bjdlzx

Parex Resources Inc. (OTCPK:PARXF) mentioned in the latest quarterly report that production was heading towards the lower end of guidance because there was some underperformance. Management took the proper action by stopping the intended actions and then redirecting capital until the whole situation could be properly evaluated. Welcome to oil and gas, where outcomes frequently either do not exceed guidance or provide a surprise to the upside.

However, the strong balance sheet allows management as many tries as it needs to find significantly more oil. Since management is on course and doing what is expected, it is likely time to “stay the course” and not “abandon ship” just because a well came in at a disappointing rate.

The Last Article

The last article mentioned that Parex was a Canadian company that reports in United States dollars and does business in Colombia, South America. This quarter, management repaid some of that debt so that there is a $50 million balance remaining. That balance is easily handled given the reported EBITDA for the quarter. In many ways, debt is so low compared to cash flow and EBITDA that this can be handled as a debt free situation.

One thing to note is that Colombia has historically been far more supportive of its oil and gas industry than has some other areas of the continent. However, the government is not quite as effective as one would expect living in the United States. Therefore, even though the environment is overall positive, it is a bit more complicated doing business there, than it would be in North America.

Growth

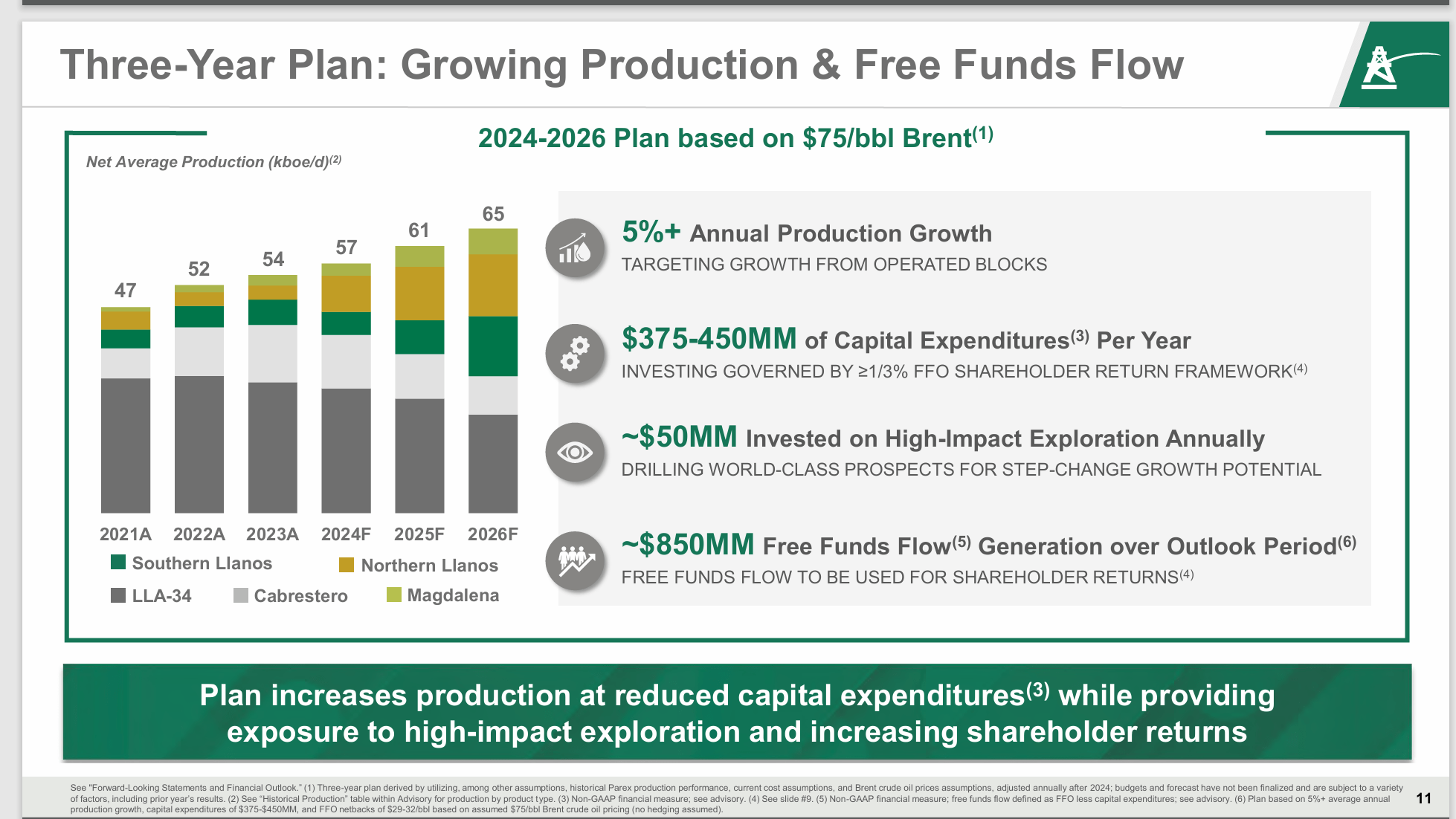

This fiscal year will likely show minimal growth. But management shows no signs of backing down from their growth-oriented strategy. Therefore, the long-term orientation of the growth strategy appears intact. The temporary disappointment may be a time to consider this stock because if management ever “hits it big” with a discovery, it will then be too late.

Parex Resources Long-Term Growth Plan (Parex Resources Second Quarter 2024, Corporate Presentation)

The growth plan is suitably conservative. But like any plan, it can be changed it management “gets lucky”. I am a firm believer of companies that hit a lot of singles and doubles (like this one) while showing steady growth are the ones most likely to “hit a homerun”. The problem with the oil and gas business is that patience is required because no one knows where that “homerun” is and hence exactly when it will be hit. Trying to time such an event is way above my pay grade.

Also note, that when management has a disappointment (as it does this quarter), the budget is conservative enough for management to still meet the long-term growth rate even with a few disappointments along the way.

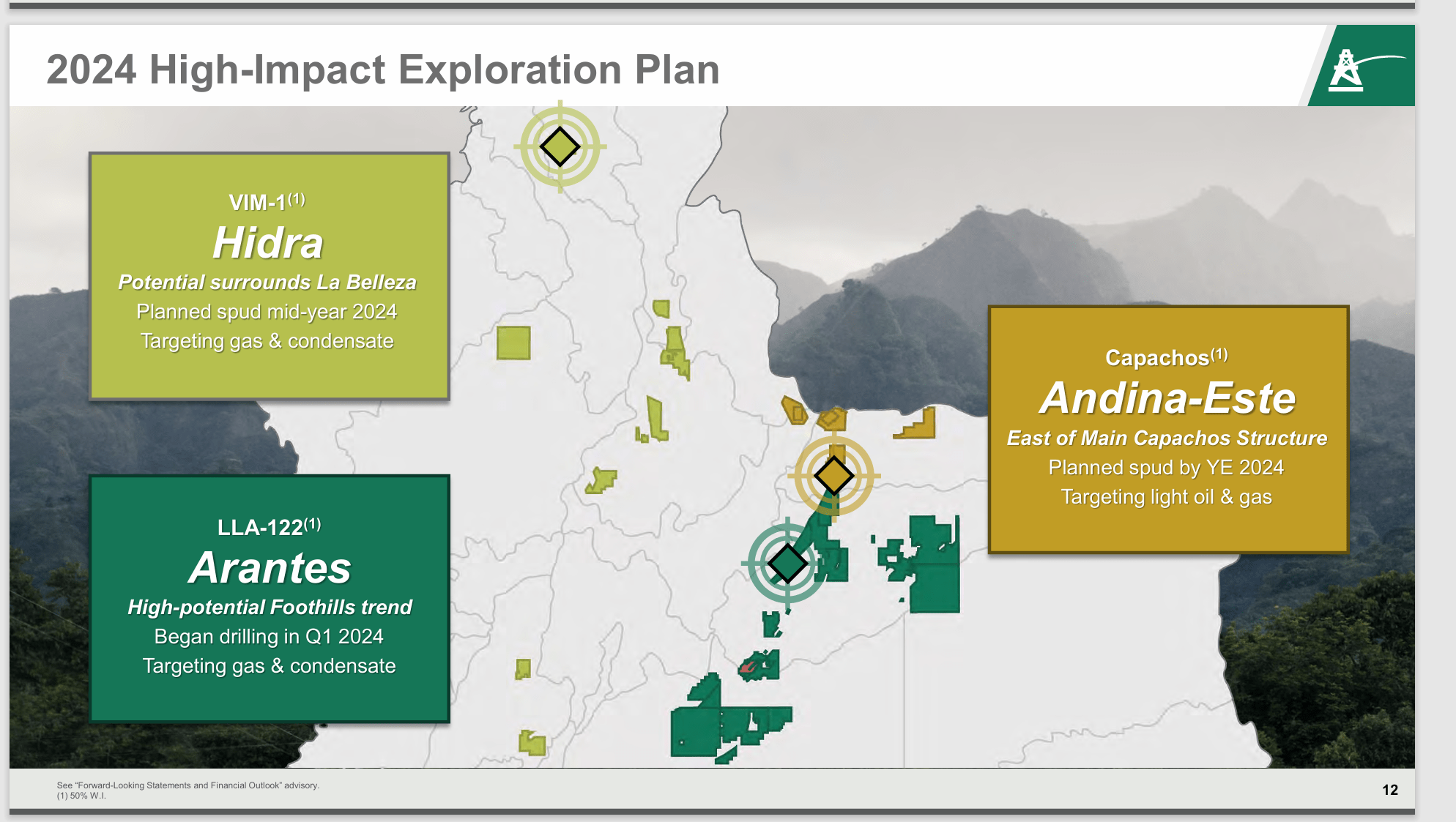

Parex Resources High Impact Exposure Budgeted For Fiscal Year 2024 (Parex Resources Second Quarter 2024, Corporate Presentation)

The other consideration is that the high-impact part of the budget is balanced against a goal of showing some growth “no matter what” and shareholder returns. Of course, maintaining the balance sheet remains the top priority. Many things can go “out the door” before that does.

Earnings Summary

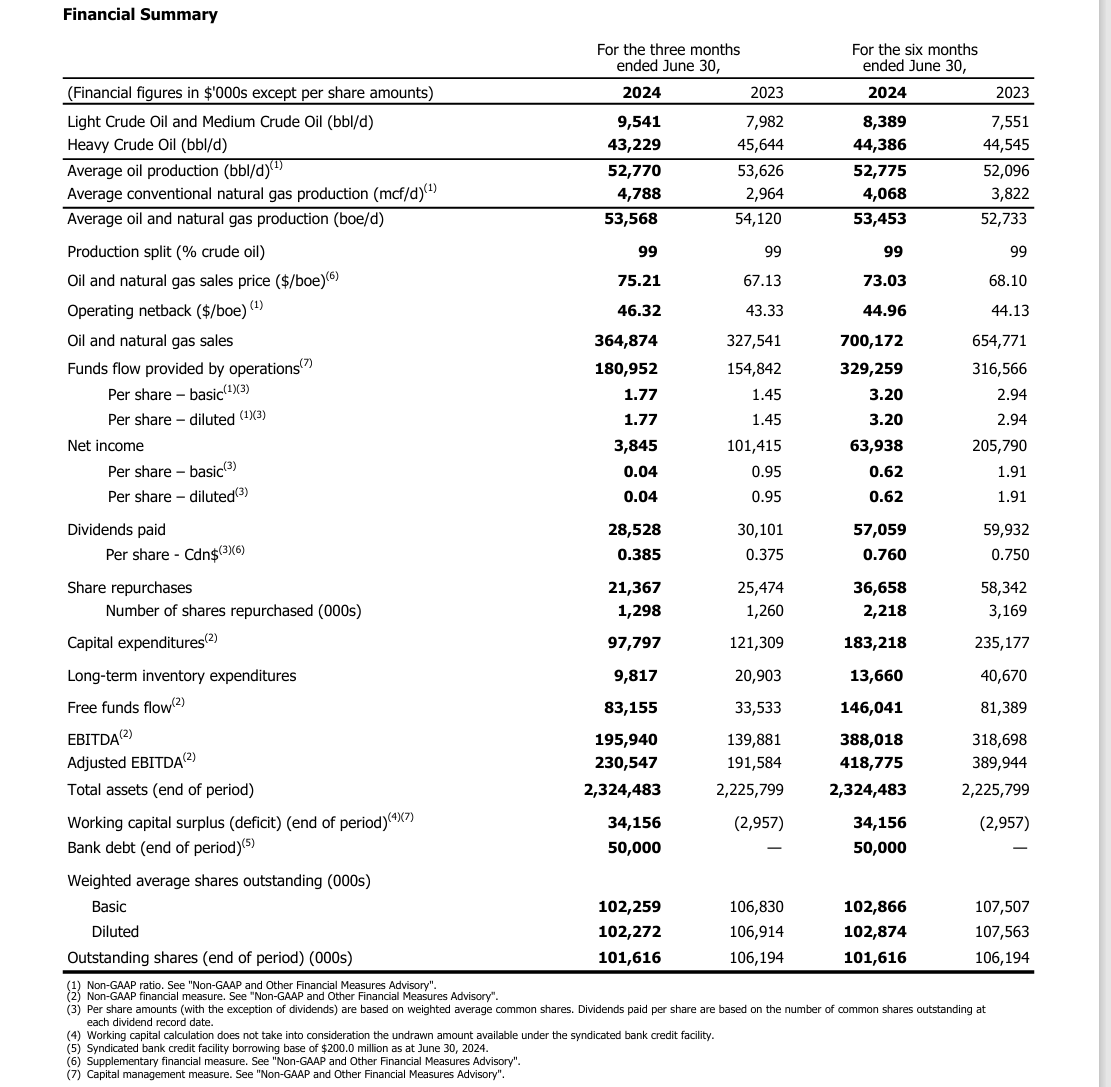

Despite the well results disappointment, cash flow is comfortably higher than it was the year before on level production (roughly).

Parex Resources Financial Summary Of Quarterly Results (Parex Resources Financial Statements And Management Discussion And Analysis Second Quarter 2024)

The improvement in cash flow is largely due to better prices received for production. Capital expenditures are down. That would be indicated if a well underperformed expectations and there was capital dedicated to that area of underperformance.

Note also that management has been repurchasing shares on the open market. Companies that do business in Colombia (primarily) will often sell at a discount to companies that do business in Canada. Similarly, companies that do business in Canada likewise sell at a valuation discount to United States oil and gas companies. This situation generally allows for a continuing share purchase program by the company. It is one way for per share profits to grow faster over time than the company profitability.

Stock Price

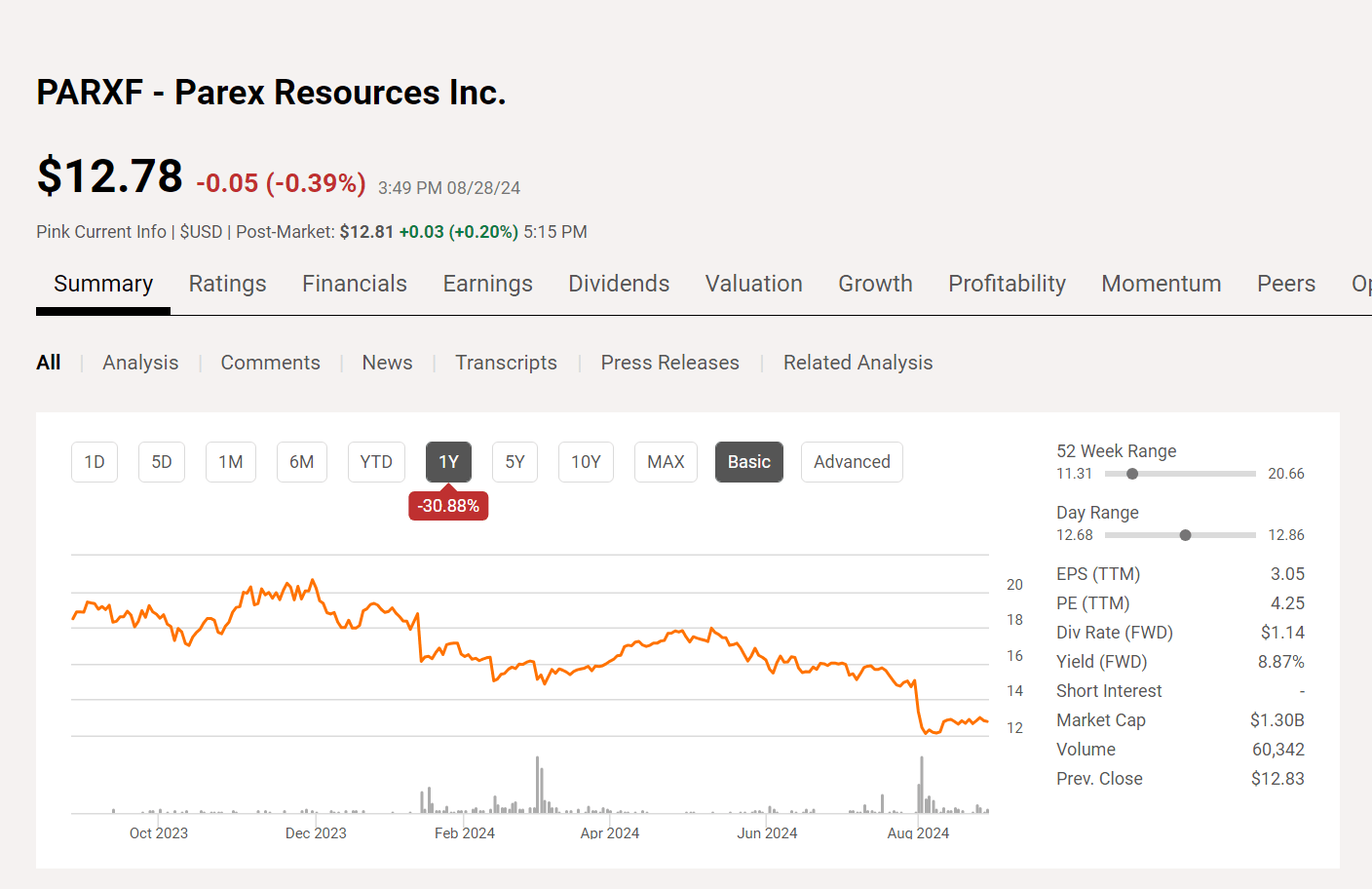

The valuation is beginning to get ridiculously low. That kind of thing often means that the market itself is likely to enter correction mode down the road. Oil and gas often outperforms the market in a downturn. But sometimes that means the out-of-favor stocks go “crazy low” because they are out-of-favor. Fundamentals do not matter temporarily. They will later though.

Parex Resources Common Stock Price History And Key Valuation Measures (Seeking Alpha Website August 28, 2024)

Before we get started, it needs to be noted that this is an upstream company and that as an upstream company, commodity price levels play a huge role in the staying power of the dividend.

However, that dividend yield is now roughly meeting the return that many investors report annually. Any one of those impact wells that turns out to be a success will only provide more upside potential in the future.

The payout ratio is on the low side and there is a large cash balance. The only threat to that dividend is a period of severe commodity price decline that susains longer than anticipated. But the balance sheet strength probably “ensures” that the dividend would be restored quickly after such an event passes.

There is an advantage here over the far more widely covered Petrobras (PBR) in that the government has no financial interest in this company. This company is therefore far more likely to be efficiently run. To me, that makes the above dividend rate far more sustainable.

Summary

Parex Resources remains a somewhat speculative strong buy that deserves consideration for anyone that can handle the risk of doing business in Colombia, South America. The very strong balance sheet and good cash flow offset much of the business risk.

The stock is getting into “crazy low” territory in that cash flow is currently at an annual rate of at least $6 per share. Meanwhile, the stock price is about twice the cash flow. To say that the pessimism is overdone is an understatement.

That dividend should provide downside protection, as should the sizable cash balance. In the meantime, the recovery potential appears to far exceed the downside possibility, while any “homeruns” would be icing on the cake.

Because of the possibility of an extraordinary discovery, it is hard to say what the stock price will be in 3 to 5 years. But even if management never finds that “elephant”, the stock price should probably at least double over five years from current levels in a wide variety of commodity price environments, plus that dividend.

Risks

Any upstream company is subject to the volatility and low visibility of future commodity prices. A severe and sustained downturn can materially affect the future of the company. In this case, the extremely low debt levels likely mean much of the industry would suffer long before this company does.

Colombia is subject to periodic protests and blockades that can reduce production for the duration of such actions. This company seems to handle the situations rather well.

Colombia has so far proven to be far more supportive of the oil and gas industry, despite the leftward turn of the government. This is a much better record overall than is the case for much of the South American Continent. That can change without much notice, and it may be responsible for much of the stock price discount.

The loss of key personnel could materially set Parex Resources Inc. back, in the future.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

I analyze oil and gas companies like Parex Resources and related companies in my service, Oil & Gas Value Research, where I look for undervalued names in the oil and gas space. I break down everything you need to know about these companies -- the balance sheet, competitive position and development prospects. This article is an example of what I do. But for Oil & Gas Value Research members, they get it first and they get analysis on some companies that is not published on the free site. Interested? Sign up here for a free two-week trial.