H-Gall

A stunning reversal bounce

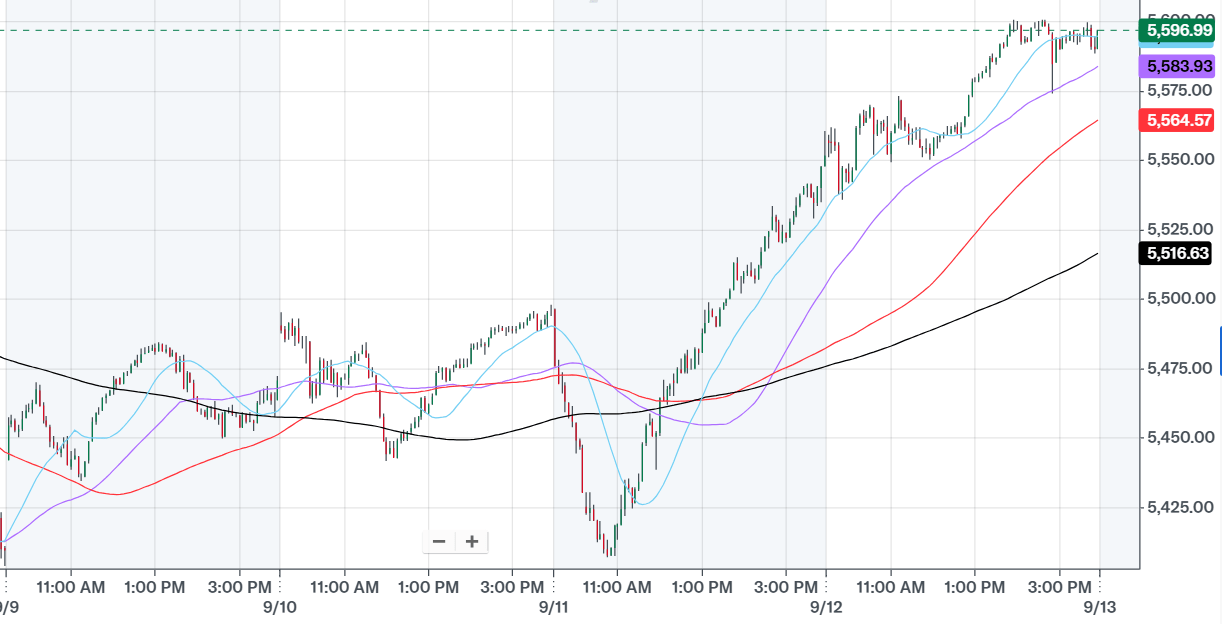

The S&P 500 (SP500) had a stunning bounce after the selloff caused by the August CPI release on Wednesday - the nearly 2% selloff turned into a 1% gain on Wednesday, which was extended by another 0.75% rise on Thursday. Here is the 3-day chart:

Yahoo

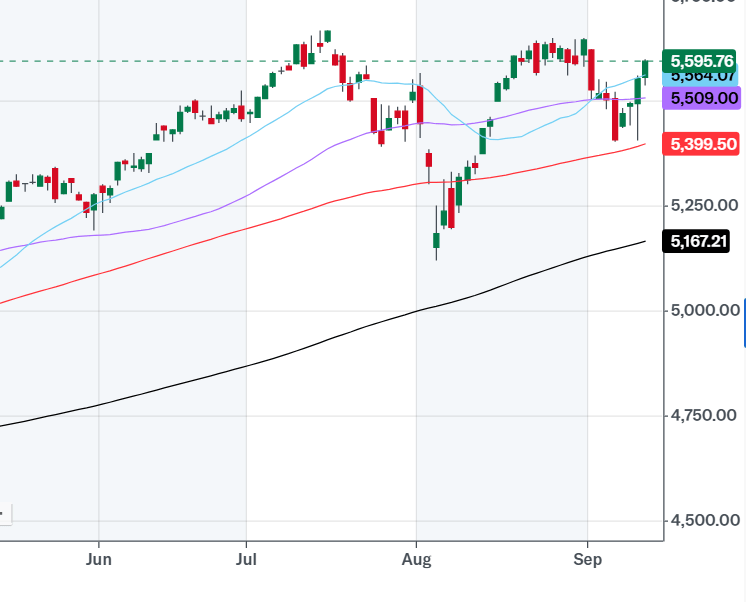

In fact, this bounce is similar to the August bounce. In early August, the S&P 500 sold off after the July labor market report, and also due to the Yen carry trade blowup, only to stage a sharp bounce higher towards the end of the month to near all-time highs.

Similarly, the S&P 500 sold off in early September after the August labor market data was released, and is currently bouncing back to the near all-time highs. Thus, it seems like the triple-top formation is developing, which would be a bearish technical indicator.

More importantly, the stunning reversal on Wednesday took the S&P 500 from near the key support level of 100dma to the 50dme resistance, which was broken, and further to the 20dma resistance, which was also broken on Thursday.

Yahoo

But, this is not a technical analysis article, so let's evaluate the fundamentals, and what's moving the S&P 500.

The bearish case

I am following these key fundamental variables, that collectively paint a very bearish picture for the S&P 500.

The pre-recession environment

As previously stated, the August and the September selloffs were in response to the respective labor market reports. Basically, the job creation is slowing significantly, based on the non-farm payrolls (including the negative revisions) and this trend is likely to continue and lead straight into the recession.

However, the mass layoffs usually associated with a recession have not started yet, and this is based on the initial claims for unemployment data. Although there has been a trend of rising claims since May, the claims have been falling over the last 6 weeks - this means we are not currently in a recession. The recent claims data from Thursday at 230K supports the thesis that the mass layoffs have not started yet. Thus, we are still in a pre-recessionary environment.

However, the bond market is pricing an imminent recession - the 2Y T-Bill Note (and Federal funds Futures) suggests that the Fed will cut from 5.33% to 2.82% by the end of 2025. The Fed cuts this aggressively only in response to a recession - this is not a normalization policy.

Thus, the recession is expected to come, and with it the recessionary bear market, as the earnings estimates for 2025 will have to be downgraded and the PE multiple will likely contract from 24 to sub-20.

Trading Economics

The Gen AI bubble burst

The Gen AI is likely a bubble because the wider adoption of the Gen AI applications is not happening, and the Gen AI capex does not have a sufficiently high rate of return. This is now well understood by the market, and even BlackRock is potentially turning bearish on Gen AI tech stocks, based on these recent statements:

We still favor the AI theme yet fine-tune our exposure. In the first phase of AI now underway, investors are questioning the magnitude of AI capital spending by major tech companies and whether AI adoption can pick up. While we eye signposts to change our view, we think patience is needed as the AI buildout still has far to go. Yet we believe the sentiment shift against these companies could weigh on valuations.

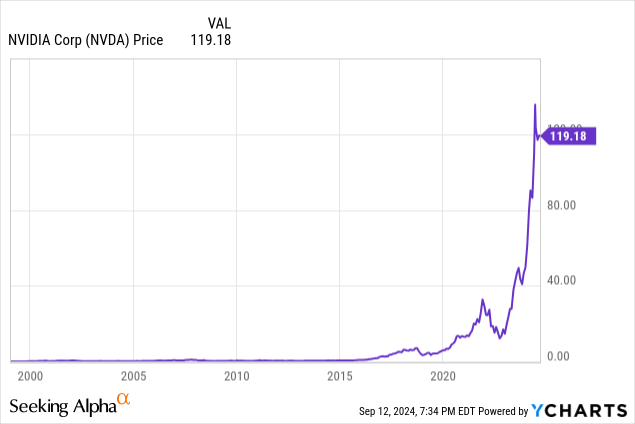

The valuations are still very high for the mega-cap tech stocks under the Gen AI theme, while the revenue growth rates are decreasing. Thus, the Gen AI bubble burst is unfolding. The mega-cap tech stocks led the market lower in early August, and also in early September. In fact, it was Nvidia (NVDA) that led the selloff in both cases, given the weak guidance in the latest earnings report.

However, it was also Nvidia that led the bounce in August, as well as the current bounce. Note, this is an early-stage bubble burst, and there is uncertainty as many retail investors are still bullish on Nvidia and buying the dips. The bubble bust will enter the accelerated stage only when Nvidia (and others) miss the earnings estimates, and for this, we have to wait for the next earnings season. This is the current state of the NVDA bubble burst.

Other risk factors

- The escalating geopolitical situation

The market is not currently pricing the escalating geopolitical situation, but the current situation is very dangerous, and it could produce a shock to the markets.

The situation in Russia-Ukraine has escalated to the point where the NATO countries are deciding whether to allow Ukraine to strike Russia with long-range missiles. This would potentially create a direct conflict between NATO and Russia.

The situation in the Middle East is also escalating, as the cease-fire agreement between Israel and Hamas is unlikely to be reached, and the strike by Iran on Israel is still a possibility. In addition, it seems like Iran is supplying missiles to Russia, so the conflicts in the Middle East and Ukraine are connected.

- The Yen carry trade blowup

The Yen has been rising against the US dollar, but the market is not being negatively affected by the rising Yen, as in early August. Yet, the situation requires monitoring, especially due to the expected Fed cut next week, which could weaken the USD.

Implications

The S&P 500 is facing a recessionary bear market with the Gen AI bubble burst. However, at this point, the recession is still delayed, and the Gen AI bubble burst is still in the early stages.

Thus, the S&P 500 remains resilient, as each selloff is met with dip buyers. Currently, we have another bounce led by Nvidia that's pushing the S&P 500 toward the all-time high level.

However, the current triple-top formation is likely to hold as more data comes and supports the bearish thesis.

The next trigger is the Fed meeting on Wednesday. For the current bounce to continue to the new all-time highs, the Fed needs to cut by 50bpt, which seems very unlikely given the higher-than-expected core CPI data for August. Thus, the Fed's meeting next week could be the trigger to the downside.