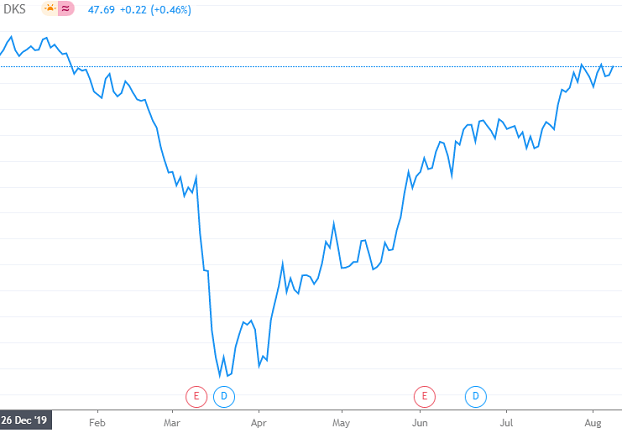

- Following the strong earnings report out of Foot Locker, Susquehanna sees Dick's Sporting Goods (NYSE:DKS) also sending some shockwaves through the retail sector when it reports on August 26.

- "We anticipate 2Q20 results will be much stronger than Street expectations particularly due to increased demand for high-ticket (albeit low-margin) hardlines product (e.g., bikes, exercise/golf/fishing equipment), which checks indicate continue to sell out. We expect the exercise-at-home trend will continue to accelerate in a post-Covid world. And while the exercise-at-home trend will likely be tailwind for DKS over the long-term, we expect sales of exercise equipment and other hardlines product to be amplified on the 2Q20 print," writes analyst Sam Poser.

- Looking ahead, Poser says DKS is positioned to benefit from competitor bankruptcies/store closures, a primarily off-mall store fleet where traffic has been faster to return to pre-crisis levels vs. mall-based retailers and a more developed e-commerce business.

- Susquehanna has a Positive rating on Dick's and price target of $59 (12X the FY21 EPS estimate).