The Top Seven Oilfield Services Companies

When oil and gas companies are in the news, as they frequently are these days, there is seldom mention of the companies that enable all of that exploration, drilling, extraction, production and distribution. The backbone of the oil and gas industry is undoubtedly the Oilfield Services (OFS) companies, who not only keep the industry humming, but are growing in capacity and importance. The oil and gas industry is very volatile, as we outlined in Part 1 of our series and is impacted by five global trends, as we outlined in Part 2. Now in Part 3 of our series, we will focus on the OFS companies whose technology, innovation, efficiency, and tenacity are causing a fundamental shift in the oil and gas industry.

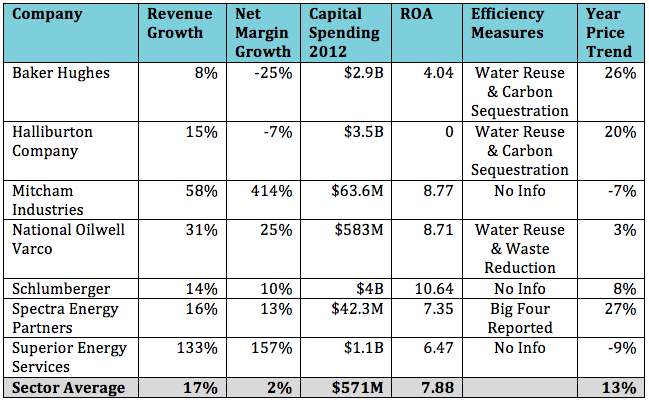

Several of these companies are well known and quite large, while others are tiny, but growing in size and influence. We analyzed a field of 36 companies using FiRM Analysis ((Financial, Resource, and Market)) that support the oil and gas companies in all facets of the exploration and production (E&P) cycle. Of the companies that made our top 7 list, the largest is Schlumberger (SLB), which earned over $42B in revenue in 2012, and the smallest is Mitcham Industries (MIND), which earned $113M in 2012.

Outlook for the Oilfield Services Sector

The oil and gas industry, particularly the largest companies, have been experiencing more than their normal share of ups and downs. The latest round of Q4 earnings calls revealed less than stellar performance by four of the largest companies whose losses reaffirmed our stance that positions in oil and gas companies should be closely monitored, as they are likely to experience yet more volatility over the coming year. Adding to the woes of the oil and gas majors, many smaller, leaner oil and gas companies are whittling