Monty Rakusen

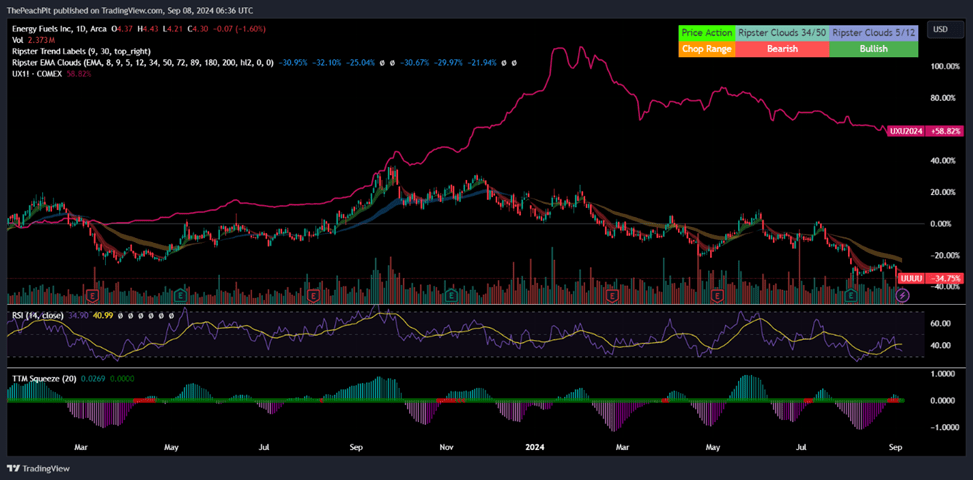

Uranium has been taking a turn off the high watermark of ~$105/lb in January 2024 and has since settled in the low-$80s. Energy Fuels’ (NYSE:UUUU) (TSX:EFR:CA) shares have directionally followed the trend, given the firm’s split between long-term sales agreements and spot sales. Looking at the price trend for uranium futures, Energy Fuels may experience some additional downside throughout the duration of the year, despite the firm’s aggressive shift towards increasing production to 1.1-1.4mm pounds per year by the end of 2024. Long term, I believe Energy Fuels will be well-positioned as one of the main sources of domestic uranium and rare earth elements (“REE”) production; however, I believe the company’s stock will route lower in the short-to-mid-term given demand will likely remain relatively stagnant through the end of the decade. Given these factors, I am rerating UUUU shares with a HOLD rating with a price target of $4.10/share at 70.30x eFY25 EV/EBITDA.

TradingView

Energy Fuels Operations

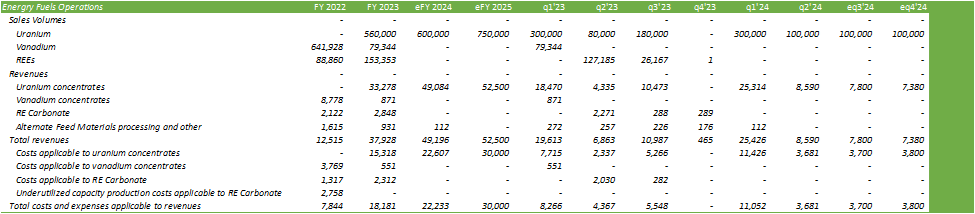

Energy Fuels is in a strong position with multiple revenue streams that span across the renewable energy sector, including uranium, REEs, monazite, and other byproducts that fall into their production process. Management voiced the transition of the firm’s White Mesa Mill back to uranium processing, which should be readily available by October 2024, in order to build their stockpile of processed uranium. At the end of q2’24, Energy Fuels had nearly 1mm pounds of processed and unprocessed materials on hand, 285,000 pounds of which is processed uranium available for sale. Energy Fuels sold 100,000 pounds of uranium on the spot market at $85.90/lb and has a long-term sales agreement in place with the potential of an additional 100,000 pounds of uranium for sale with a US-based utility.

Management’s current plan for the organization is to lean into uranium mining and processing, with the intent of mining 1.1-1.4mm pounds of uranium per year by the end of 2024. Longer-term, management anticipates having the capacity to produce 2mm pounds of uranium through the commencement of the Nichols Ranch ISR location. The firm is currently developing three additional locations for potential production, including Sheep Mountain in Wyoming, Roca Honda in New Mexico, and Henry Mountains – Bullfrog Project in Utah. Management forecasts that these three projects have a combined resource of 70mm pounds of uranium for production and may allow for Energy Fuels to produce upwards of 6mm pounds of uranium per year.

One factor that was mentioned on the q2’24 earnings call was that management signed their 4th long-term contract with a US utility. What brings a certain appeal to this contract is that it was signed with a shorter duration when compared to their other SPAs. The rationale for this appeal is that the contract can be renegotiated and repriced when lapsed and allow for a more appealing price if spot uranium prices tick up at the time of renewal. Though this may appear as a risky move on Energy Fuel’s strategy given the historical volatility in uranium spot prices, the strategy may hold value given the growing interest for SMRs, or small modular reactors, which should enter the market at the turn of the decade. At this time, I believe China is the only country that has SMRs under development; however, there are a few domestic companies that are developing the technology for production.

Cameco (CCJ) acquired Westinghouse Electric Company at the end of 2023, which includes their nuclear-related technology and services business, bringing in their SMR technology. GE Vernova (GEV) is also developing SMR technology, which is said to be more cost-effective than the traditional reactor and can be constructed in as little as 24-36 months.

For the most part, I believe the long-term investment outlay for the uranium industry is appealing. Reuters has reported that demand for uranium as an energy source is expected to increase from 65,650 tonnes per year to 83,840 tonnes by 2030 and 130,000 tonnes by 2040.

Taking into consideration management’s investment strategy, I believe that it will play out to the firm’s benefit in which Energy Fuels will produce and process to stockpile uranium and opportunistically sell the finished goods on the spot market or through their SPAs.

In addition to uranium, Energy Fuels has been adamant in developing their REE resources for domestic production of magnets and other components found in electric vehicles, windmills, and aerospace & defense. Though this will likely be another long-term strategy, the short-term economics remain challenged.

Trading Economics

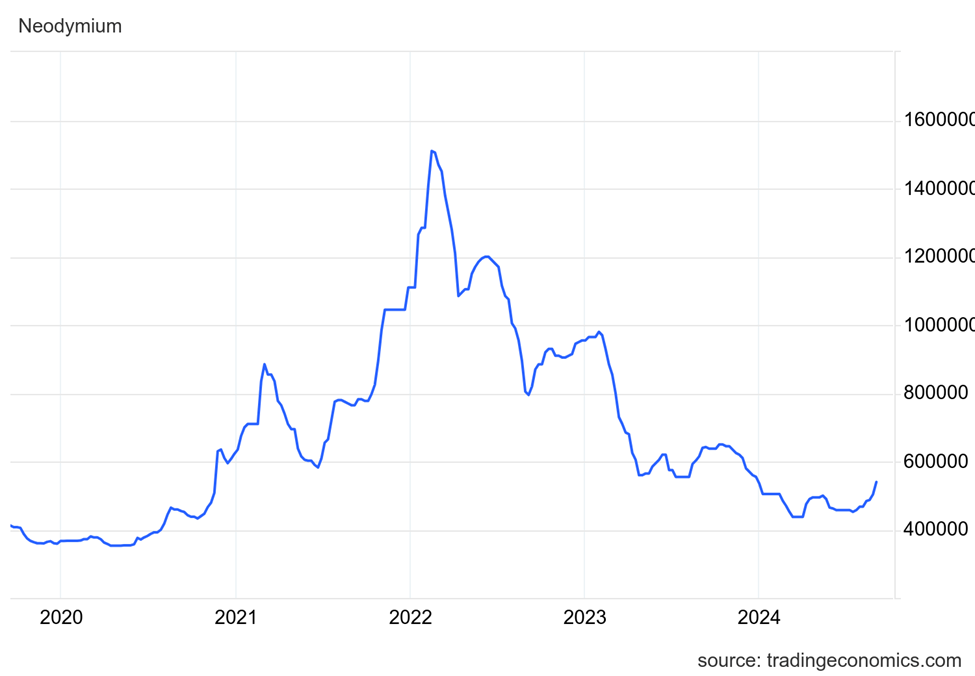

The market for NdPr cratered at the end of 2022 going into 2023 as China increased their production quotas by 20%, resulting in a surplus of materials on the market. The Goldman Sachs analyst cited in the report anticipated demand to outpace supply by 2028; however, I believe that the forecast is now dated given the declining interest in electric vehicles both by consumers and automotive OEMs. As of recent, Ford (F) has backpedaled from their EV initiatives and canceled plans for their 3-row SUV in favor of smaller EVs. Volkswagen (OTCPK:VWAGY) also considering reducing their EV exposure due to anticompetitive pricing from Chinese OEMs. AB Volvo (OTCPK:VLVLY) is falling into the same boat as the firm abandons their 90-100% exposure to EV sales by the end of the decade. In addition to this, BMW (OTCPK:BMWYY) and Toyota (TM) are partnering to develop hydrogen-fueled vehicles with production by 2028.

This could pose a challenge for NdPr demand outside of China. Given that China is flush with REEs, I do not believe that Energy Fuels will have market share to gain within the country. This is in addition to the trade restrictions between the US and China as it pertains to REEs.

Given these factors, I believe that management has made the right decision to transition the White Mesa Mill back to uranium processing to cater to the nuclear power industry.

On August 19, 2024, Energy Fuels acquired RadTran, LLC, a private company that specializes in the separation of critical radioisotopes that are used for medical isotopes in cancer treatments. The firm’s expertise includes separating radium-226 and radium-228 from uranium and thorium process streams. The two firms have been working together since July 2021 to evaluate the feasibility of recovering these two isotopes from existing process streams at Energy Fuel’s White Mesa Mill. Energy Fuels anticipates commercial-scale production of these two isotopes sometime between 2026-2028. The deal was closed at $3mm in value, split evenly between cash and equity.

Energy Fuels Financials

Corporate Reports

For the first half of 2024, Energy Fuels has sold a total of 400,000 pounds, 200,000 pounds of which were under a fixed price agreement and 200,000 pounds at spot. The firm has not sold any additional materials YTD, which is likely due to the challenged commodity prices.

Corporate Reports

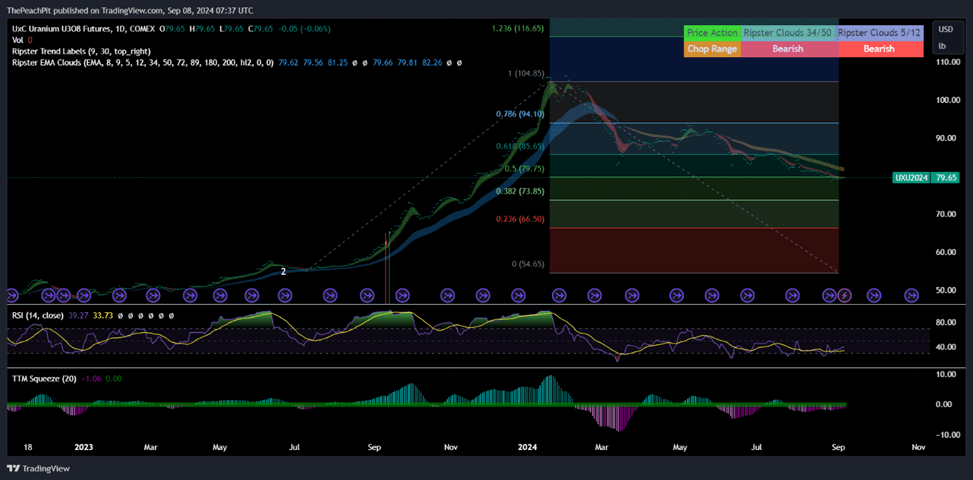

Forecasting the duration of eFY24, I anticipate Energy Fuels will sell an additional 100,000 pounds of uranium per quarter, resulting in 600,000 pounds sold throughout all of eFY24. Given the current spot price at sub-$80/lb, I anticipate further pricing pressure throughout the duration of the year, with spot uranium prices potentially touching $73/lb.

TradingView

If spot uranium prices continue this trajectory, Energy Fuels may experience a decline in revenue as a result of the softer selling price. I believe that this will result in a loss for the remaining two quarters in eFY24, with eq3’24 diluted EPS coming in at -$0.06/share.

Risks Associated With Energy Fuels

Bull Case

The long-term outlook is positive for Energy Fuels as the company is well-diversified across multiple nodes as it pertains to the next generation of clean energy. Uranium demand is expected to improve through 2030, primarily driven by the ramp-up of regional SMRs for localized power. REEs may grow in demand domestically as well if electric vehicle demand picks back up towards the end of the decade.

Bear Case

Spot uranium may be going through a downcycle towards the end of the year as the commodity cools off from its recent peak price in January 2024. Considering that spot uranium is generally priced by bankers and traders, spot prices generally follow Elliot Wave Theory as part of the technical trading trends. If spot uranium is to follow these trends, I believe spot prices will fall to $73/lb by the end of 2024, resulting in a decline in revenue for Energy Fuels as a result of potential spot sales. REEs continue to face pricing pressure and may not recover to profitability in the near-term.

Valuation & Shareholder Value

Corporate Reports

UUUU shares currently trade at 5.68x price/book value of mineral assets. From a company comps perspective, UUUU shares trade at a discount to its peers when comparing price to total book value. This might make UUUU shares more of a value strategy when compared to its comparable company cohort.

Seeking Alpha

Taking into consideration Energy Fuel’s cash generation, I believe that shares may be slightly overpriced based on their current valuation. Though my valuation model calls for a -5% decline from the current price level, I do believe that Energy Fuels’ long-term strategy makes the company an appealing asset to hold. Given the near-term price volatility, I am rerating UUUU shares with a HOLD with a price target of $4.10/share at 79.30x eFY25 EV/EBITDA.

Corporate Reports