bymuratdeniz/iStock via Getty Images

NICE (NASDAQ:NICE) is a leading CCaaS (Contact Center as a Service) provider with growth and profitability higher than sector averages but trading at a significant discount. The share price dropped $30 in a day from $228 to $198 due to the resignation and retirement of its CEO. Prices have weakened further but stabilized at the $175 mark. At these prices and given the growth prospects, we believe it provides an excellent opportunity to buy into growth at a reasonable price. We initiate with a buy rating.

The Company

NICE provides organizations with tools to optimize and enhance customer experience. Its cloud platform, CXone a CCaaS, helps with customer interactions, from AL chatbots to voice conversations. NICE also offers cloud-based financial crime and compliance solutions through its X-Sight platform. The company is listed on the Tel Aviv Stock Exchange, and NICE ADR’s have been trading on NASDAQ since 1996. 85% of its revenues are generated from the Americas, mainly the US. They have more than 8,400 employees and operate across 30+ countries.

NICE has adopted and recognized the requirement for its enterprise solutions to digitalize, be cloud-based, and more recently, artificial intelligence, and the fusion of the three. Its SaaS (software-as-a-service) model and its comprehensive lineup of CX solutions ensure recurring and increasing revenues from existing customers.

Barak Eilam, CEO:

We continue to gain market share with the most comprehensive CX platform in CXone, rapid innovation in AI that is experiencing significant enterprise adoption and the flexibility afforded by our rock-solid financial position. We are positioned to further expand our market leadership and deliver long-term growth.

Only 20% of the market the company operates in has shifted to the cloud, giving ample scope for growth. Governments, companies, and other organizations are digitalizing, and looking to use more AI-powered analytics and automation. These are the key strengths of NICE, and we get an outlook into the potential size of the market and the scope for midterm growth.

NICE operates in a highly competitive market, yet there are high barriers to entry. New vendors to specific products with new technologies may pose threats in particular areas. However, NICE’s integrated solutions and its full range of products give it an advantage. Companies with deeper pockets, a larger customer base, bigger databases, patents, and intellectual property portfolios are the chief risks faced by NICE.

NICE has grown its customer base, patents, and products organically and through multiple bolt-on acquisitions. They acquired LiveVox in December 2023 for $424m. For FY24 LiveVox is expected to contribute $142m in revenues, putting it at par with the sector average PS ratio of 3x, but significantly cheaper than NICE’s 10-year average of 5x or FY24 of 4.1x. Similarly, in 2021 and 2022 they made several smaller acquisitions for a total sum of $184m. Mattersight, a cloud-based analytics for customer service organizations, was acquired for $105m in 2018.

Financial analysis

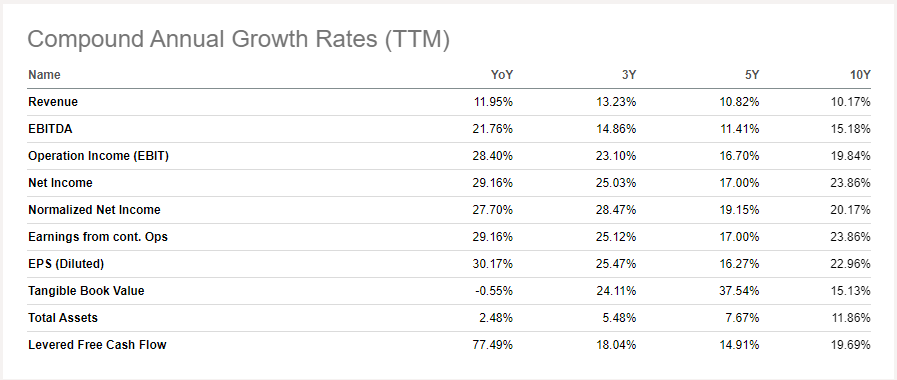

The company has an impressive track record in revenue growth and strong margin expansion.

NICE Growth Profile (Seeking Alpha)

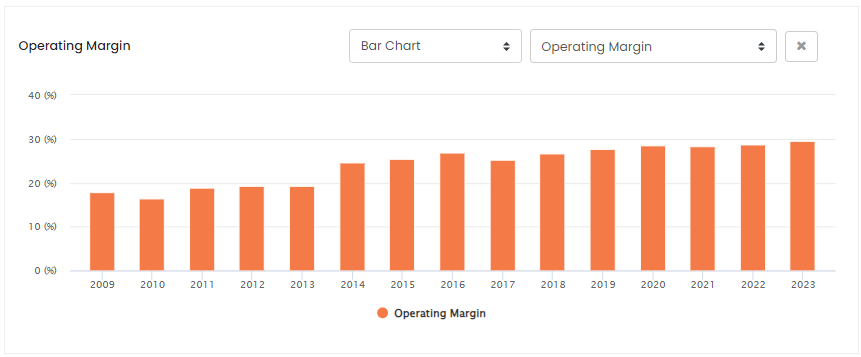

Long-term revenue growth has been impressive at over 10% and earnings growth higher. Its market leadership and its comprehensive CX platform have helped margins improve.

NICE Operating Margins (ROCGA Research)

FY23 results did not disappoint, revenue growth slowed but we up 9% to $2.4bn, and operating margins improved from 28.7% to 29.6%. Non-GAAP EPS was $8.79, 15% higher compared to last year.

Increasing revenues in Q1 and Q2 made up for the slight slowdown during FY23. 2024 H1 clocked in an impressive 15% increase in revenue and operating margins improved further from 29.2% last year to 30.4%.

The impressive performance is partly organic and to some extent a portion coming from the December 2023 acquisition of LiveVox. We estimate LiveVox contributed 5% to 6% to the total growth, bringing organic growth to approximately 9% to 10%. This is still commendable, as NICE managed to grow without diluting existing shareholders' equity or taking on debt. As of June 2024, NICE had a cash and equivalent pile of $1.5bn, up from December 2023’s $1.4bn. Total debt decreased from $783m in December 2023 to $568m at the end of Q2 2024, improving balance sheet strength.

Management expects growth to continue and is forecasting 15% revenue growth and a mid-range EPS growth of 22% for FY24. Consensus estimates point to the same numbers for FY24, and the analysts expect growth to continue but taper back to historical averages of 11% for revenues and 15% for EPS growth for FY25.

Valuation

Before we look at valuation, let us look at some of the key drivers that help determine the intrinsic value of a company. The first is profitability, and NICE scores top marks on all measures. Not only are its margins improving, but they are significantly higher than the sector averages. Top-line growth is also slightly higher than its 5-year average and is higher than the sector averages. EPS growth is more than double the sector average. Share price momentum is not on the company's side, but these have stabilised since June.

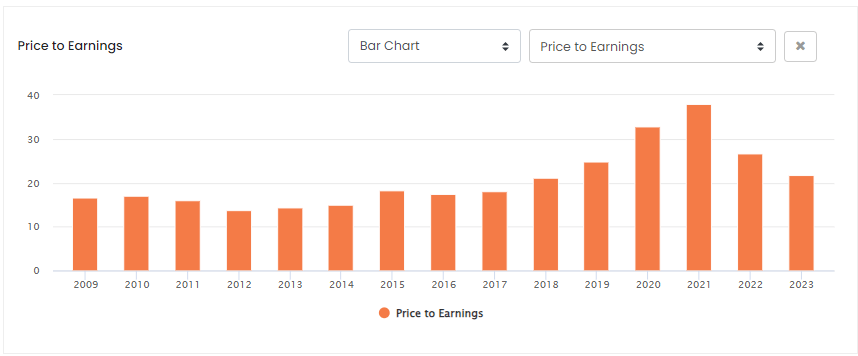

Before 2016 NICE was trading at a PE ratio between 14x and 18x. This has increased in recent years. Some of the increase was warranted, but the company was overvalued during 2020 and 2021.

NICE PE Ratio (ROCGA Research)

Share prices have continued to decline since early 2022 and have fallen below warranted value, and at current prices, offer a good investment opportunity.

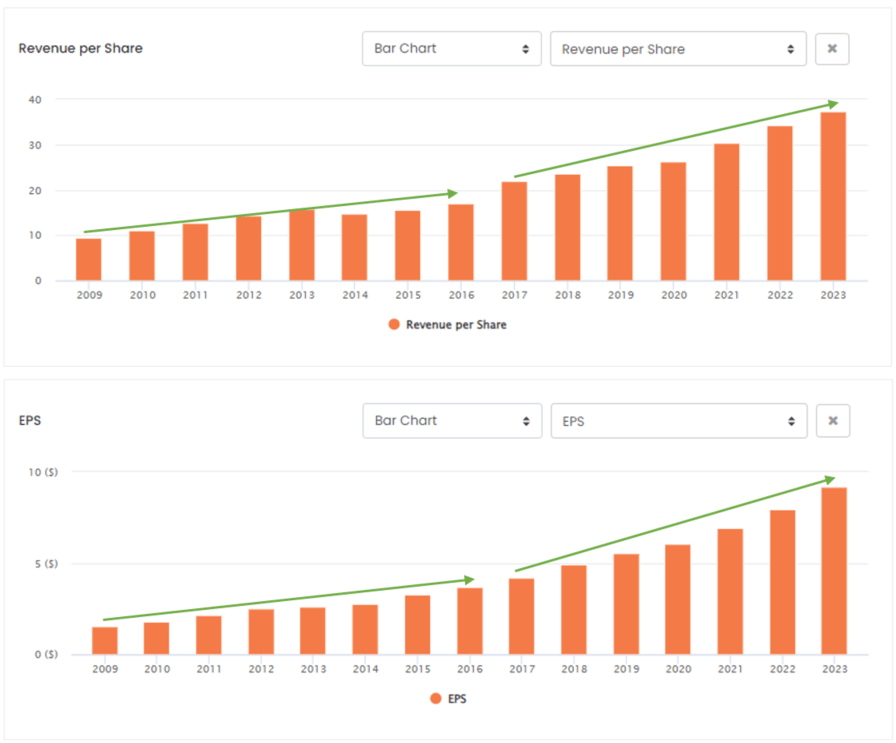

Growth in revenues and EPS have accelerated since 2017 and NICE should be trading on higher multiples than it was pre-2016.

NICE Increasing Revenue And EPS Growth (ROCGA Research)

We can see in the charts above that growth has been steeper since 2017.

As a quick recap, growth and profitability are higher than sector averages and NICE is trading at a discount to sector averages on valuation multiples. Despite its superior financial profile, if the prices were to trade at the industry average PE ratio (FWD, Non-GAAP) of 24.1x, the target price for NICE should be approximately $258.

Conclusion

We think revenue growth and profitability will continue to improve. The superior financial performance, high volume of recurring revenues, strong balance sheet, and being at the forefront of the digital and AI-based analytical and cloud-based transition put NICE in a strong position. They should be trading at a higher valuation multiples. FY24 PE of 16.2x is too low for a high-quality high-growth company and at the very least should be trading at the sector average PE. NICE presents itself as an excellent GARP opportunity.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.