Why GPRO is Interesting As A Stock

GoPro (NASDAQ:GPRO) has been one the most active stocks on the market since its IPO in 2014. In October of 2014, the stock registered a 52-week high of $98.47, marking more than a 190% run up since its IPO earlier that year.

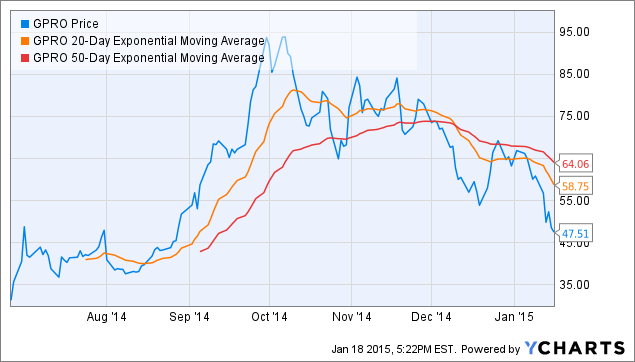

GPRO data by YCharts

Since then shares have tumbled 48% on news of a camera-related Apple patent and worries of a too premium valuation.

GPRO data by YCharts

Yet, despite the huge sell-off, the percent of shares short is still increasing, and is at an all-time high of 11.76%.

GPRO data by YCharts

A technical analysis viewpoint, however, shows that the last time the stock traded significantly below its EMAs (mid-December), the stock rebounded to prices right in line with its EMAs, roughly a 20-25% surge in stock price.

GPRO data by YCharts

We believe all these charts signal why GPRO is such an interesting company to follow for 2015, and one that offers investors a lot of promise.

Qualitative Understanding

GoPro has been headlining news these past two weeks with concerns regarding potential competition and longevity of the product offered.

The new GoPro HERO4 camera has steered GoPro down a new path with incredible high-resolution footage, touch display and wireless and Bluetooth capabilities. GoPro also is currently positioned to expand into newer markets, potentially constituting them as more than just a camera company.

A recent partnership with UK-based Vislink signals opportunity for GoPro international sales to increase, perhaps even regaining international revenues they lost in 2014. Per the chart below, we can see that while Americas revenue have more than doubled so far in 2014, international revenues have taken hit, especially a 21.5% decrease in Europe/Middle-East/Africa sales in the quarter ended September 30, 2014.

| Three months ended | Nine months ended | ||||||||||||||

| (in thousands) | September 30, 2014 | September 30, 2013 | September 30, 2014 | September 30, 2013 | |||||||||||

| Americas | $ | 204,893 | $ | 92,515 | $ | 482,769 | $ | 328,006 | |||||||

| Europe, Middle East and Africa | 50,905 | 72,176 | 193,844 | 218,884 | |||||||||||

| Asia and Pacific area countries | 24,173 | 27,455 | 83,679 | 77,395 | |||||||||||

| $ | 279,971 | $ | 192,146 | $ | 760,292 | $ | 624,285 | ||||||||

GoPro and Vislink are looking to create a minute transmitter that can be worn or mounted in distinctive areas for enabling a unique broadcast experience for viewers. If successful, this would mean a whole new market of wearable broadcasting devices for sports.

As mentioned earlier, worries over wearable camera patent technology from Apple (AAPL) has caused GoPro stock to recently plummet.

One firm, however, believes that this was an overreaction, and that the Apple patent does not directly compete with GoPro or threaten GoPro's products.

After analyzing US Patent 8934045 (and although we are no camera technology patent experts, we have analyzed a few patents in-depth before), we believe this statement to be true. The patent's technicals (2-Axis imaging, remote control use case, etc.) are more applicable to smartphones and other smart devices as opposed to action capture devices like GoPro's HERO.

Further, we believe GoPro and HERO have no parallel in the business. While one competing product has incorporated LTE technology, that competing product does have the user wearability, flexibility or specifications that HERO provides. Indeed, we believe that as this section of the camera sector is currently booming, GoPro could utilize this incorporated LTE technology to bolster its own products and revenues.

Despite these potential catalysts and the stock's upside potential, we are not overly bullish on GoPro. Analysts have pegged growth rates in the next five years at roughly 33% per annum, which seems absurdly high for a company with large uncertainty in its future. While we do believe that GoPro has established themselves as the pioneers in wearable recording devices for sports, we see many barriers in entering new markets.

GoPro is set to release earnings on February 5. As such, we believe now is an appropriate time to value the stock.

Valuation

To value this stock, we have employed a two-stage FCFE (Free Cash Flow to Equity) Model with the two stages being: 1) a high-growth stage, and 2) a stable growth-stage.

Given the uncertainty surrounding the upside of this stock, but acknowledging that there is revenue and earnings growth to be had in the foreseeable future, we have employed a weighted average analysis to achieve a fair present value for the stock.

To do this, we have created 35 different scenarios in our FCFE model by combining varying high-growth rates from 35% to 5% in 5% intervals (7 different rates) with varying stable-growth rates from 6% to 2% in 1% intervals (5 different rates).

We have chosen 35% as the ceiling high-growth rate in the next five years (annually) because this is slightly higher than already optimistic analyst projections (33.28% per annum) while still significantly below GPRO's most recent quarter growth of 45%, which GPRO said it could not sustain in its most recent conference call.

Further, we have chosen 5% as the floor high-growth rate in the next five years (annually) because, per qualitative upside outlined above, we believe GPRO is king of a growing industry, which should constitute some marginal earnings growth going forward.

We believe that within 3-5 years, the camera market will be saturated, and that GPRO's high-growth era will come to close. We further believe that GPRO's HERO products is one-of-a-kind and will continue to be the premium product in that industry for years to come, despite increasing competition (much like the iPad). As such, we believe a stable growth rate of at least 2% is appropriate for GPRO, and that growth rate could be as high as 6% (we cannot reasonably see a company growing more than 6% per annum long-term into infinity).

In our weighted averages analysis, these 35 unique scenarios give us 35 unique "price-targets." We then separate our 35 PTs based on common stable growth rates. Consider our 6% stable-growth rate chart for varying high-growth rates below.

| 6% Stable Growth Rate | |

| High-Growth Rate | PT |

| 35% | $115.74 |

| 30% | $95.82 |

| 25% | $78.69 |

| 20% | $64.06 |

| 15% | $51.64 |

| 10% | $41.17 |

| 5% | $32.39 |

We then assume standard Gaussian distribution of probabilities with mean of 20%. In other words, we attribute that a 35% high-growth rate has just as much likelihood of occurring as a 5% high-growth rate, a 30% high-growth rate has just as much likelihood of occurring as 10% high-growth, etc. The other assumption is that a 25% high-growth rate is more likely than a 30% high-growth rate, which is more likely than a 35% high-growth rate.

"With mean of 20%" simply implies that we believe 20% is the most likely high-growth rate in the next five years.

We can thus assign "weights" to our PTs using this quasi-Gaussian distribution, and appropriately take a weighted average of our PTs. Again, see our 6% stable growth rate chart for this below.

| 6% Stable Growth Rate | ||

| Weight | PT | Weighted PT |

| 1 | $115.74 | $115.74 |

| 2 | $95.82 | $191.64 |

| 3 | $78.69 | $236.07 |

| 4 | $64.06 | $256.24 |

| 3 | $51.64 | $154.92 |

| 2 | $41.17 | $82.34 |

| 1 | $32.39 | $32.39 |

| Weighted Average: | $66.83 | |

After performing this analysis for 5%, 4%, 3% and 2% stable growth rates, we employ a similar analysis on the weighted averages for constant stable-growth rates. This gives us the chart below.

| Stable-Growth Rate | Weight | Weighted Average PT | Double Weighted PT |

| 6% | 1 | $66.83 | $66.83 |

| 5% | 2 | $51.53 | $103.06 |

| 4% | 3 | $42.17 | $126.52 |

| 3% | 2 | $35.87 | $71.74 |

| 2% | 1 | $31.33 | $31.33 |

| Weighted Average: | $44.39 | ||

We can then arrive at what we feel is a fair present value of GPRO, roughly $44 per share, based on our weighted average analysis.

Given uncertainty surrounding the camera market and GPRO in general, we attribute roughly 15% uncertainty to this valuation, meaning we believe the stock's present value could vary anywhere between 85% to 115% of our aforementioned weighted average present value.

Thus, we believe GPRO has a present value range of $37-$51 a share.

Naturally, this implies we would long the stock at any prices under $37 and short it at any prices over $51.

Justification for the Model

Given financial models are rather parameter sensitive (especially in relation to growth rates), we believe this weighted analysis approach is the fairest way to valuing the stock.

We also believe that 20% growth rate in the next five years per annum with a stable growth rate thereafter of 4% is the most likely scenario, as our model weights. We believe this because it is a fair compromise between an "all-goes-right" 35% high-growth rate scenario wherein HERO remains top dog, international sales pick back up, and GoPro expands into more than just an action camera company, and an "hardly-anything-goes-right" 5% high-growth rate scenario wherein HERO sales climb but all else is rather unsuccessful.

Conclusion

We don't pretend to know exactly what the growth rate will be in the next five years, but we do have a general feel that 20% looks most appropriate. This is why we have employed a weighted average approach to valuing this stock, and have also accounted for relative uncertainty.

The stock may very well bounce or fall based on what the company reports on February 5. Either way, if the stock falls out of our present value range, we will enter a position in the stock accordingly.