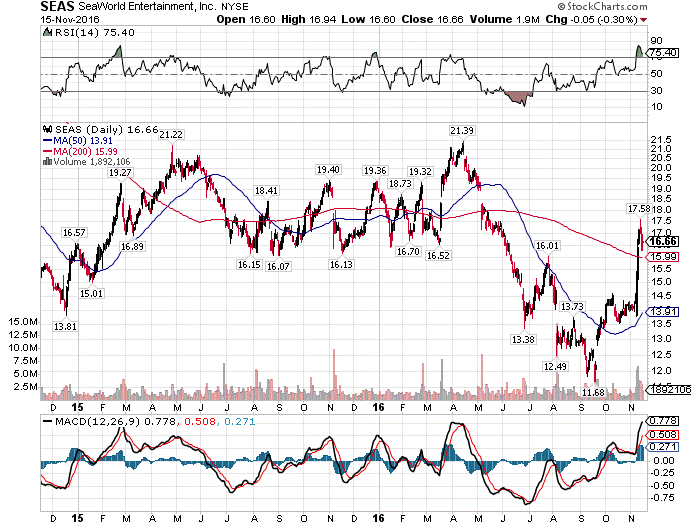

SeaWorld (SEAS) has been a battleground stock for the last two years or so to put it lightly. The company's fundamentals were starting to show some signs of wear before the Blackfish documentary put SEAS on the mat and since then, it has only gotten worse. The stock has struggled since then and SEAS has also suspended its once-huge dividend. But at $16, one wonders if the damage done to the stock combined with the improvements we are starting to see in the fundamentals creates a situation where SEAS may actually be worth a look on the long side. Shares exploded higher off of the Q3 earnings report and have consolidated those gains; is this the start of a rally?

SEAS saw yet another quarter of negative revenue growth, something that has plagued the company for years at this point. SEAS continues to struggle with the combination of traffic and in-park spending and at times, both have seen strength. The problem is that we haven't seen a robust combination of the two and that has hurt SEAS' ability to keep revenue afloat. In Q3, traffic was actually up 1.3% despite a headwind from Latin America, but per capita spending was down 2%. This reflects a small decrease in in-park spending and a more sizable decrease in ticket revenue per guest. This is the opposite situation SEAS produced in recent quarters where traffic was down but was offset partially by higher spending; the numbers have flipped but the results are largely the same; SEAS has a revenue problem.

To be fair, we know SEAS has a revenue problem and we also know it is probably going to have that same problem for at least a few more quarters to come. Management's commentary surrounding traffic was positive in the Q3 release but no specifics were given. If the Latin America headwind really is abating, perhaps we'll see traffic and per capita spending move up together but right now, that isn't in the cards.

But what about the rest of the business? SEAS is making progress with its new attractions and of course, the orca controversy seems to have died down. We don't really know yet what the new version of SEAS will look like once its orca shows have gone and it has remade its ride and show lineup. The progress that has been made is encouraging but it is also early. But for now, things like Cobra's Curse and Mako seem to be drawing in guests and that's great news.

Higher marketing and labor costs contributed to operating expenses rising despite the fact that revenue was down once again. This is a problem that SEAS has continuously experienced and it drove adjusted EBITDA down 10% against last year's Q3. That means margins suffered quite substantially but to its credit, SEAS is working on it. Management announced a cost savings program with an ultimate goal of $65M per year and $40M by the end of 2018. That's an ambitious goal if we put it into the context of adjusted EBITDA, which is supposed to be around $320M this year. If most or all of the savings from the expense cuts flow through to adjusted EBITDA - and they should - that would represent a 15% or 20% increase irrespective of any other gains that may accrue between now and then. We are a long way off from those cuts coming into effect but there is certainly a lot of potential here.

The thing is that despite the rosy commentary surrounding the Q3 report, SEAS certainly isn't out of the woods. S&P continues to be negative on SEAS' debt and why not? There is a lot of it and SEAS continues to produce lower operating earnings. Until that turns around via lower debt totals or higher earnings - preferably both - debt is going to be a problem. SEAS suspended its dividend so it can use some of that cash to pay down debt but we also know investments are being made to drive traffic. Management wasn't specific on what it plans to do with the dividend cash but I hope for SEAS' sake that some sort of debt reduction is in the cards.

At 22 times next year's earnings, SEAS is very much still valued like a turnaround stock. There is no fundamental reason why this stock should trade for that valuation given all of the headwinds it faces but to its credit, steps are being taken to improve its operating results. Suspending the dividend is painful for shareholders that held the stock for income but it was the right thing to do to get the house in order. The money that would have paid the dividend can continue to fund new rides and shows as well as pay down some of the massive pile of debt on the company's balance sheet, all of which should provide SEAS with a brighter future. But does that make the stock a buy?

SEAS is very expensive right now as investors bet on a successful turnaround. While I'm on board with this conceptually - the early read seems to indicate actions taken are working - I'm not sure this stock is ready for 22 times forward earnings. After all, if adjusted EBITDA does rise by 20% or so in the next two years and EPS rises by the same amount, we are still talking about a dollar or less of EPS in 2018. That would put SEAS at almost 17 times 2018 estimates and I'm not sure SEAS has earned that right. As a former bull I want to own SEAS again but I keep finding reasons not to.

The fundamentals seem to be improving but for me, I haven't seen enough to warrant the gigantic rally we've seen since the earnings report. I think SEAS has accrued several quarters' worth of gains in a few days and that means I'm on the sidelines. Things are getting better for SEAS but I just don't see enough progress to pay 22 times next year's earnings for this stock. If it comes in I may be interested but longs would do well to consider taking some off the table after the rally.