andreswd

Since the publication of my previous article, “Sanofi: A Leader In Life-Saving Vaccines And Treatments,” Sanofi’s share price (NASDAQ:SNY) (OTCPK:SNYNF) has grown by more than 18%, once again reaching a high last seen in April 2023, despite the disastrous results of the GEMINI 1 and 2 studies evaluating the efficacy of tolebrutinib in the treatment of relapsing forms of multiple sclerosis.

Looking ahead, I believe that this outcome will not have a significant impact on the expected continuation of the trending momentum of the stock price of the largest French pharmaceutical company since its rich portfolio has more promising product candidates for the treatment of this neurological disorder, including frexalimab and oditrasertib.

In addition, in this article, I will provide an analysis of the sales of its oncology, immunology, and rare disease franchises, recent progress in its late-stage clinical development programs, and the impact of the acquisition of Inhibrx, which was completed on May 30, 2024, on its long-term financial position.

Sanofi's financial results for the second quarter and 2024 outlook

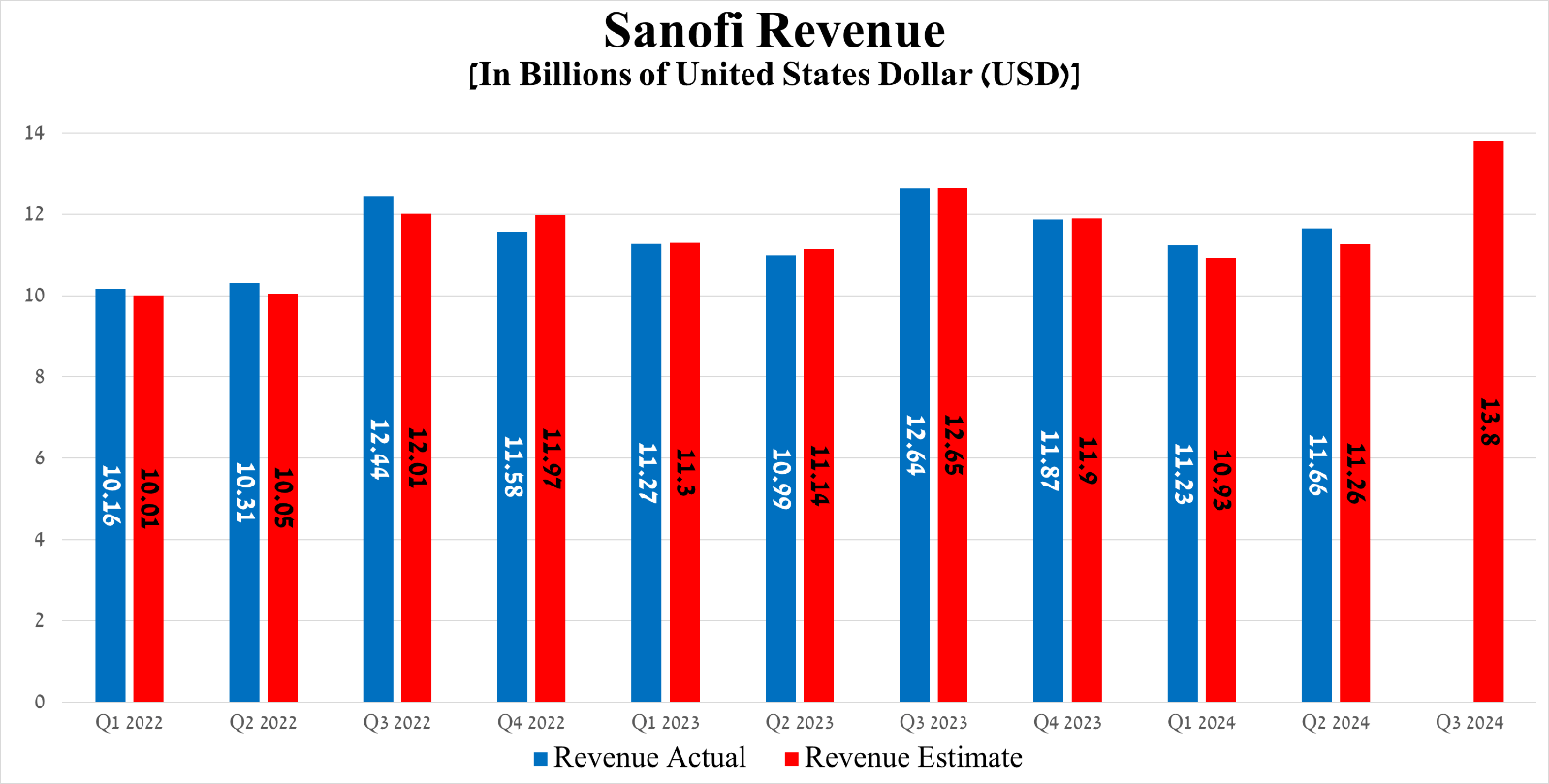

The Paris-based company's revenue was approximately $11.66 billion in the second quarter of 2024, up 6.1% year-over-year and beating the consensus estimate by $400 million.

Source: Seeking Alpha

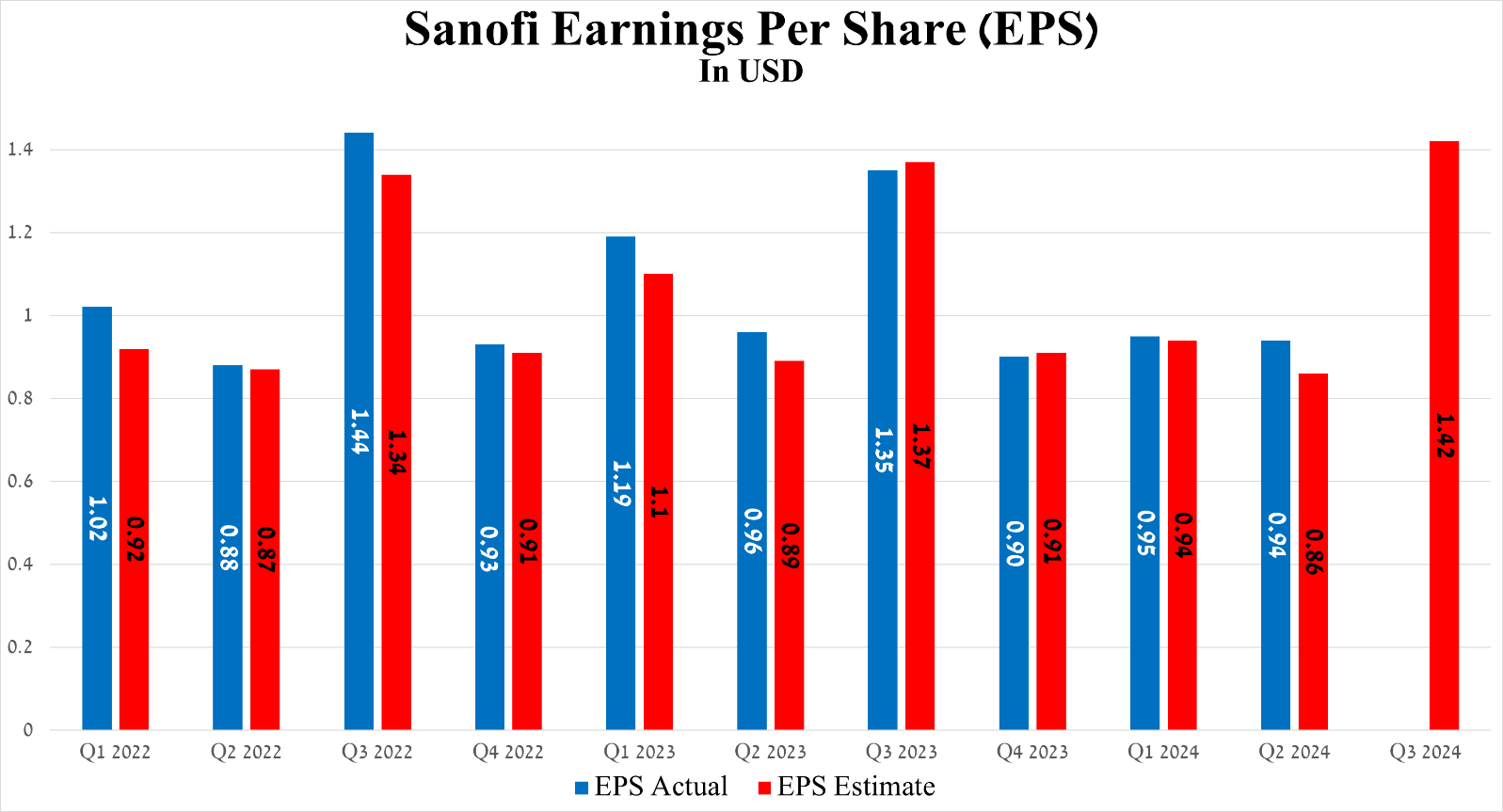

On the other hand, its earnings per share amounted to 94 cents for the three months ended June 30, 2024, slightly down quarter-on-quarter but beating analysts' expectations by 8 cents.

Source: Seeking Alpha

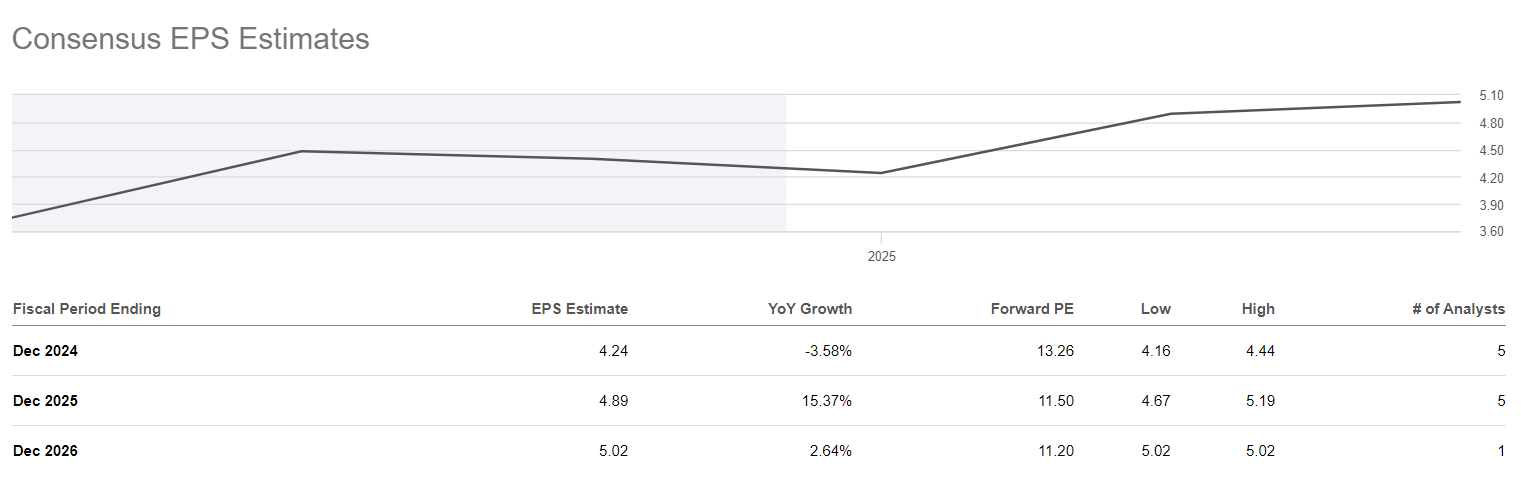

Let's look at this most important financial metric on a larger scale, namely its dynamics up to 2026, and it will pleasantly surprise Seeking Alpha readers, especially those who are not familiar with Sanofi's business.

So, its EPS is expected to grow from $4.4 in 2023 to $5.02 by 2026, thanks to increased sales of its blockbusters, as well as due to the expansion of indications for the use of recently launched drugs.

Source: Seeking Alpha

In addition, I believe that regulatory approvals of next-generation vaccines and medications in late-stage clinical development, including amlitelimab, rilzabrutinib, duvakitug, and fitusiran, as well as the expected spin-off of its consumer division, which is valued at between €18 billion and €20 billion, will help reduce the French pharmaceutical giant's total debt and accelerate its EBIT margin growth in the long term.

Ultimately, its non-GAAP P/E ratio will fall from 12.7x to 11.2x, signaling to financial market participants that Sanofi is trading at a discount to many of its peers, including Novartis (NVS), Merck (MRK), and AstraZeneca (AZN).

Let's continue.

The figures that reflect changes in Sanofi's revenue and net income are undoubtedly important, but I believe the primary focus should be on identifying key factors and assessing the impact of each on the development of its business in recent months and over the long term.

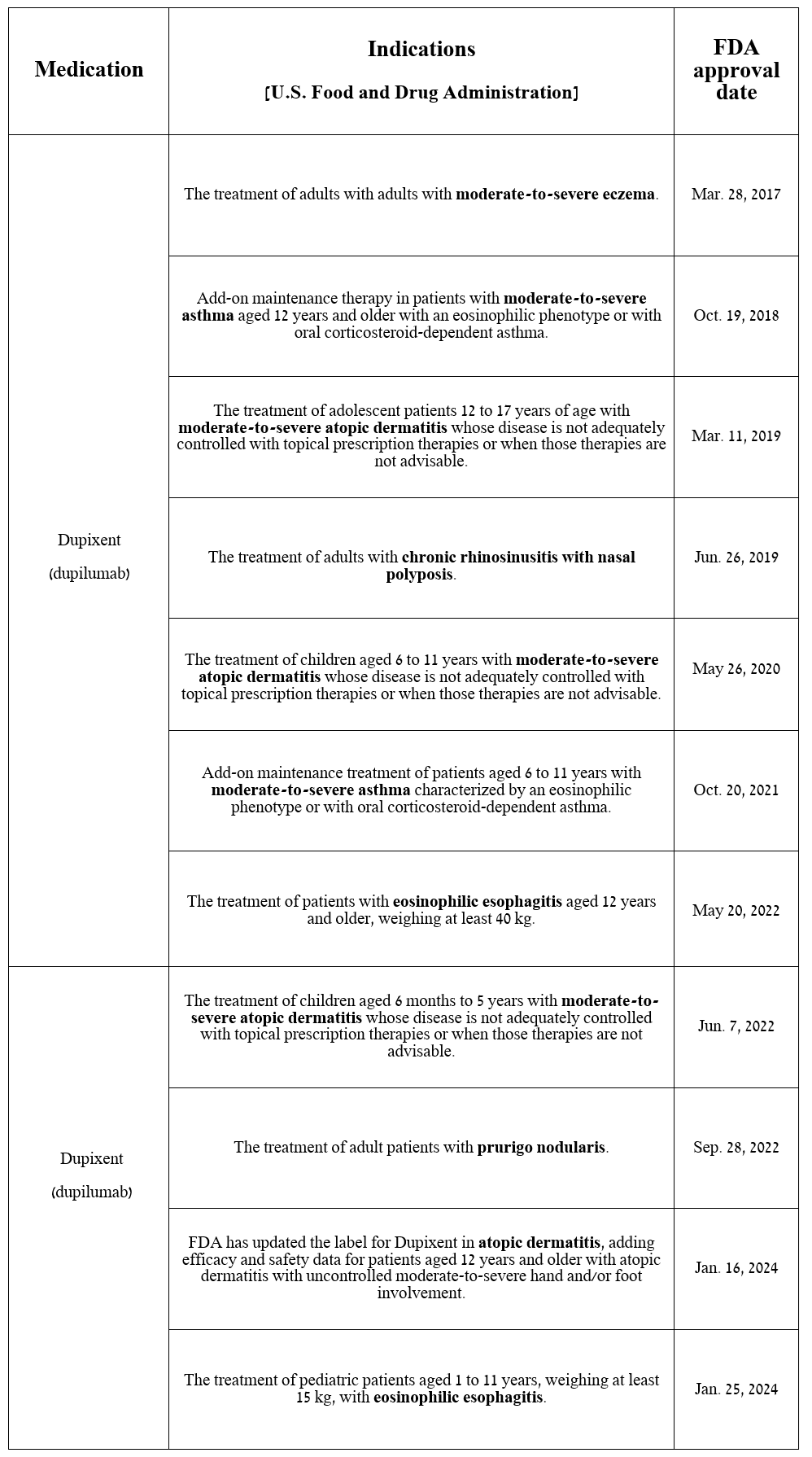

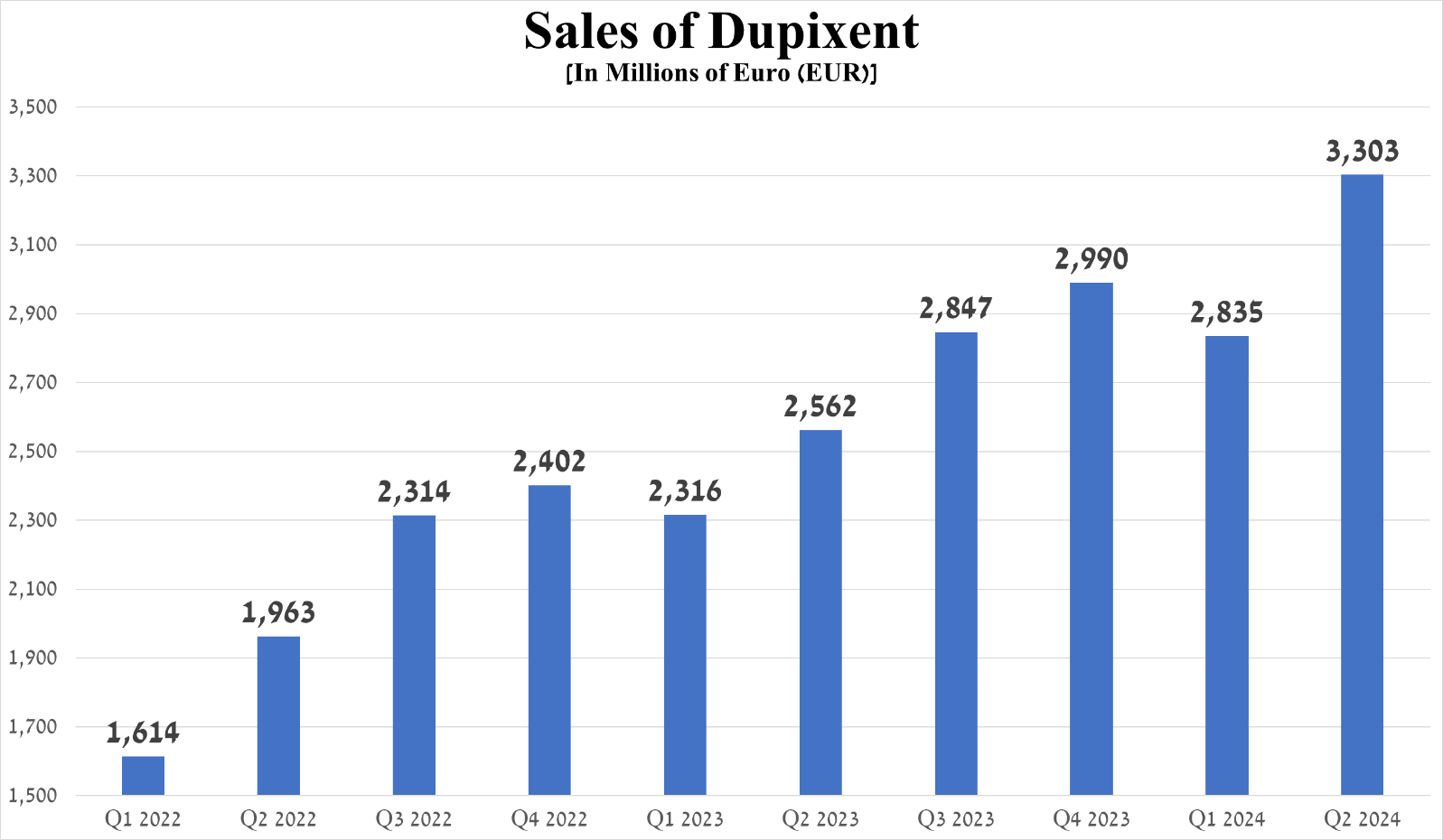

Dupixent (dupilumab) is an anti-IL-4Rα monoclonal antibody developed in partnership with Regeneron Pharmaceuticals (REGN) and widely used to combat a broad range of immune-mediated inflammatory diseases, highlighted in the table below.

Source: table was made by Author based on Sanofi press releases

Its sales exceeded the €3 billion mark for the first time in the company's history, reaching €3.03 billion in the second quarter of 2024, up 28.9% year-on-year and 16.5% quarter-on-quarter.

Source: graph was made by Author based on Sanofi’s financial reports

What are the reasons for Dupixent's commercial success?

Firstly, the demand for Sanofi's blockbuster was provided by extremely high demand from patients suffering from atopic dermatitis, eosinophilic esophagitis, and asthma.

In addition, since the beginning of 2024, its label has been expanded for two indications in the United States, which, together with additional promising clinical data published at the end of February of this year, played a key role in increasing the growth rate of Dupixent sales both year-on-year and quarter-on-quarter.

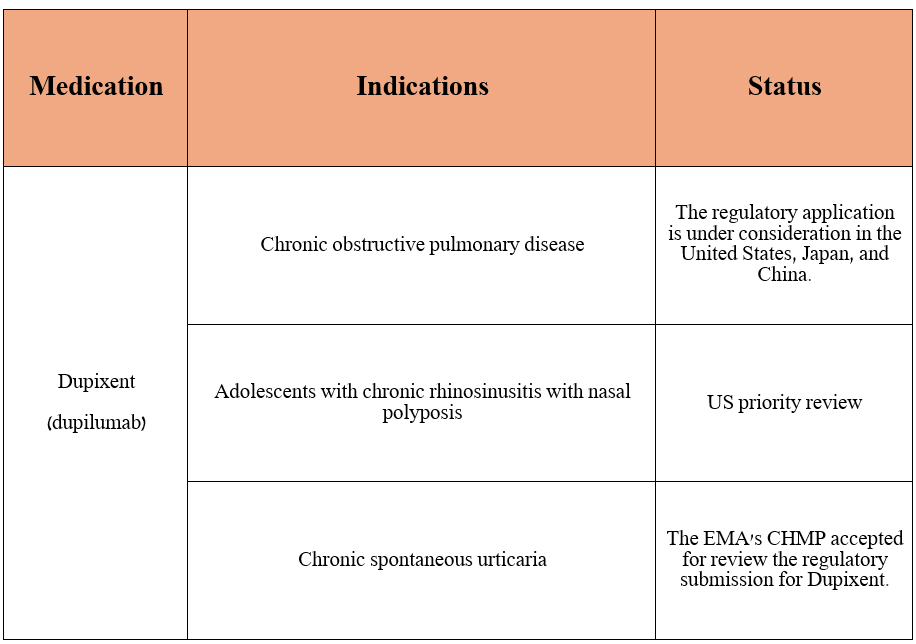

Should investors expect label expansions for Dupixent in 2024/2025?

The short answer is yes.

In addition, I want to note that this is an important question since the correct answer to it, first of all, allows investors to understand from which quarter they should expect an acceleration in the growth rate of sales of Sanofi's medication, and also, if it is approved by regulatory authorities, will lead to a revision of analysts' forecasts for its peak sales upward.

So, the French pharmaceutical giant is not resting on its laurels and is looking to expand the indications for Dupixent.

Source: table was made by Author based on Sanofi press releases

In the table above, I have highlighted key milestones that will help broaden the eligible patient population for the medication, which will ultimately strengthen its position in the global anti-inflammatory therapeutics market until it loses market exclusivity.

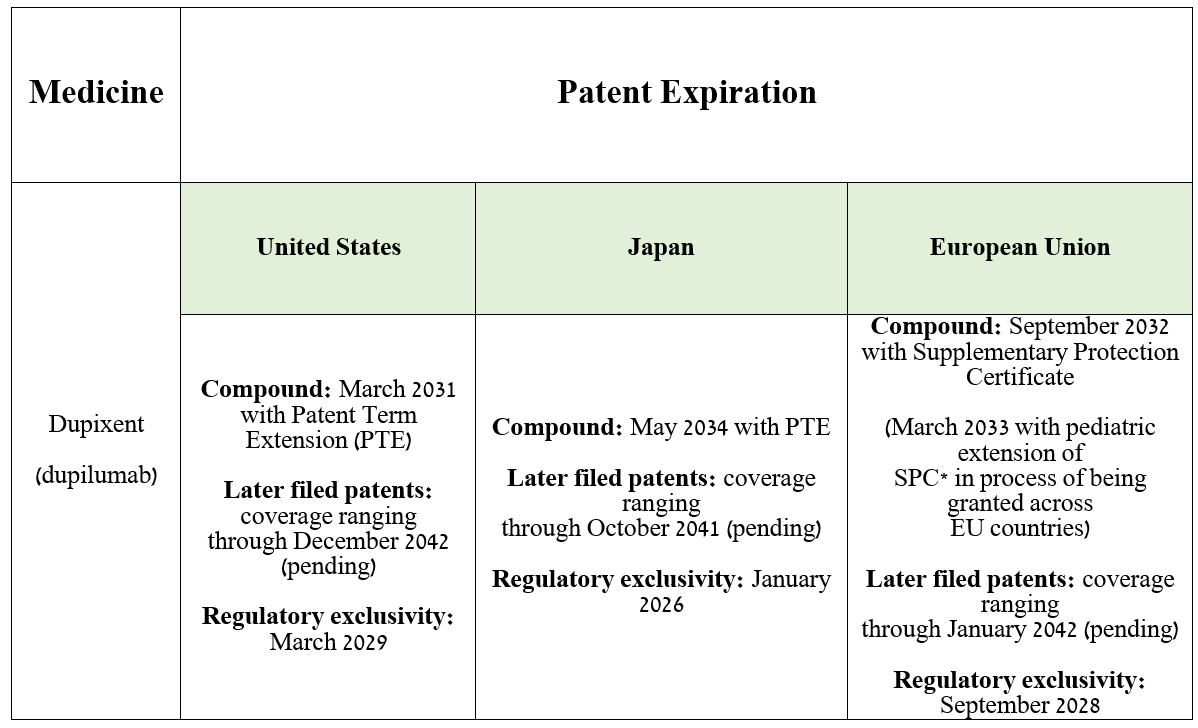

Source: table was made by Author based on Sanofi’s 20-F

After discussing the progress in Dupixent's development, logical questions arise.

What other Sanofi medications have contributed to beating the analyst consensus estimate, and which will continue to make a significant contribution to improving its margins and revenue growth in the long term?

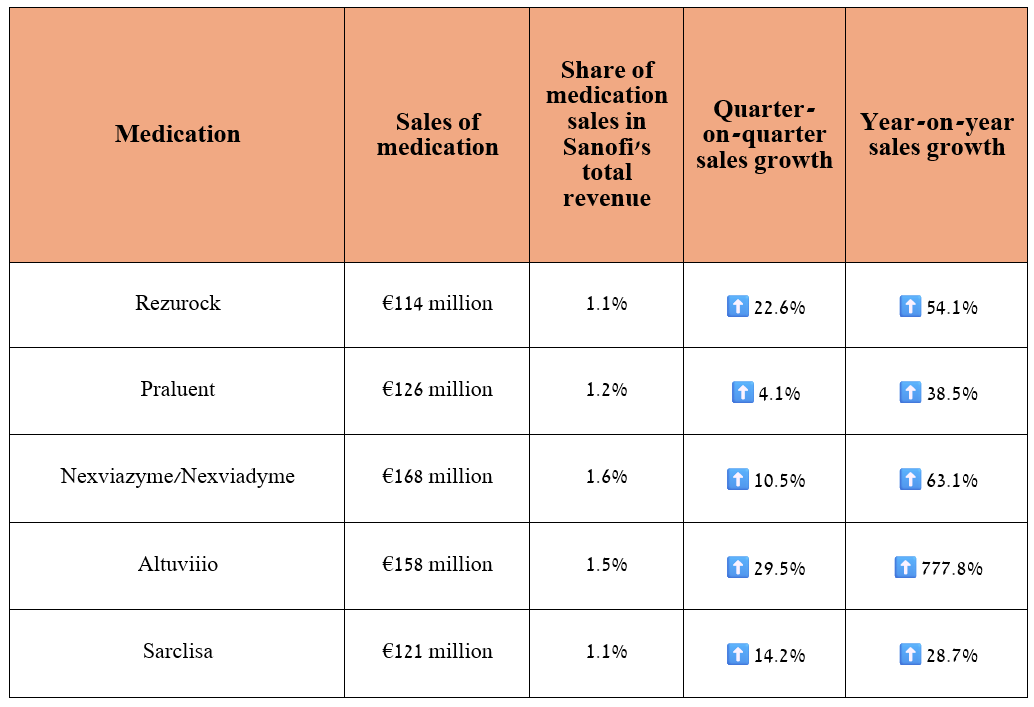

In addition to Dupixent, which I discussed earlier in the article, I believe that Rezurock, Praluent, Nexviazyme/Nexviadyme, Altuviiio, and Sarclisa are the medications that will continue to have a notable impact on improving Sanofi's financial position in the long term.

Source: graph was made by Author based on Sanofi’s financial reports

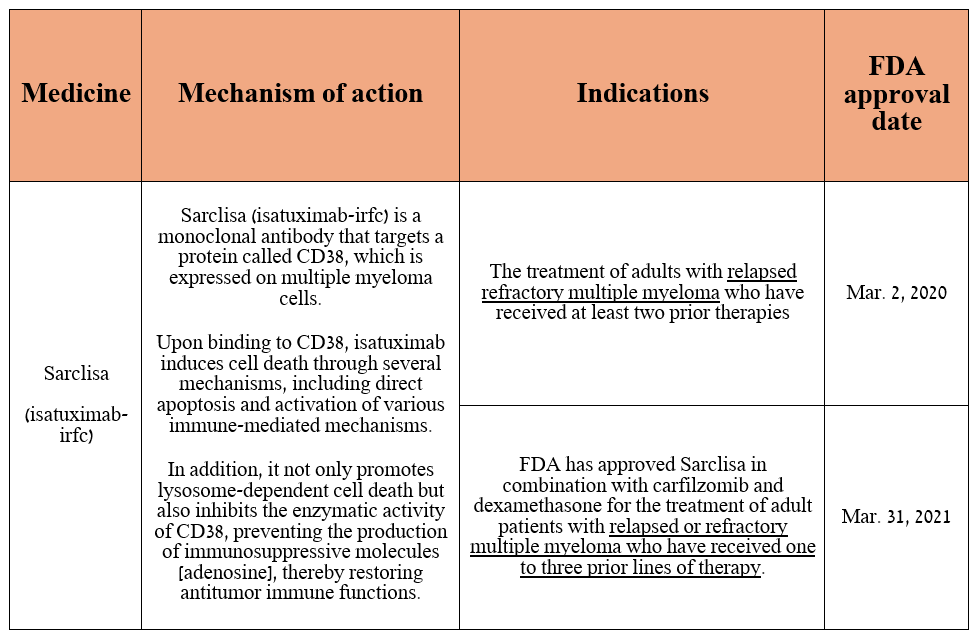

Dear Seeking Alpha readers, let's continue our journey by discussing Sarclisa (isatuximab-irfc). It is an anti-CD38 monoclonal antibody approved by the EMA, FDA, and other regulators in combination with certain drugs, including pomalidomide [thalidomide analogue], carfilzomib [irreversible proteasome inhibitor] and dexamethasone [glucocorticoid] for the treatment of people with multiple myeloma.

Also, I have described Sarclisa's mechanism of action in simple terms in the table below, which will allow some of you to better understand how it works.

Source: table was made by Author based on Sanofi press releases

As I said in the article "Gilead Sciences: Buy This Bargain Before It's Gone," understanding the mechanism of action of medication helps me further evaluate how effective it will be, the likelihood of life-threatening side effects, and the potential for label expansion. Eventually, these factors play a key role in the growth rate of its sales, which the pharmaceutical company spent hundreds of millions of dollars on developing.

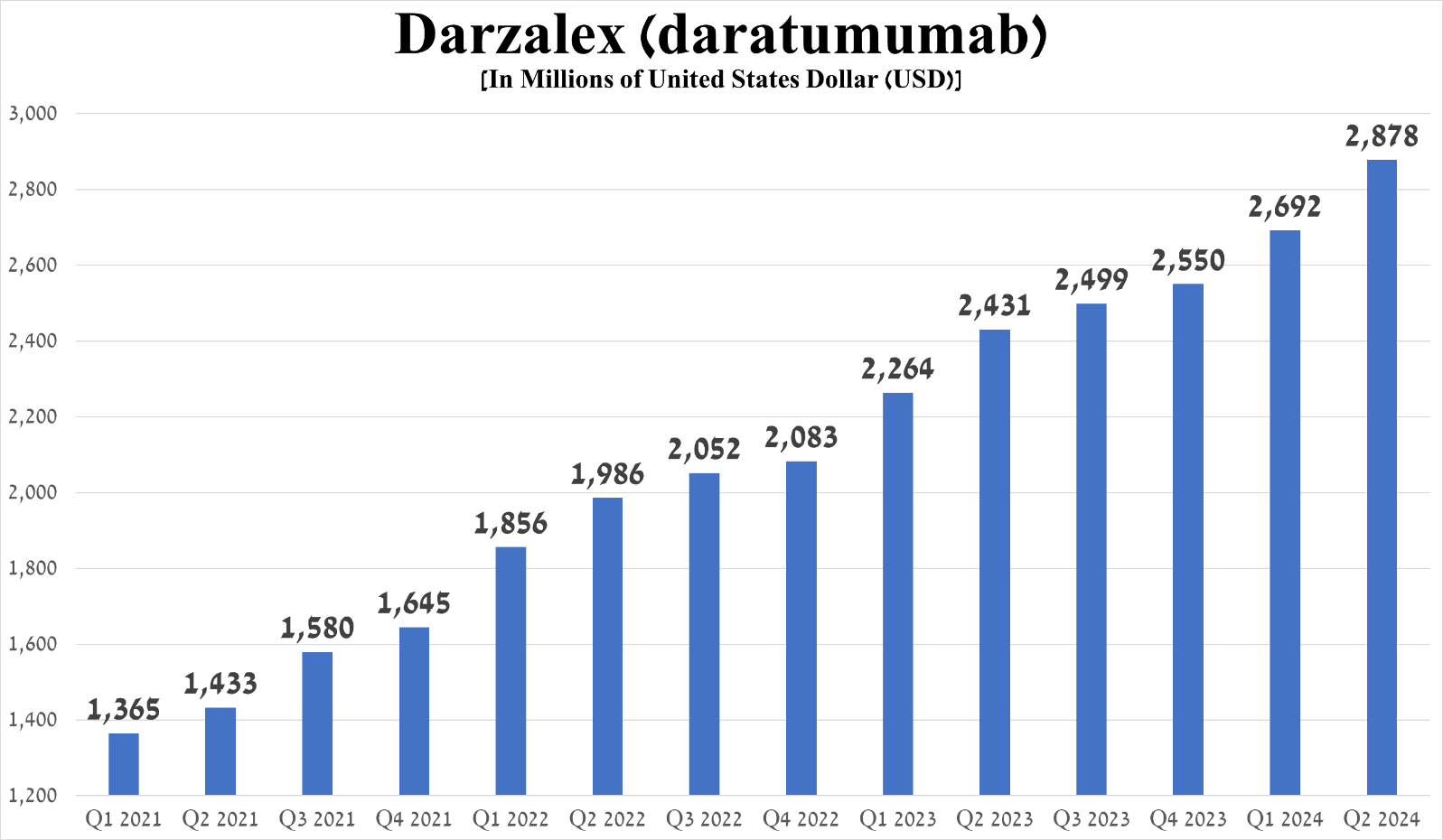

Also, when determining the prospects of a drug, I pay attention to its competitors within the same class. So, the closest competitor is Johnson & Johnson's Darzalex (JNJ), approved for an extremely wide range of indications for use and whose sales amounted to about $2.88 billion in the second quarter of 2024, an increase of 18.4% year-on-year.

Source: graph was made by Author based on 10-Qs and 10-Ks

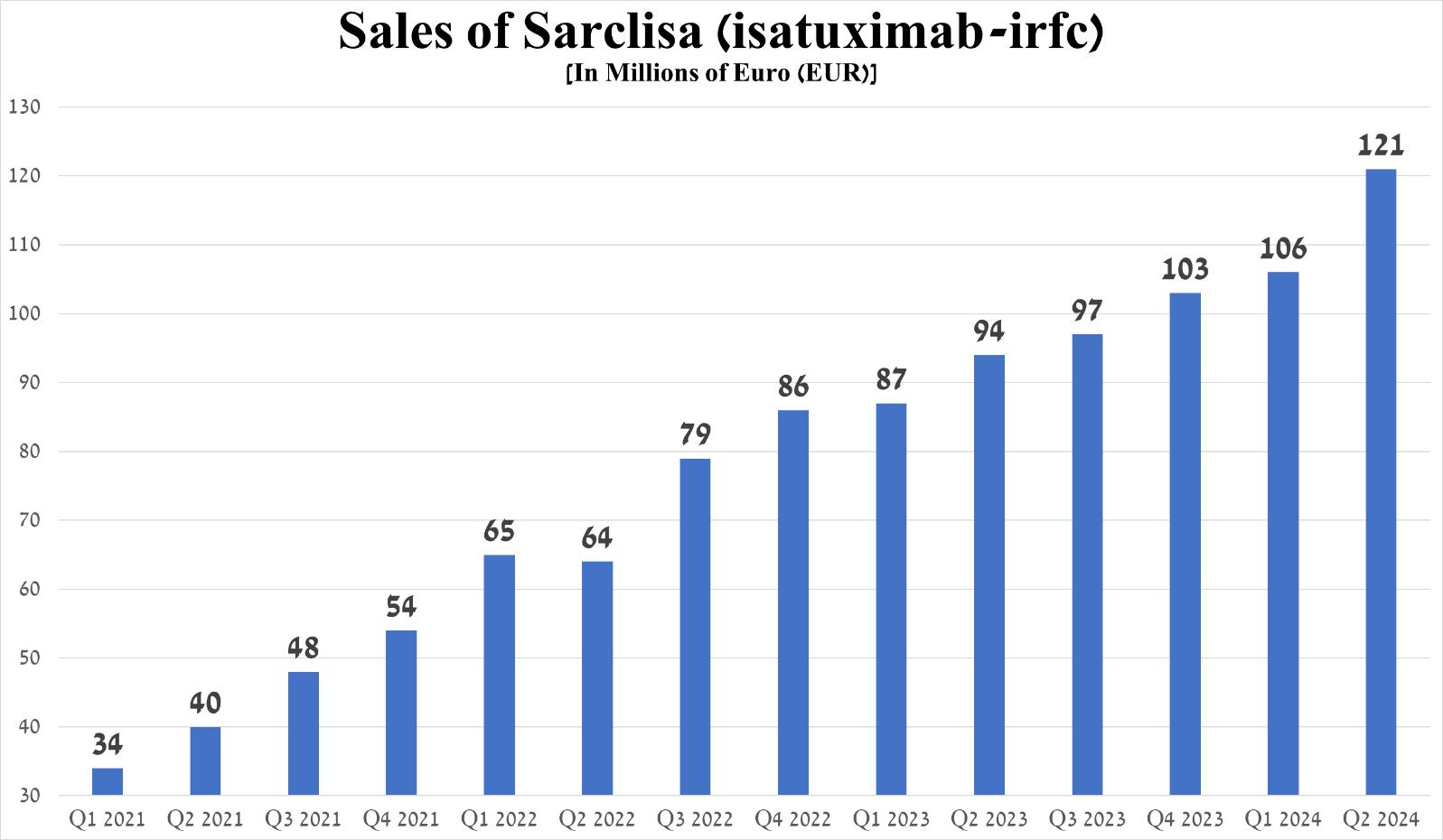

As a result, this information is the first significant signal that Sarclisa has a bright future. However, a more detailed explanation of why I believe this will be presented later.

From the launch of Sarclisa until the first quarter of 2024, its sales showed a steady positive trend, but its growth rate accelerated in the second quarter of 2024.

So, its revenues amounted to 121 million euros, an increase of 14.2% quarter-on-quarter and 28.7% year-on-year, primarily due to strong demand for it in the US and Japan, the expansion of the global multiple myeloma therapeutics market, as well as its competitive advantages compared to Bristol-Myers Squibb's Empliciti (BMY).

Source: graph was made by Author based on Sanofi’s financial reports

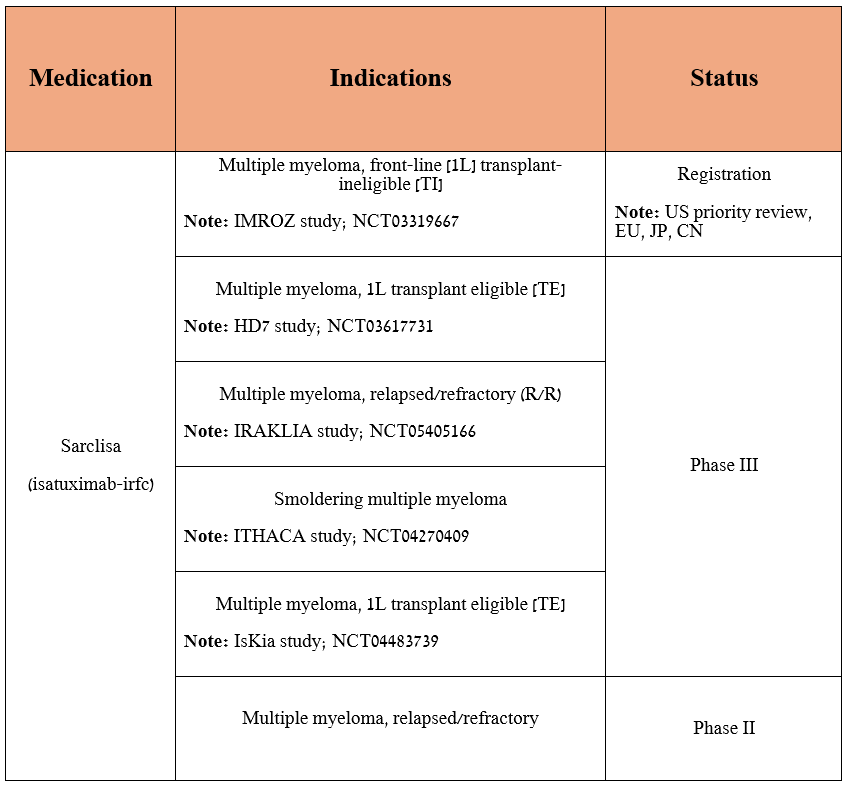

In addition, Sanofi is not resting on its laurels following the progress made in the Sarclisa development program and is continuing to evaluate its efficacy in treating a broader population of patients with multiple myeloma.

It is equally important to note that isatuximab is currently approved only in the form of intravenous infusions, and in order to improve the quality of life of patients and speed up its introduction into medical practice, the company is conducting a pivotal clinical trial evaluating a subcutaneous version of the medication.

Source: table was made by Author based on Sanofi' pipeline/ClinicalTrials.gov

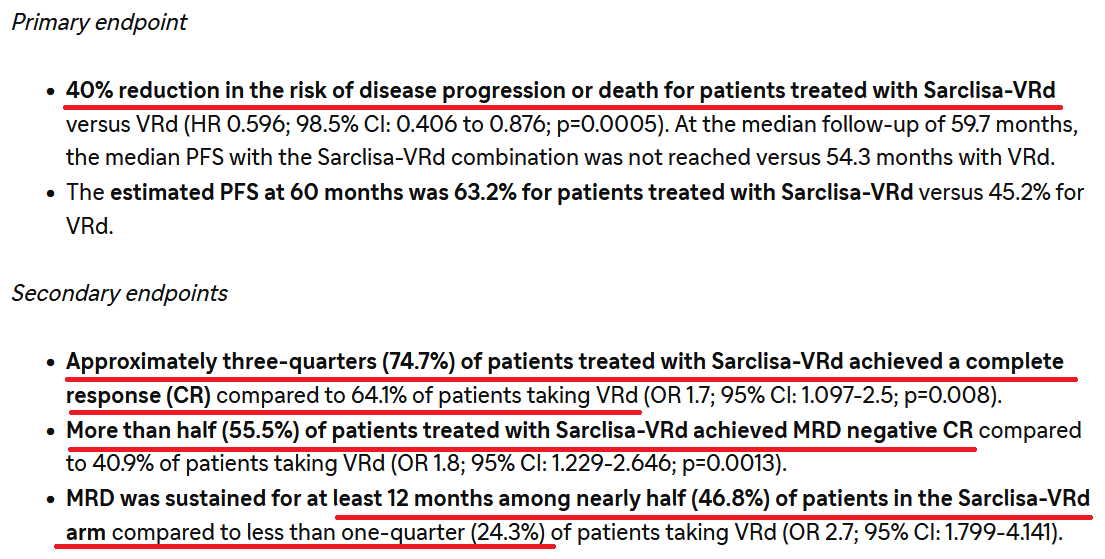

By the end of Q3 2024, I expect the FDA to approve the combination of Sarclisa with standard-of-care [lenalidomide, bortezomib, and dexamethasone] for the treatment of transplant-ineligible newly diagnosed multiple myeloma based on the extremely promising results of the Phase 3 IMROZ clinical trial, which met both primary and secondary endpoints.

Source: Sanofi

Before discussing the financial risks that existing investors or those considering Sanofi as a long-term investment should take into account, I want to highlight its progress in commercializing two drugs in its rare diseases' portfolio.

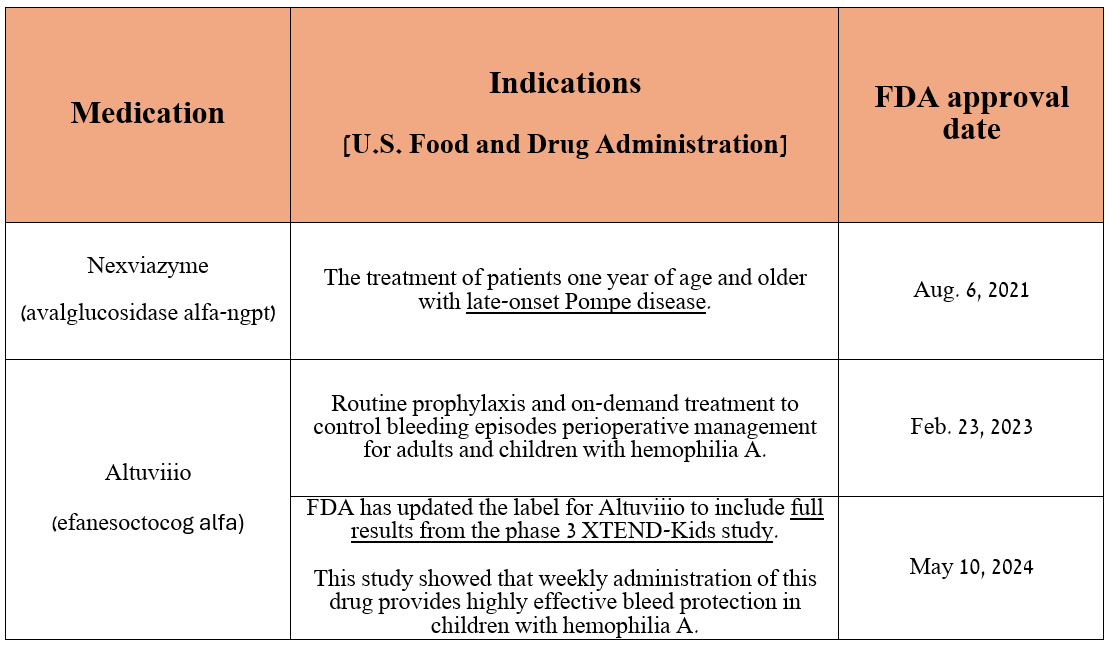

The first of these is Altuviiio, which is a recombinant factor VIII replacement therapy approved by the FDA and EMA for the treatment of patients suffering from Hemophilia A, which in turn is a rare bleeding disorder that mainly affects men. According to Orphanet, its prevalence is estimated at 1 in 6,000 males.

The second is avalglucosidase alfa, whose brand name is Nexviazyme in the U.S. and Nexviadyme in Europe. It is an enzyme replacement therapy used to treat late-onset Pompe disease. This rare disorder is caused by a buildup of glycogen in human cells, leading to progressive muscle weakness, and can be fatal if left untreated. According to MedlinePlus, it affects about 1 in 40,000 Americans.

Source: table was made by Author based on Sanofi press releases

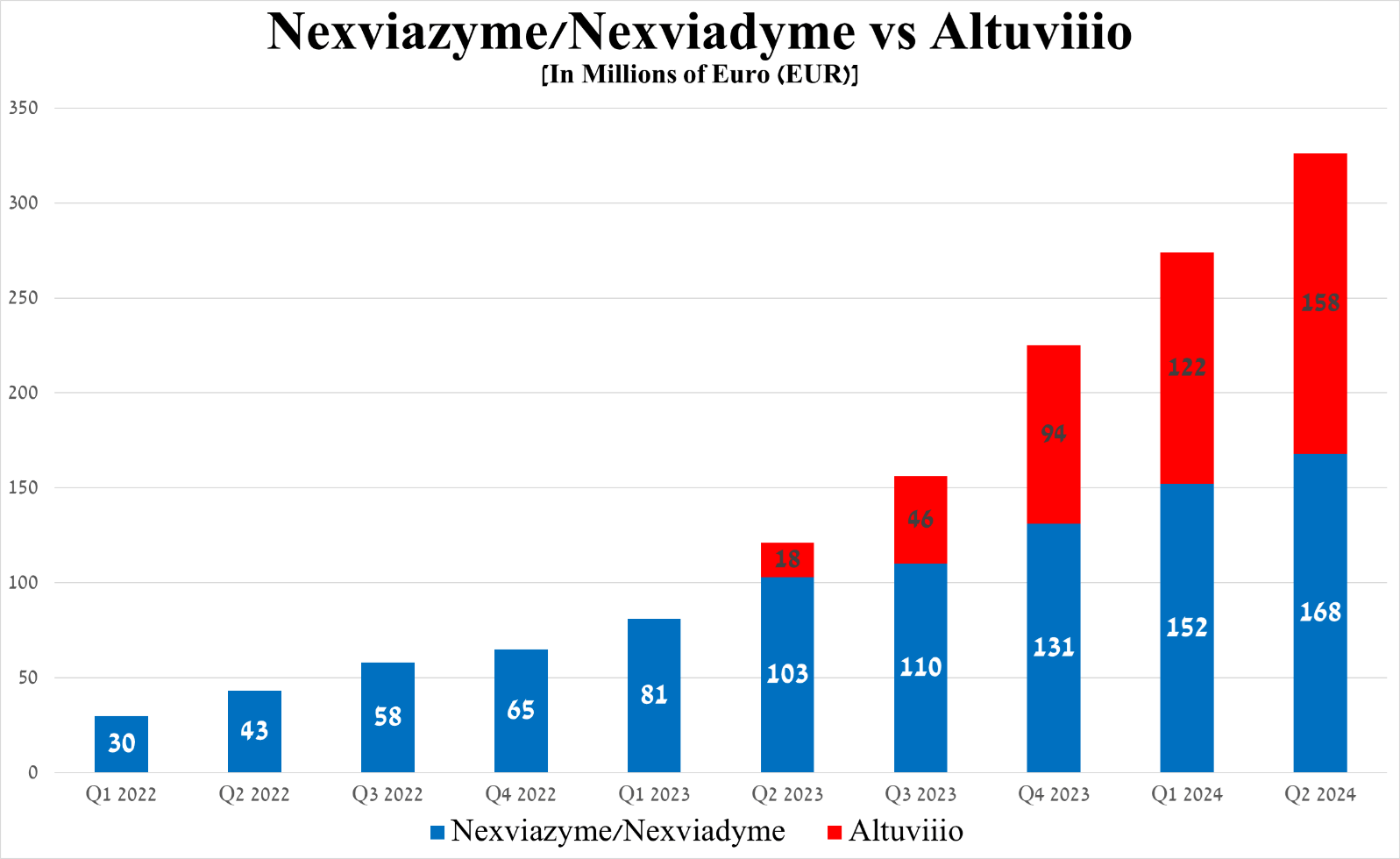

Combined sales of the two medicines were €326 million for the three months ended June 30, 2024, up 169.4% year-on-year and 19% quarter-on-quarter, driven primarily by the patients switching from Myozyme/Lumizyme to Nexviazyme/Nexviadyme, as well as Altuviiio's competitive advantages, including its once-weekly administration and its demonstrated ability in clinical trials to maintain factor VIII levels above 40% in most patients with hemophilia A.

Source: graph was made by Author based on Sanofi’s financial reports

Risks

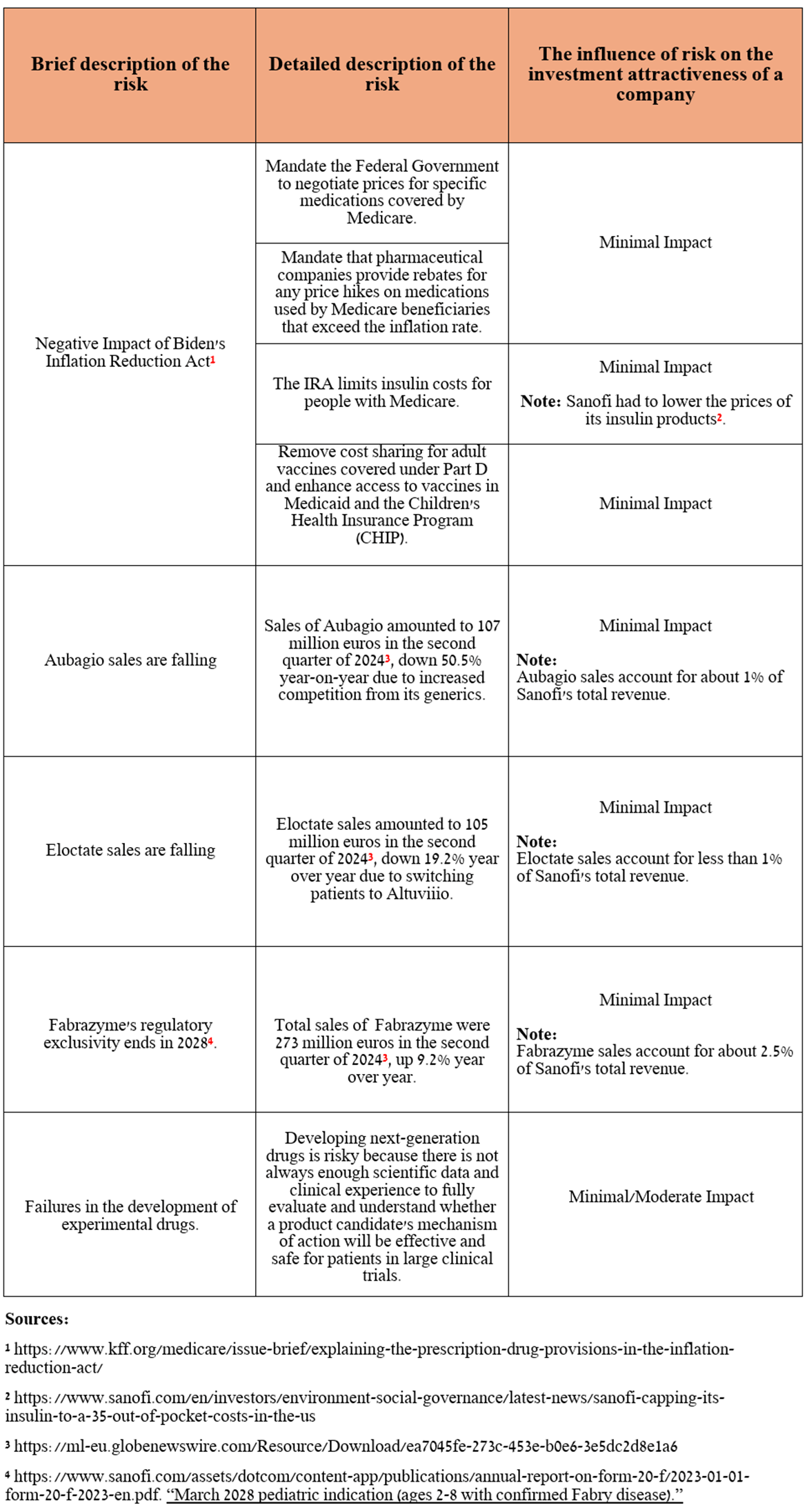

In addition to the risks outlined in my last article about Sanofi, I also want to point out that, despite the growth in sales of Fabrazyme, which is a drug approved by the FDA to treat patients with Fabry disease, its regulatory exclusivity in the US ends in 2028, which will eventually lead to the launch of its biosimilars.

Source: table was made by Author

Takeaway

On July 25, Sanofi reported financial results for the second quarter of 2024, which beat Wall Street analysts' expectations even as competition in the global insulin market intensifies.

Thanks to strong sales of the oncology and rare diseases franchises, the expected label expansions for Dupixent and Sarclisa, and the strengthening of the euro against the US dollar, the company's management raised the full-year 2024 EPS guidance.

Based on our current performance in the first half of the year, on a strong business outlook for the remainder of the year, we upgrade our earnings per share guidance for 2024 to stable at constant exchange rates.

In addition, the Paris-based company has a relatively high dividend yield of 3.6%, its operating income continues to grow year-on-year, and the acquisition of Inhibrx allowed Sanofi to strengthen its position in the global alpha-1 antitrypsin deficiency treatment market.

Combined with the above factors, and also taking into account its rich portfolio of experimental drugs, many of which have the potential to become "gold standards" in the treatment of common diseases such as ulcerative colitis, asthma, psoriasis, and atopic dermatitis, I continue to cover Sanofi with a 'Buy' rating.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.