions can be found in this press release. Since trading in the company's shares on the NASDAQ is still halted, and it's unclear how quickly trading can resume, let's look at how much the company's remaining business might be worth. Given the fact that there is not much public data on Yandex N.V.'s business and the businesses left by Yandex N.V. are very diverse, the best solution for valuing the company, in my opinion, would be a sum of the parts valuation. Let's dive in.

Branicks: Commercial Office Property Faces Headwinds, But Market Conditions Improving

| OTCPK:DDCCF | Hold |

Branicks Group AG (OTCPK:DDCCF) is one of the largest real estate asset managers in Germany, with AUM standing at €13.1 billion in 2024, consisting of 351 properties split between Industrial and Commercial Office, as well as an Investment Management business with €9.4 billion in assets under management.

The German real estate industry has experienced some of the most challenging market conditions for over a decade and Branicks has experienced one of the worst performances amongst peers as a consequence of depressed asset valuations and elevated levels of debt. However, I believe there is value within the portfolio of assets which can be realized through disposals as part of the strategic deleveraging plans. Diversification into renewable energy assets adds further risk to this turnaround story as the company seeks to reduce exposure to office properties and capture a piece of the growth in renewable energy.

Branicks offers compelling value at 14% of its Net Asset Value. However, given the current risks there are better opportunities elsewhere in the German listed real estate sector.

The Other Five Fit For Mention

CommScope: Depressed Sales Are Not The Solution

| COMM | Hold |

CommScope Holding Company (COMM) is a challenged network infrastructure provider, which has been hurt by too much debt and worsening operating performance. These challenges have been going for years, as the higher interest rate environment and weakness in 2023 sent the company into almost a debt spiral. The company now sells an important chunk of its activities to Amphenol, as relative leverage ratios likely only increase, making the situation still highly uncertain.

MidCap Financial Investment: Too Much Uncertainty To Go Long

| MFIC | Hold |

Last year, I assigned a neutral view to MidCap Financial Investment Corporation (MFIC) due to potential interest rate cuts and rising corporate default rates. Despite these concerns, MFIC slightly outperformed the broader BDC market, driven by a "risk on" mode in the sector. After dissecting the fundamentals of MFIC, including the potential benefits of the merger, I still do not gain sufficient level of comfort to go long here.

Southwest Airlines' Recovery Is Encountering Turbulence

| LUV | Hold |

Southwest Airlines Co. (LUV) has faced challenges in recent years, including a revenue guidance revision and Elliott Investment Management's purchase of a significant stake in the company. The airline is transitioning to a new revenue management system, which has impacted revenue performance, and is also dealing with delays in Boeing's delivery of the MAX 7 aircraft. Despite Southwest's strong track record and balance sheet, there are uncertainties surrounding revenue growth.

Cannabis Rescheduling And Green Thumb Industries: A Powerful Combination

| OTCQX:GTBIF | Buy |

July 22 marks the end of the public comment period for cannabis rescheduling, with a potential effective date as soon as September 22. Rescheduling is likely to move forward quickly due to the 2024 national election and the Democratic Party's support for pro-cannabis legislation. Green Thumb Industries Inc. (OTCQX:GTBIF) stands out as a top performer in the cannabis industry, with consistent positive earnings, strong cash flow, and responsible funding strategies.

Agenus: Novel Drugs That Just Are Not Novel

| AGEN | Sell |

Agenus Inc. (AGEN) is a small biotech company focused on developing cancer treatments, with a history of poor stock performance and financial struggles. The company's primary assets in its pipeline are Botensilimab and Balstilimab, which have shown limited efficacy in pre-clinical and clinical trials. Recent FDA meeting and phase 2 metastatic colorectal cancer data plummeted AGEN stock 60%, due to discouragement to file for accelerated approval.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.