Elevator Pitch

With Seven & i Holdings Co., Ltd.'s ADR (OTCPK:SVNDY) is trading at $22.79 and the Tokyo Stock Exchange's equivalent (OTCPK:SVNDF) is trading at $44.49. This is an opportune moment to buy a solid foreign investment. Seven & i's financials - i.e. sales, EPS, and distributions - will steadily grow in the coming fiscal years and virtually all analysts expect the company to outperform its estimates. As the already leviathanic company spreads its reach into Southeast Asia and its growing middle-class economies, the outlook for Seven & i is only positive.

Company Description

Seven & i Holdings Co. is a large-cap-blend general food and staples holdings company based in Japan, publicly traded on the TSE, with an ADR listed on the Nasdaq, available for U.S. investors. The company operates in seven business segments, however; its main operating focus areas are convenience stores, superstores, department stores, specialty stores, and restaurants. Seven & i has 118 consolidated subsidiaries with 24 equity-method affiliates and employs over 54,000 full-time individuals. Its subsidiaries are recognizable worldwide. For example, if you've ever lived in the U.S., you should recognize the 7-Eleven convenience store franchise; or, if you've ever lived in Japan, the Itō-Yōkado superstore should ring a bell.

Thesis And Catalyst For Seven & i Holdings Co., Ltd. ADR

In Japan alone, Seven-Eleven Japan Co., Ltd. has a total of 17,491 domestic stores (up 1,172 stores YOY) in 43 prefectures and opened a record-high 1,602 stores this fiscal year, including "...an expansion into Ehime Prefecture in March 2014 and the opening of stores in train stations through business alliances with the JR West group and the JR Shikoku group, etc." On top of the staggering amount of convenience stores that Seven & i already operates in Japan, Seven & i's presence is Southeast Asia growing rapidly, for example, at a rate of 500 stores per year in Thailand. Seven & i's explosive expansion into the rest of Southeast Asia is reminiscent of the spread of Imperial Japan (albeit economic not military) and is major catalyst for future growth.

The pie chart below shows the growing share of convenience stores Seven & i operates internationally.

(Source: Original image; data from Seven & i Shareholder's Meeting)

Valuation

(as of October 1)

SVNDF: $44.49

SVNDY: $22.79

52-week High: $23.87

Conservative Price Target: $27.45

Yield: 1.34% (5-yr avg. 2.07%)

(Source: SunGard)

CAPM: With the data collected, we can calculate the basic capital asset pricing model, or CAPM, in order to predict the theoretical expected return of SVNDY after one year. Using the yield of 0.025% of a three-month Japanese government bond as a proxy for the risk-free rate, the beta value of 0.66, and the expected market return based on the price target, the CAPM is as follows:

ra=rf+βa(rm-rf)=0.025%+0.66(16.98%-0.025%)=+11.22%

Please note CAPM is a general tool for describing the relationship between risk and expected return for securities. It is based on a number of assumptions about the behavior of investors and does not take into account the risks of foreign investment; as such, accuracy is variable.

Currently, SVNDY is roughly ~16.98% below its price target of $27.45, based on its current and forward P/E. Not to mention, this is a conservative estimate that does not take into account, for example, its potential higher earnings and growth incoming for 2016-17. With major institutions maintaining BUY ratings and projecting the company to outperform in the coming fiscal years, SVNDY is a solid choice and currently undervalued.

(Source: Original image; data from NASDAQ)

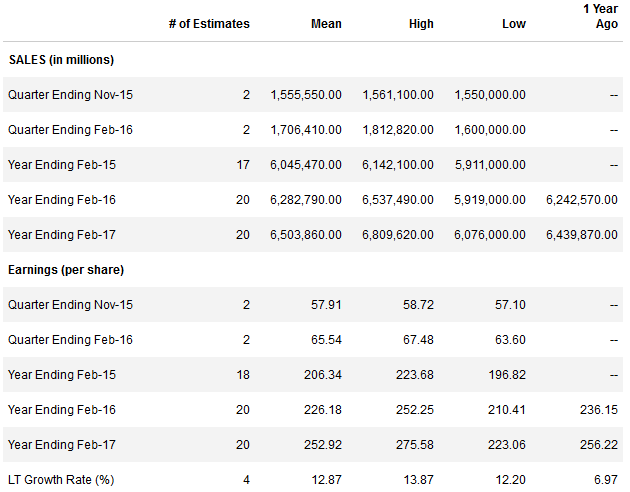

Revenue And EPS Outlook

During March 1, 2014, to February 28, 2015, revenues from operations in convenience store operations were ¥2,727.7 billion (up 7.8% YOY), and operating income was ¥276.7 billion (up 7.5% YOY). Like many Japanese stocks, SVNDY has a fairly average-to-high P/E ratio, at $27.62. Compared to general retail counterparts in the U.S., it correlates very well (average U.S. retail trailed P/E ratio at $27.65 and a forward P/E of $22.96). The company has also signaled to shareholders that it seeks to greatly increase future distributions, i.e. dividends, and this can be seen in analyst estimates for future EPS.

(Source: Thomson Reuters)

Competitive Landscape

To understand the competitive landscape of Seven & i Holdings Co., it is necessary to understand the nature of Japanese "collectivist state capitalism." From the days of the pre-Meiji shogunates to the post-WWII zaibatsu, the nation of Japan has a complex yet marked history of collusion, cartelization, and monopolism. In the modern day, this pseudo-capitalist system persists as keiretsu - long-term intimate business relationships and shareholdings between sets of companies. Robert L. Cutts writes of the keiretsu in the July-August 1992 issue of the Harvard Business Review:

"This lattice work of interwoven interests depends upon the acceptance of a national social contract by workers, corporations, and the government, as well as the compliance of the consumers who are penalized by it. And this idiosyncratically Japanese version of capitalism-unified more by tradition and custom than by formal legal ties such as interlocking directorates and cross-ownership-has proven to be at least as vigorous as its American or European counterparts. Indeed, Japan's strength causes many people to ask if keiretsu is the ideal socio-political-economic system, the new paradigm for industrial supremacy."

Seven & i is exemplar of the keiretsu system. Essentially...there is no competition - its various subsidiaries do have minor competitors, yet as a holdings company, Seven & i is unparalleled and unprecedented even in Japan. Investing in Seven & i is almost akin to investing in the entire Japanese retail sector as a whole. With the Japanese government still favorable towards this economic system and virtually no historical legal precedent against such monopolies, there is no threat to Seven & i's hegemony over the retail sector.

Variant View And Currency Consideration

Investing in any foreign company presents additional risks such as conversion expenses and foreign taxes. It is also important to consider the impact of currency value on any investment. A weaker yen and a stronger dollar is a mixed bag for Seven & i; while it could mean less costs and more profits for international exports, i.e. into the U.S. and SE Asia, it could also mean higher prices for imports, especially food costs. With the yen forecast to stay in depreciation and the BoJ signaling no changes in monetary policy, this trend is on track to continue. More and more analysts, however, see the BoJ as having to provide more QE in the near future, such as Goldman Sachs which states:

"...we think weaker growth is raising the odds of additional BoJ and ECB stimulus at coming meetings...Both central banks will need to provide additional stimulus in fairly short order to meet their inflation forecasts...We therefore maintain our strong view for EUR/$ downside and $/JPY upside in coming months."

So, it can be forecasted that if the BoJ moves to provide more monetary stimulus, then the USD/JPY will lower to more normalized levels wherein, subsequently, the currency impact on Seven & i's business would be minimal.

(Source: XE)

Additionally, compared to some of the competitors of its subsidiaries, Seven & i may not seem like the best investment in certain technical datapoints. For example, in the convenience store sector, FamilyMart Co., Ltd. (FYRTY) is a worthy competitor with a much less expensive P/E of ~19 and a higher yield of 2.10%. Furthermore, there are a few indicators that may not signal SVNDY to be such a strong buy, such as the fact that SVNDY's current P/E is higher than its 5-year average or that its price target is not 20% above its current price. However, despite these current weaknesses, SVNDY is still a strong investment for the future and a risk worth taking.

Conclusion

Despite Japan's incoming demographic decline or historically weak consumption or contracting economy, the Japanese economy is still one of the strongest in the world. One particular positive factor for investors to take note of is that under the Abe administration, Japan's corporate tax rate is lowering, with plans to get the rate under 30% over the next five years, which will have a direct positive effect on Seven & i's future income. Overall, with its fundamentals and financials looking strong and its unparalleled dominance in the Japanese retail sector, Seven & i is one of the strongest foreign investments in Japan.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.