KingWu

We initiated our coverage of Canadian oil major Cenovus Energy (NYSE:CVE) in April when we outlined our favorable view on the company given 1) a deep and durable portfolio benefitted by tightening WTI/WCS spreads and 2) the company being on track to distribute 100% of FCF to shareholders, leading us to name it as our top pick among Canadian oils. While shares have (slightly) underperformed its wider North American peers and (significantly) underperformed its Canadian peers Suncor and Imperial, we continue to see a favorable setup as mgmt hit its net debt target during Q2 and CVE's valuation discount grew further.

Being on track to distribute 100% of FCF from this Q onwards, we reiterate our Overweight rating on Cenovus and view it as a key potential outperformer among North American oils. We marginally raise our SOTP-based price target from $34 to $35 per US ADR, implying ~78% current upside. Key risks remain in broader energy market downturns, as well as additional regulatory hurdles for oil and gas producers in Canada.

[Note: Canadian peers are Suncor (SU) and Imperial (IMO). US peers are Exxon (XOM) and Chevron (CVX). All financials in C$ if not indicated otherwise, price target refers to US listed shares.]

Key Discussion Points

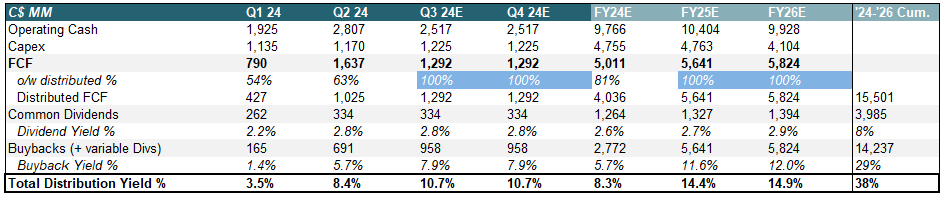

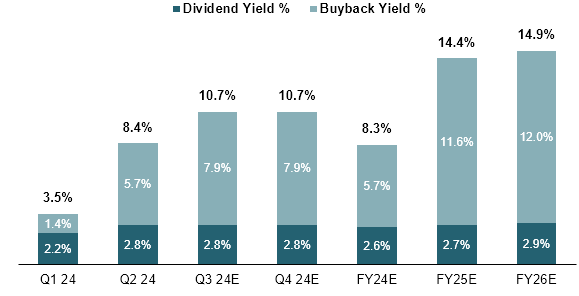

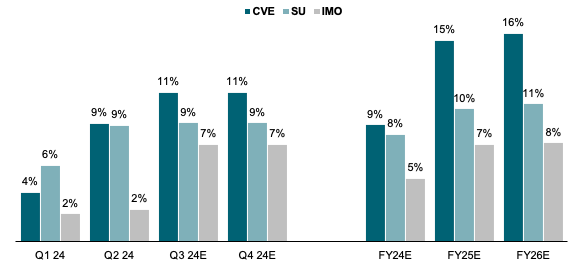

With net debt target reached, 100% of FCF is now distributed for a 13-15% annual yield through 2026. Cenovus achieved its targeted level of C$4B in net debt during Q2, implying a 100% FCF payout ratio from Q3 onwards. While buybacks (and variable divs) have yielded 1% and 6% during Q1 and Q2 respectively, we estimate this to rise to ~11% through H2 as we see around $1B in buybacks/quarter. For the full fiscal year, we calculate that this implies a ~8.3% cash yield from dividends and buybacks.

Company Filings, WSR Estimates

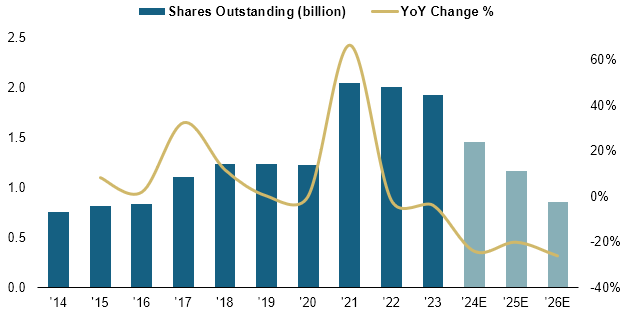

While this year, however, was impacted by a lower yielding H1 which saw only about ~60% FCF distributed to shareholders, we see a significant expansion from next year onwards. Assuming consensus FCF figures and a 100% distribution ratio with ~5% annual dividend/share growth, we forecast distribution yields for 2025 and 2026 rising to ~14.4% and ~14.9% respectively. The majority of this will be driven by share buybacks, with Cenovus buying back ~12% of outstanding stock per year, enabling the company to retire roughly 40% of current shares by YE26 as per our calculations.

WSR Estimates

This would bring sharecount down to ~800MM, a figure last seen around 2016 and remove the dilutive impact on EPS and FCF/sh that we had seen following the mid-2010s oil price crash and Covid.

Company Filings, WSR Estimates

When compared to its key Canadian peers Suncor and Imperial Oil, Cenovus' shareholder return potential screens as significantly ahead with CVE's 11.4% annualized distribution expected for Q3 and Q4 vs Suncor at ~9% and Imperial at ~7%. Going into 2025 and 2026, with Suncor expected to hit its net debt target by Q1/2 25 and at consensus FCF estimates, we see CVE's outyear cash yield ~5pp higher and significantly above Imperial.

Distribution Yield (WSR Estimates)

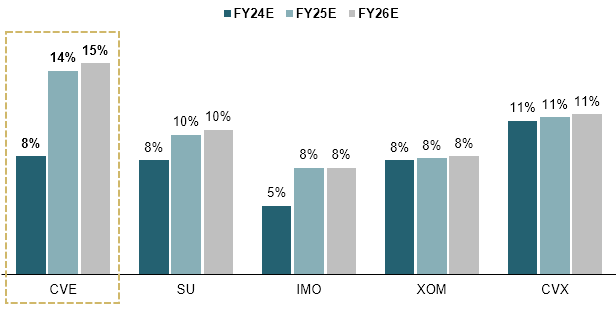

Also, comparing annualized yields to the American majors Exxon and Chevron, Cenovus' distribution potential continues to exceed peers by a wide margin. While the large North American oil majors pay out ~9% of their market cap on average through 25E and 26E, Cenovus' yield is almost 50% above that on both a highly accommodating payout policy and a relatively discounted equity valuation. With the oil industry largely defined by its ability to return capital to shareholders, we continue to view CVE's as a key long in the sector.

Total Distribution Yield (WSR Estimates)

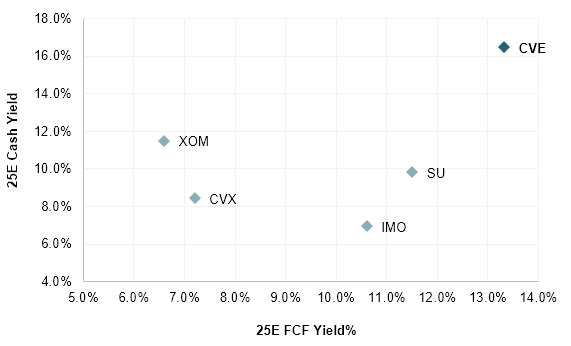

FCF yield of >12% implies an attractive valuation/distribution framework vs Canadian and US peers. On 25E FCF consensus estimates, Cenovus shares currently trade at a ~12.5% yield, implying a significant discount vs the broader NA major average of ~9% while on the other hand, distributions of ~16.5% are almost 80% above the ~9% group average. Risk/reward has also improved considerably relative to its Canadian key peers in light of recent share price underperformance. At a 12.5% FCF yield, CVE now screens as ~20% cheaper than Suncor and Imperial, while shareholder returns are at a roughly double rate.

Bloomberg, WSR Estimates