- A big rally in nominal and real Treasury yields will leave U.S. equities in an unfavorable position compared with other regions, Citi says.

- Calling the recent rally in government bonds "largely technical," Robert Buckland, chief global equity strategist at Citi, is forecasting the 10-year Treasury yield (NYSEARCA:TBT) (NASDAQ:TLT) to rise to 2% through 2022, with real yields rising 70 basis points.

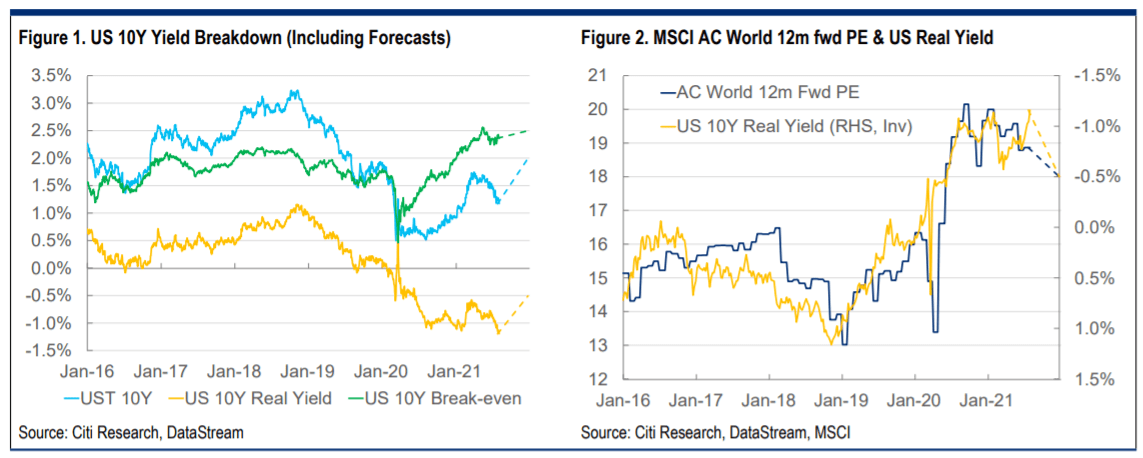

- The 10-year is currently up 2 basis points to 1.2%, while the 10-year TIPS (NYSEARCA:TIP) is just above a record low, down 2 basis points to -1.21%.

- "What is the bond market trying to tell us?" Buckland writes in a note. "Is it worried that the Delta Covid variant may hold back global economic recovery? Is it now convinced that the current inflationary upturn is transitory? Or does curve flattening (short yields up, long yields down) suggest potentially over-zealous monetary tightening, that a 'policy mistake' is now imminent? Maybe the bond markets are worried about a China slowdown?"

- "Citi US rates strategists are not especially convinced by these tempting narratives," he says. "Instead, they attribute much of the move to technical factors. Most notably, US treasury issuance has dropped over the summer, but will rise again later in the year. They think that this, along with ongoing economic recovery and likely QE tapering, will push 10-year bond yields back towards 2.0%."

- "We factor this bearish bond view into our global equity strategy," he adds. "Amongst regions, we downgrade the Tech-heavy US to Neutral. We upgrade Japan to Overweight, where valuations and cyclical exposure should be supportive, along with a weaker yen. We remain Overweight UK equities, our favourite value trade."

- "Amongst global sectors, we downgrade real yield-sensitive IT to Neutral and raise Health Care to Overweight. We remain Overweight Financials and Materials, which should outperform as bond yields rise."

- Citi strategist Tobias Levkovich, who has a target of 4,000 for the S&P 500 (SP500) (NYSEARCA:SPY) for 2021, says central banks have been keeping rates repressed since 2008, which indcates that they do not have confindence in sustainable growth and keeps risk premiums high.

- In 2008, the U.S. equity market was 30% deep cyclicals and 30% secular growth, he said on Bloomberg. But now it is 55% to 15% in favor of growth.

- "If you think bond yields are going to go higher, then growth stocks are probably going to take it on the chin."

- A big nonfarm payrolls number could jolt yields higher, but today's ADP showed a much-smaller-than-expected rise.