Everyday better to do everything you love/iStock via Getty Images

Investment Thesis

BlackBerry (NYSE:BB) has reached a point where I believe it's now fairly priced. More specifically, as I discuss here, it's not as important what its fundamentals are like right now.

What matters is what the future investor will think about next year. They'll see a business with more than 15% of its market cap made up of cash, with no debt. Perhaps, the icing on the cake may be that its business has mostly pivoted towards IOT and cybersecurity and has some tangible figures to support its narrative.

Therefore, I now upwards revise my sell rating to neutral.

Rapid Recap

I opened my previous analysis back in June by saying:

BlackBerry's stock jumps 8% premarket on the back of its fiscal Q1 2024 report.

And yet, I remain bearish on this stock. I contend that this cheer from investors is little more than a relief rally that its earnings results weren't worse.

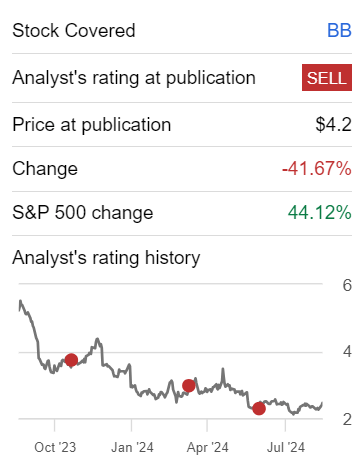

BB is a stock that I've been consistently bearish on for a long time. In that time, the stock has underperformed the S&P 500 by a wide margin, as you can see below.

Author's Work on BB

But now, as I appraise its prospects, I believe that the stock is fairly valued.

BlackBerry's Re-Positioning Into IOT and Cyber

BlackBerry has undergone a significant transformation, now focusing on two key areas: Internet of Things and cybersecurity.

In the IoT space, BlackBerry is making a big impact through its QNX platform, which serves as the operating system for over 235 million vehicles worldwide. This platform plays a critical role in running the software that powers modern cars, giving BlackBerry a solid foothold in the automotive industry.

On the cybersecurity front, BlackBerry continues to build on its legacy of secure communications through its unified endpoint management and advanced AI-driven security solutions like Cylance. Together, these two business divisions position the company for future growth and profitability.

As keen followers will know, following a leadership change in December 2023, BlackBerry took decisive steps to streamline its operations and focus more narrowly on IoT and cybersecurity. This shift has already shown positive results, with $125 million in cost reductions and a clearer vision for profitability. The new leadership has brought a fresh focus on driving growth in these two areas while cutting unnecessary expenditures. This renewed clarity and strategic direction could potentially lead to stronger business performance, making the leadership change a positive development for the company.

And yet, BlackBerry may face challenges in gaining market share against competitors like Samsara (IOT), which is already generating over $1 billion in annual revenue and growing at a strong rate of over 30% compound annual growth (CAGR). Samsara's ability to rapidly scale its business, paired with its path toward achieving 8% free cash flow margins, gives it a competitive advantage. (Disclosure: Deep Value Returns is long IOT).

Given this balanced background, let's now discuss BlackBerry's fundamentals.

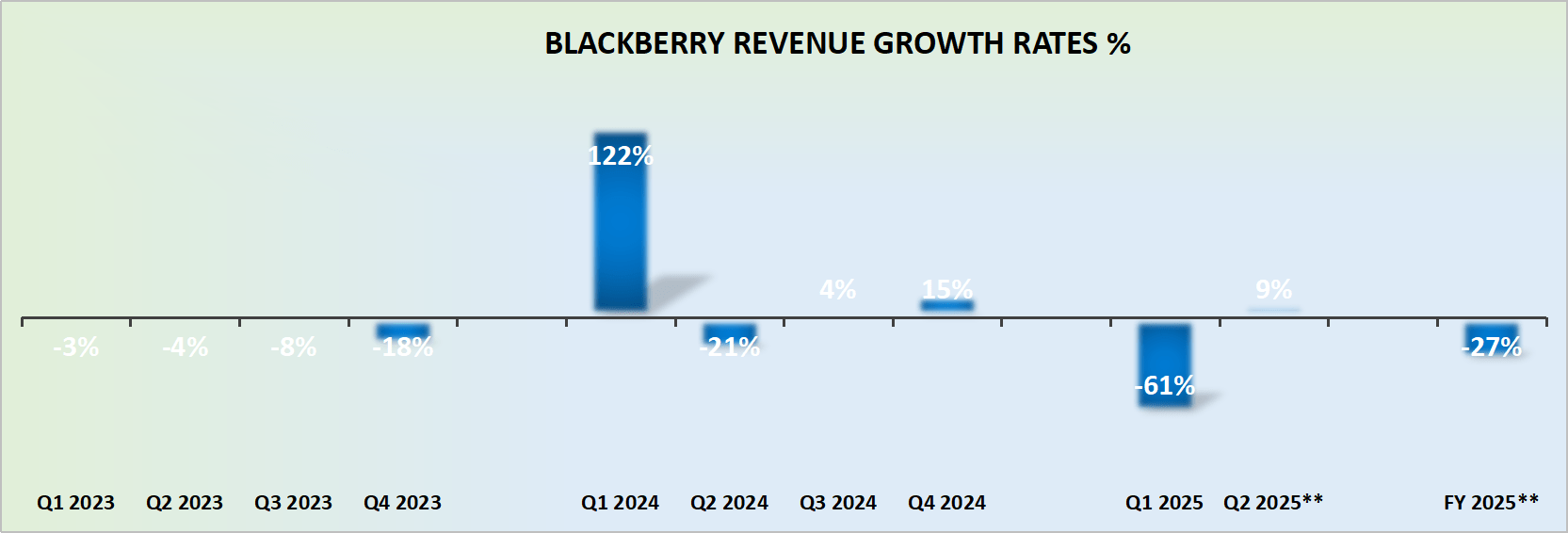

Revenue Growth Rates Are Starting to Moderate

BB (Revenue Growth Rates)

Before we go further, keep in mind that the negative 61% y/y shown in the graphic above for fiscal Q1 2025 compares against the same period a year ago, which included the one-off patent sales.

The actual organic growth rates were down 7% y/y. This means that it's possible that in the back half of fiscal 2025, as the overall comparisons start to moderate for BlackBerry, the business may start to exude better financials.

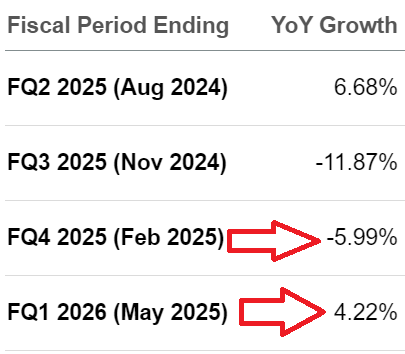

SA Premium (Revenue Growth Rates)

In fact, looking ahead to early next year, it appears possible that BlackBerry will start to report positive revenue growth rates, and that could significantly change investors' mood toward this business.

With that context in mind, let's now discuss its valuation.

BB Stock Valuation - +80x EBITDA

As an Inflection investor, I'm always thinking about the company's financial footing. I believe that companies that have no debt and ample cash have more than a safety net. They have the ability to make their balance sheet an asset that can be deployed to make a large needle-moving acquisition that propels the business forward.

More specifically, BlackBerry's market cap is made up of 16% as net cash. This is enough cash that can allow good things to happen.

And now, the aspect of most contention. I believe that paying +80x for BlackBerry's potentially $10 million to $20 million of forward EBITDA is excessive.

But there again, we have to think about the investor that will look at BlackBerry in the coming year. The investor that is in the stock today makes no difference. That's completely irrelevant. What matters is what the investors looking at BlackBerry next year will think.

And I'm not convinced that there's enough bad news left to take this stock lower.

The Bottom Line

While BlackBerry's prospects remain murky, the downside risk appears muted at this point. The company has repositioned itself toward IoT and cybersecurity, with 15% of its market cap in cash and no debt, providing it a solid financial cushion.

Although BlackBerry will struggle to compete with rapidly growing competitors like Samsara, which is annualizing over $1 billion in revenue and expanding at a 30% CAGR, it doesn't make sense to remain bearish on BlackBerry.

The stock seems fairly priced now, and as revenue growth stabilizes, there's potential for investor sentiment to improve, making it more of a neutral setup rather than a bearish one. Samsara offers a better growth story, but BlackBerry's downside is likely limited.

Strong Investment Potential

My Marketplace highlights a portfolio of undervalued investment opportunities - stocks with rapid growth potential, driven by top quality management, while these stocks are cheaply valued.

I follow countless companies and select for you the most attractive investments. I do all the work of picking the most attractive stocks.

Investing Made EASY

As an experienced professional, I highlight the best stocks to grow your savings: stocks that deliver strong gains.

- Deep Value Returns' Marketplace continues to rapidly grow.

- Check out members' reviews.

- High-quality, actionable insightful stock picks.

- The place where value is everything.