Workiva is the unquestionable leader when it comes to providing XBRL services to public companies. With their solution Wdesk, the company has seen revenue grow over the past year. In Q2 2017 revenue increased roughly 15% ($49.4 million), in part thanks to Q2 subscription and support revenue growing 17.2% ($41 million) compared to prior year.

The company also has an impressive revenue retention rate which was 96.1% (excluding add-on revenue), and the revenue retention rate including add-on revenue was 106.0%. Add-on revenue includes the change in both seats purchased and seat pricing for existing customers.

Workiva has the largest number of clients of any XBRL service provider. In the first quarter of 2017, Wdesk was responsible for over 50% of filings relating to XBRL facts. Workiva finished the second quarter with over 2,908 customers, including new client, Walmart (WMT). Workiva saw an increase of 286 clients from Q2 2016.

Workiva specializes in compliance services but as management mentioned on the Q2 conference call, non-SEC sales are gaining traction as more clients are purchasing add-on services.

Workiva’s revenue growth is impressive, especially their subscription and support revenue. However, I have concerns regarding their XBRL professional services and the quality of their XBRL.

What is XBRL?

XBRL (eXensible Business Reporting Language) is the underlying code associated with financial statement filings. It was created to provide an approach for which financial data can be easily sorted and compared. For all public companies, XBRL must be “built” and “tagged.” Using elements from approved SEC taxonomies, a company will select elements or tags to include in their taxonomy. From this custom taxonomy, the elements will be “tagged” meaning the elements become associated with values within the financial statements and footnotes. For Workiva, these types of services would be classified as Professional Services, which only grew 4.6% compared to Q2 2016. Professional services make up less than 20% of the company’s total revenues for Q2 but these services could have a resounding impact for the company going forward.

Professional Services - Opportunities

As the management team mentioned during their latest conference call, Workiva doesn’t plan to get into the IPO market until 2018. Arguably the two largest IPO filings of 2017, Blue Apron (APRN) and Snap, Inc. (SNAP) went to competitors, Merrill Corporation (Blue Apron) and Donnelley Financial Services (Snap). The professional services revenue to set up XBRL can be considerable and likely these IPO dealings would result in an initial service agreement which would contribute to subscription and support revenue.

Workiva’s next opportunity lies with foreign filers. Foreign filers may file with XBRL immediately; however, they must file their financial statements with XBRL on or after December 15, 2017 (More information about this mandate can be found here - SEC.gov | IFRS Taxonomy). This new mandate gives service providers such as Workiva a new market for which they can provide XBRL professional services. Like the IPO market, the revenue that could be generated from creating the XBRL for these foreign filers could be considerable for the company. The management team has failed to mention this huge opportunity which makes me believe the company is not aggressively pursuing this opportunity or they hope to poach these foreign filers after the initial XBRL is completed.

Neglecting such an opportunity in the XBRL world leads me to my biggest concern which is the accuracy of Workiva’s XBRL.

Risks – XBRL Accuracy

In recent years, the SEC has begun to look at XBRL filings more seriously. The SEC as well as investors consuming XBRL information are looking more closely at this information and are notifying companies of XBRL errors. One of the biggest XBRL errors to date occurred at Goldman Sacks (GS). Goldman had to submit an amendment to their 10K filing due to issues with the XBRL. (Read here for further information on the incident - Yes, the SEC Examines Your XBRL Exhibits). This lack of due diligence by both the service provider and the public company can create additional costs as well as unwanted negative attention.

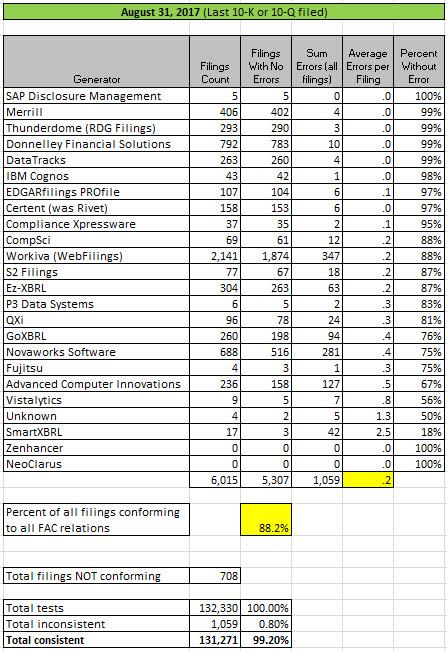

Over the past several years, individuals and organizations such as XBRL US have sought to improve XBRL quality. Charlie Hoffman, dubbed the father of XBRL, has been a vital part of creating fundamental accounting rules (FARs) for all XBRL filers. His rules (many of which are basic such as Assets = Liabilities + Stockholders' Equity) help ensure accuracy within XBRL filings and also contribute to making the data more comparable. Hoffman has reached out to service providers to share his rules in an attempt to improve XBRL accuracy. He has been reviewing XBRL accuracy for the last several years. As shown below for Q2 2017 filings, some service providers are bearing better results than Workiva as Hoffman himself states -

This is the data to which Hoffman is referencing for Q2 2017 filings:

In my opinion, Workiva's poor results are due to two reasons. The first is that they are letting their clients handle their own XBRL. Due to the complexity and ever-changing XBRL guidance, a self-tagging client will surely file with an error. If not now, then certainly in subsequent filings. The second and more concerning reason for Workiva, is that their XBRL knowledge when it comes to building and tagging falls short compared to their peers. With the continued scrutiny filers and public companies are under, should Workiva continue to struggle with the accuracy of their XBRL filings, an issue like the one with Goldman Sachs, could soon be on the horizon.

Issues with XBRL accuracy would directly impact the creditable of Workiva’s professional services. Since the company is first and foremast, a compliance services company, an XBRL problem such as this would certainly bleed over and impact the subscription and support revenue as well.

Valuation

Workiva's net margin is -18.9% for the last 12 months, compared to -6% for the industry average. Considering the poor P/E ratio and continued expected negative earnings per share (expected EPS average for 2018 being -0.45), there is likely no clear path to profitability for the next several years. With the 32% growth in share price for past year, I believe Workiva's stock is currently overvalued and wouldn't buy unless the price dips back down to the mid-teens.

Conclusion

Workiva has the best product on the market in Wdesk, which is reason the company is seeing impressive revenue growth within their subscription and support revenue. However, the quality of Workiva’s XBRL does not compare to their peers. Neglecting professional services opportunities to pursue non-compliance revenue puts Workiva at risk. Considering the company appears overvalued and might face issues due to XBRL accuracy I would not recommend Workiva. I have no current position in Workiva but will look to future posts by Charlie Hoffman in regards to XBRL quality and will monitor future calls to see if management mentions XBRL professional services.