Analysis Brief

Microsoft Corporation (NASDAQ:MSFT) provides an excellent growth opportunity given the company's dominant position in the technology software market and the company's diverse product line. Microsoft is one of those few Fortune 500 companies that has excelled in its industry since its inception, from Windows, Microsoft Office, and other programs to cloud technology and high-tech devices. Microsoft is a cash cow, with a strong balance sheet and tremendous cash flow. With growing revenues, growing dividends, and steady margins, Microsoft Corporation makes for a good growth position. Additionally, Microsoft is one of the leading companies in hybrid-cloud technology with Azure, which seamlessly allows old hardware-based data management systems and newer cloud-based data management systems to combine and support the mission and vision of various companies. In the future years, I expect Microsoft's relative market position to strengthen as Azure claims its rightful position in the marketplace. More details regarding Azure can be found under the Catalysts section of this report.

I valued Microsoft using the discounted cash flow model using free cash flow. Using my observations and assumptions, my model yielded an intrinsic value of $126.48 for Microsoft. (Additional details can be found in the "Valuation" section of this article.) Given my understanding of the company and the industry in which it operates, combined with my fundamental analysis of its financials and the general economy, I recommend this company as a strong buy.

Catalysts

Azure: Hybrid-Cloud Technology

What is Azure?

Azure is a hybrid-cloud based service offered by Microsoft Corp. that modernizes existing IT infrastructure by upgrading it to the cloud. A hybrid-cloud is a cloud computing model that connects a company's existing IT infrastructure with a cloud platform to allow for seamless interface between the two platforms. Hybrid-cloud technology is beneficial for companies that operate on an aged IT infrastructure that makes it difficult for them to switch to a cloud platform. With Azure, the size and age of existing infrastructure becomes irrelevant, which is not the case with many other cloud-based technologies in the market. No matter how small, large, old, or new a company's IT infrastructure is, through Azure, they can integrate it all into one seamless system. As advertised by Microsoft, Azure is increasingly productive, is hybrid, is intelligent, and is trusted. According to Bloomberg Intelligence, Microsoft has become a dominant player in the cloud industry with its cloud-based product offerings.

Services it offers?

Azure offers over 100 different services to its users. Some examples of services include AI + Machine Learning, Internet of Things, Management Tools, Analytics, Storage, Networking, Security, Integration, etc.

Additionally, Azure benefits a variety of small corporations, Fortune 500 companies, and government agencies. It offers solutions for the following industries: health and life sciences, retailers, government, manufacturing, and financial services. These solutions provide services that make processes and activities for these companies more efficient and effective.

Growth in Azure

- Azure is a part of Microsoft's Intelligent Cloud Segment

- In Quarter 3 of Fiscal Year 2018, Intelligent Cloud revenues increased to $7.9 billion or by 17% Y/Y.

- Revenue growth in the Intelligent Cloud has been led by growth in Azure for the past 15 quarters.

- Intelligent Cloud represents nearly 30% of Microsoft's consolidated revenues.

- In addition to Azure, Enterprise Services and other Server Products and Cloud Services are contributing to increased growth in Intelligent Cloud revenues.

- Enterprise Services grew by 8%.

- Server Products and Cloud Services grew by 20%.

- Azure's revenue grew by:

- 90% in Q1 of FY18.

- 98% in Q2 of FY18.

- 93% in Q3 of FY18.

- Azure has been experiencing double-digit and triple-digit growth for the last several quarters, and I expect this growth to continue.

- Additional investments are being made in Azure to improve the quality of the software.

Competition

There are a few competitors in the market that are comparable to Azure, but Azure might be more favorable for several customers because of the range of services that it offers and its ability to integrate the Windows Server and other enterprise products that are offered by its competitors or are used by customers. Additionally, since most businesses use Windows as their main operating system, it is easier and more cost-effective for them to elect Azure as their choice for a hybrid-cloud based technology.

Other Positive Factors with Microsoft

- In addition to Intelligent Cloud, Microsoft's other segments, Productivity and Business Processes and More Personal Computing, are experiencing double-digit revenue growth at 17% Y/Y and 14% Y/Y, respectively, in Q3 of FY18.

- Growth in Office 365 cloud technology.

- Microsoft is considered a cash cow, with over $39 billion in Cash from Operating Activities in FY 2017.

Outlook for Hybrid-Cloud Industry

- According to Bloomberg Intelligence, many large enterprises are upgrading their IT infrastructure to a hybrid-cloud technology, such as Azure.

- Integration of hybrid-cloud technology is expected to increase at rapid rates in 2018, with products by Microsoft leading the change.

- According to Bloomberg Intelligence, total tech spending in 2016 was equal to about $1.8 trillion, with about $86 billion invested into public-cloud technology.

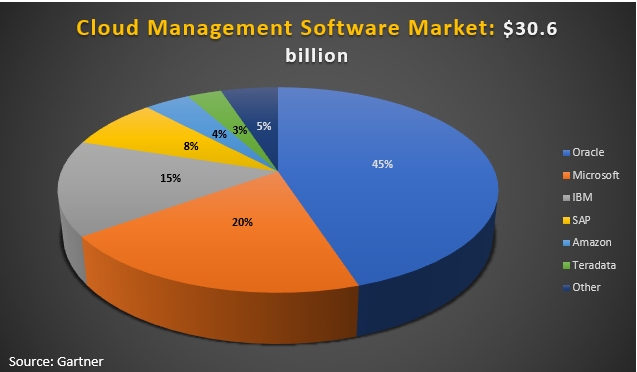

As Azure is adopted in the market at increasing rates, we can expect to see Microsoft's market share in the Cloud Management Software Market increase.

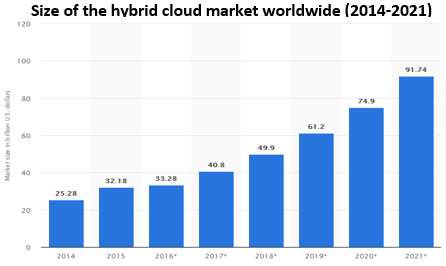

- The Hybrid-Cloud Market Worldwide is expected to increase from a $30 billion industry to around a $90 billion industry by 2021, according to Statista 2018.

- Based on this statistic, I expect that Microsoft will capture at least 20% of an approximately $90 billion market by FY 2021.

- I expect that market share to grow steadily through this time period.

Valuation

I used a discounted cash flow using free cash flow model as a valuation technique for Microsoft, which yielded an intrinsic value of $126.48 for Microsoft.

My assumptions include:

- A beta of 1.30, which was un-levered at the industry average and then re-levered at Microsoft's capital structure.

- Risk-free rate of 2.98%.

- Market risk premium of 7.25%.

- Terminal growth rate of 3%.

- WACC of 9.30%.

In my discounted cash flow model, sales are expected to grow at a 5.22% CAGR through FY 2028. The sales growth assumptions are highlighted below. The COGS and GP margins are held constant at about 34% and 66%, respectively, from FY 2019 to FY 2028. Operating expenses are relatively steady as well. EBIT is expected to grow at a 4.91% CAGR through FY 2028. All assumptions were based on management guidance and expected investments and growth in new and existing product lines.

The sensitivity analysis below shows that small permutations in my terminal growth rate and the WACC won't change my conclusion of Microsoft being undervalued. 25 out of 25 of the prices presented below show positive upside for Microsoft's share price.

Risks

General Economic Decline: A decline in economic activity could slow the pace at which several businesses and corporations decide to upgrade their IT infrastructure. However, it is important to note that IT infrastructure is a huge priority to many organizations for efficiency and security purposes.

Competition for Market Share: A major risk to the operations of Microsoft, which threaten the performance of cloud services such as Azure and Office 365, is the products offered by the company's competitors. If companies like Amazon (AMZN) and Oracle (ORCL) are able to develop more elaborate and effective cloud platforms, we can see a decrease in Microsoft's scale in the marketplace. A decrease in market share will negatively affect the company's financial margins.

Faulty Investments in New Products: Microsoft invests heavily in researching, developing, and designing, upgraded and new products and services. Because of Microsoft's established brands, many of these products and services are successful in achieving expected outcomes. But, many of them do run the risk of failure, which again will negatively affect the company and its financials.

Conclusion

Microsoft's strong financials and innovative prospects, in regards to Azure, Office 365, and other projects, make it a strong growth play.

Disclaimer: Information and opinions contained in this report have been obtained or derived from sources believed to be reliable, but no guarantees can be made regarding the accuracy of the information provided by the original sources. All opinions expressed are subject to change without notice. This research report is not tailored to the investment needs of any specific person and is provided for information purposes only.