shapecharge

The July recession scare

The US Bureau of Labor will produce the labor market data for August on Friday. This will be an extremely important event, given what happened last month, when the July labor market data was released.

The July labor market data indicated a significant weakening in the labor market, which raised the possibility that the US economy is facing an imminent recession.

Specifically, the unemployment rate unexpectedly increased to 4.3%, which triggered the Sahm Recession indicator rule. In addition, the non-farm payrolls dropped unexpectedly to 114K, with negative revisions to the previous months (and also a negative revision of over 800K jobs for the year with the later release).

Prior to the July monthly jobs data, the weekly initial claims also spiked to 250K, and this is considered a leading indicator. Thus, the recession seemed to be imminent. As a result, the bond market started to price a significant monetary policy easing, even an emergency cut. The stock market had a "flash crash" with the VIX volatility index spiking to the Lehman Brothers levels.

The Fed Chair Powell confirmed that the Fed's focus is shifting towards the full employment mandate at the Jackson Hole symposium, expressing the concerns about the weakening labor market, and stating that the Fed "does not welcome further increase in the unemployment rate". This signaled the beginning of the monetary easing cycle, possibly at the September meeting.

Better employment data expected in August

But what happened since the July labor market data release? The initial claims for unemployment fell to the 230K level, which suggested a strengthening and still very tight labor market, given that the 230K level for the claims is still very low based on historical standards.

Thus, the consensus expectations for the August labor market data are for the improving conditions. Specifically, the market expects:

- a downtick in the unemployment rate from 4.3% to 4.2%

- an increase in the non-farm payrolls from 114K to 165K

- an increase in the hourly wage from 0.2% MoM to 0.3% MoM

Trading Economics

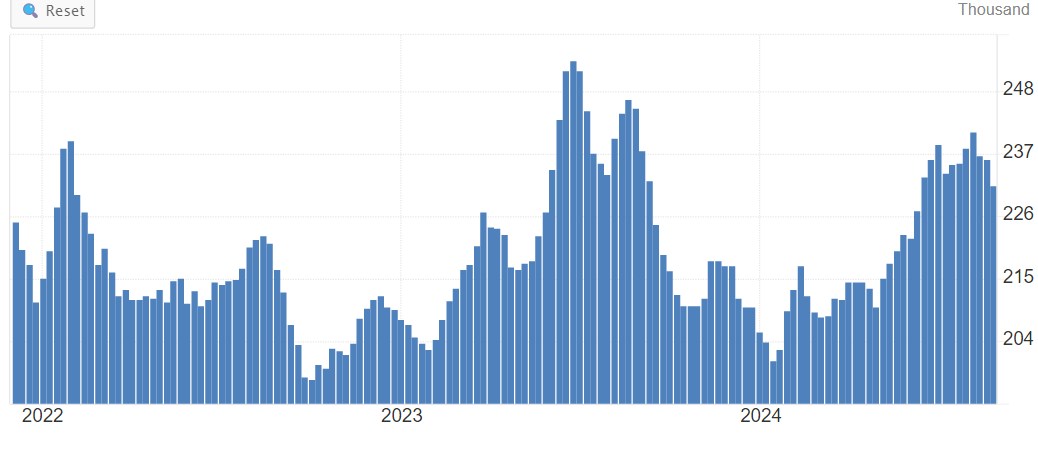

Here is the chart for the initial claims for unemployment (4-week average). This is a higher-frequency leading indicator for the labor market conditions. Usually in a recession, the weekly claims spike, as companies lay off workers, and these workers rush to file for unemployment benefits.

The weekly claims have been falling since the August 3rd peak - and until the claims get above the previous high, and continue rising, the recession continues to be delayed. It is what it is, and what the data is showing. There were three episodes since 2022 when the claims spiked, and each time the recession was avoided as the claims fell back.

Trading Economics

It's about the labor supply now

The unemployment rate spiked in July to 4.3% due to an increase in the labor supply, and not due to layoffs. So, even this was not recessionary.

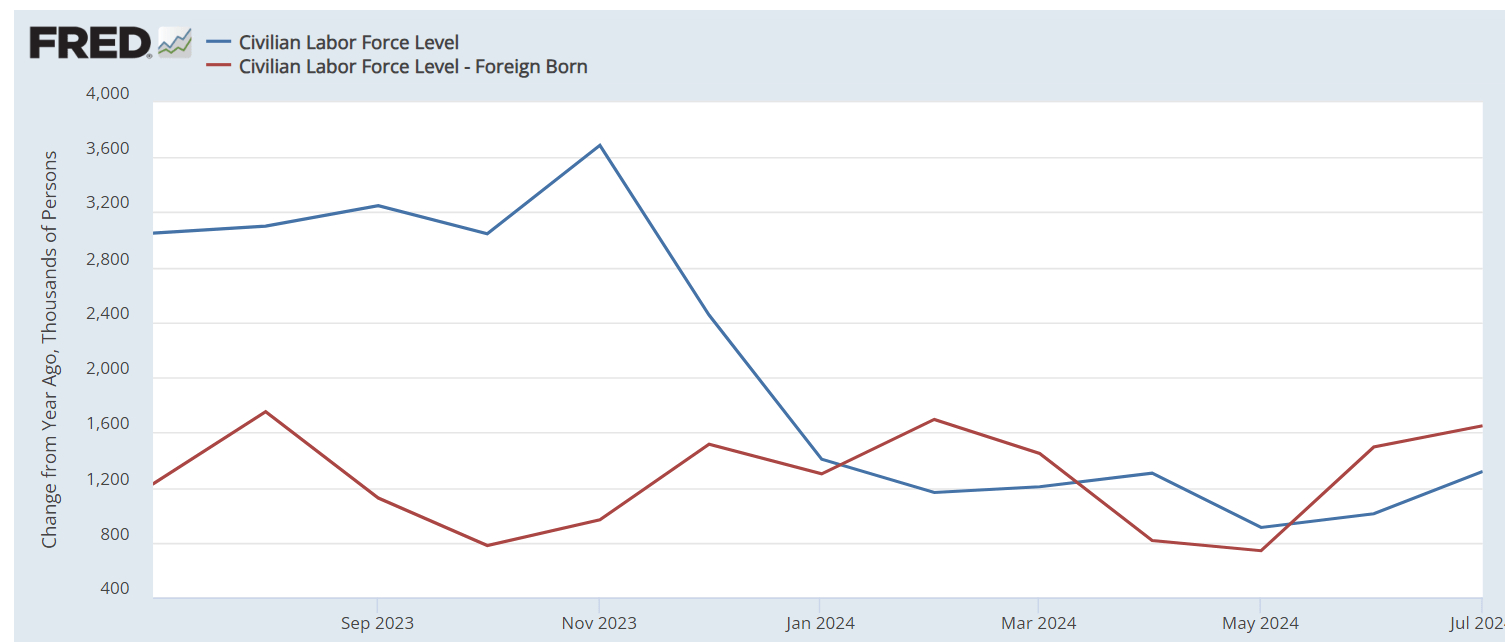

Specifically, we are facing a situation where there is a very high level of illegal immigration to the United States, and these workers are considered by the household survey (which reports the unemployment rate) as the increase in foreign born workers.

Here are the facts:

- the US civilian labor force increased by around 1.3M over the last 12 months, while

- the foreign born civilian labor force increased by over 1.6M over the last 12 months, thus

- this means that without the foreign-born labor force, the total US labor force would have decreased by around 300K over the last 12 months, which means that labor shortage would have worsened.

Trading Economics

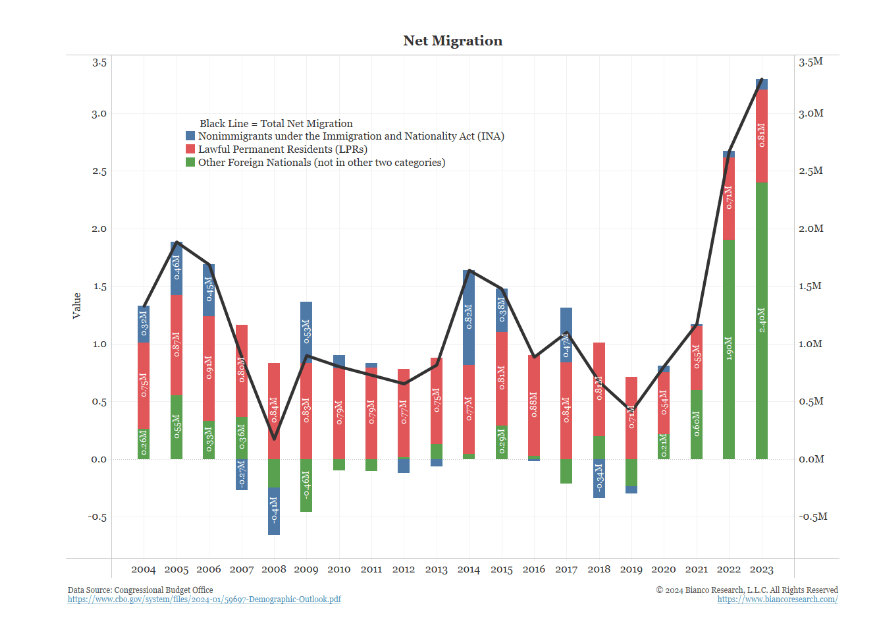

Jim Bianco of Bianco Research provided a chart that shows a significant spike in net migration in 2022 and 2023 and that most of the US population growth over the last few years has been due to illegal immigration (green bar).

LinkedIn

Why is this important? The unemployment rate has been increasing due to the increase in the labor force, and not due to the lay-offs. Thus, this situation is not recessionary, actually it's pro-growth, and ultimately inflationary.

The Fed's expected easing cycle is misguided

So, the Fed does not welcome a further increase in the unemployment rate above 4.3%, and thus it is getting ready to start easing monetary policy. This means that the Fed wants all foreign-born workers to find a job. However, this will translate into a higher demand for housing, and other goods/services, and ultimately higher inflation.

Thus, the Fed should not be reacting to the higher unemployment rate. In fact, Powell fully understands that the primary cause for the higher unemployment rate is an increase in the labor supply, and even dismissed the Sahm rule as the recessionary indicator in the current situation.

Yet, the Fed is still signaling a possible cut even in September, and this could turn out to be another Fed mistake if inflation turns higher.

What to look for in the August labor market report?

Thus, these are the things to focus on in the August labor market report:

- Change in the labor force vs the change in the unemployed persons in the household survey, which produces the unemployment rate. As long as the number of unemployed persons does not increase, the recession continues to be delayed, even if the unemployment rate increases.

- The jobs in the leisure and hospitality and construction sectors. Both of these cyclical sectors added around 25K jobs in July, which was actually a positive cyclical signal. As long as these cyclical sectors continue to add new jobs, the recession continues to be delayed.

- Revision to the non-farm payrolls. Will the July non-farm number be revised lower (this is a negative signal) or higher (this would confirm the recession scare thesis)?

Implications

The S&P 500 (SP500) is facing a recessionary bear market, as the recession is ultimately likely to hit the US economy. However, this recession keeps getting delayed, despite some obvious warning signs, like the inverted yield curve, exhaustion of pandemic excess savings, consumer sentiment, etc.

The recent increase in the unemployment rate is not recessionary because it's caused by the increase in the labor force, primarily due to immigration. However, there are many signs that the recession is not that far off and underneath the surface the labor market is weakening, for example, the loss of temporary jobs, and the increase in part-time jobs.

The investors are facing a situation where the Fed is now expected to cut, but the economy is not in a recession yet. In fact, if the economy is at the turning point, and:

- the data weakens while the Fed cuts, the stock market is bound to fall sharply as the earnings estimates are revised lower (recessionary bear market), and the Gen AI bubble continues to burst,

- the economy continues to grow, the stock market could further rise, for as long as the recession keeps getting delayed, or higher inflation prevents the Fed from easing.

It's not prudent to be short the market in a situation where the Fed is expected to cut, while there is no imminent recession. However, at the same time, it is not prudent to chase the market when the S&P 500 (SPY) P/E multiple is at 24. Thus, I am currently neutral on the S&P 500.

We are at the turning point, and the data will be volatile. It's possible that the claims spike on Thursday above 250K, and just like that we are back to an imminent recession mode and the short position. At the same time, it's possible that the data continues to point to lower inflation and positive growth, and the bubbles continue to inflate.

The key point will remain what the Fed says and does. The Fed could "walk away" from the signaled September cut if the August labor market data comes stronger, as currently expected, and that could be a negative trigger for the stock market. Or not, the Fed could be politically motivated and still cut before the election, which would be positive for the stock market. So, let's sit tight neutral for now and wait for more information. I outlined my current strategy in this article.