- The 2013 taper, 2017 Fed balance sheet reduction and even unexpected rate hikes indicate that equities won't be hit hard when FOMC starts trimming its bond purchases, Barclays says.

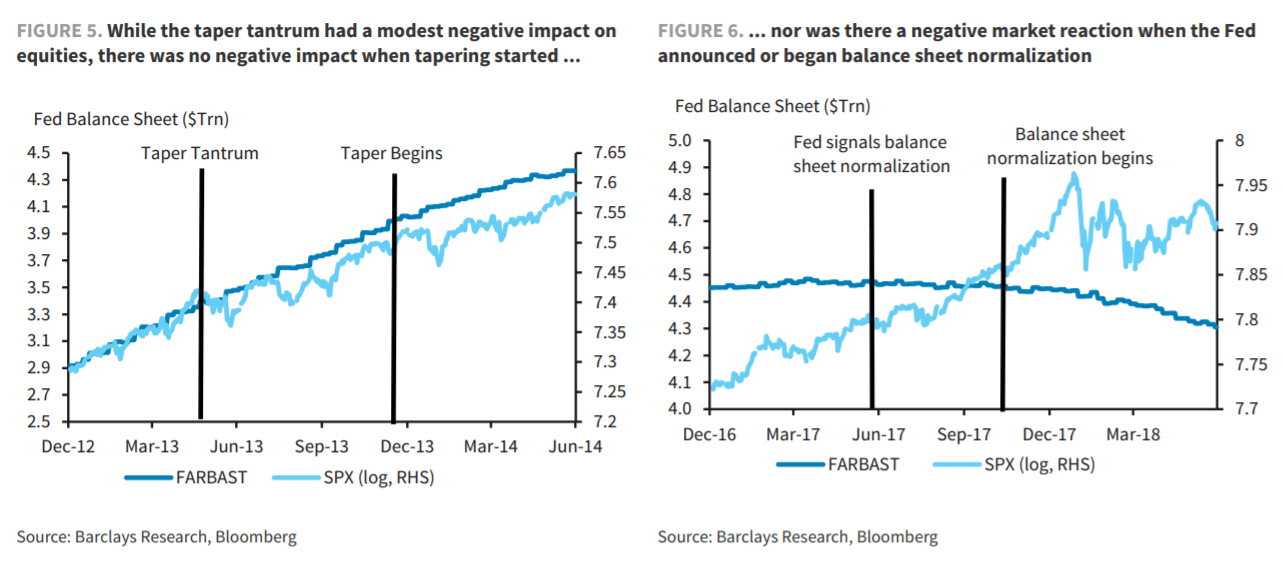

- "The direct relevant precedent is the 2013 taper of QE3 and this has drawn a fair amount of comparison," Barclays strategists led by Maneesh S. Deshpande write in a note today. "However, the chronology of events is quite important to gauge the potential reaction over the coming weeks. In particular, in our opinion, the relevant time frame is not the 'Taper Tantrum' in May 2013 but the actual start of the taper in December 2013."

- "Chairman Bernanke first raised the possibility of a taper during his Congressional testimony on May 22, 2013, which immediately caused a 'tantrum' in rates and they spiked by ~100 bp from May to June and continued to increase for the rest of the year," Deshpande says. "On the other hand, the impact on equities was relatively modest and transitory: they declined by 5.8% (from 5/21/13 -6/24/13) but the move reversed by July."

- The Fed has done a better job communicating about tapering this time around, he adds, with rates (NYSEARCA:TBT) (NASDAQ:TLT) actually falling and the S&P (NYSEARCA:SPY), Nasdaq (NASDAQ:QQQ) and Dow (NYSEARCA:DIA) moving into record territory.

- The Fed's balance sheet normalization "was announced in June 2017 and officially started in October 2017. Arguably this was a stronger step since it actually led to a decline in liquidity (rather pause in the pace of liquidity injection with the start of the taper) and yet there was hardly any equity market reaction," Deshpande says.

- And "even unexpected moves in the Fed Fund rate lead to only a modest move in equities," he says. "Our model forecasts that equities only drop 80 bp if the Fed unexpectedly hikes by 25 bp."

- "However, the reaction is dependent on prior equity returns. Thus, while equities on average drop ~80 bp, if equities have been range bound leading into FOMC meeting surprise hike, they are expected to fall only ~60bp. However, if equities have risen by 5% in the prior month, then a surprise 25bp hike would result in SPX -1.4%."

- SA contributor ZMK Capital says the Fed's tapering timeline may continue to boost Big Tech.