The biggest risk to my bullish Apple (NASDAQ:AAPL) investment thesis now is whether the long-term growth story with Services is at risk due to weak iPhone sales. The actual generation of higher corporate margins due to the Services division promises to occur this year as long as the revenue equation doesn't shift dramatically from expectations. These higher margins will provide a catalyst for the cheap stock this Valentine's Day when investors are looking for a stock crush.

Image Source: Apple website

Limited Risk

Apple has grown Services at a fast clip for years. The business has now eclipsed the $10 billion quarterly rate and would be one of the largest businesses in the world as a standalone company.

At this size, Apple Services - which includes the App Store, Apple Music, Apple Pay and others - faces plenty of risk. Maybe not a risk of being replaced, but at least for the growth rate to slow and not contribute to the future of the tech giant.

The unit grew at another fast 19% clip during the December quarter that was hampered by market weakness and, especially, a slowdown in China that included a pause on approving new games that directly impacts App Store revenues.

AllianceBernstein's Toni Sacconaghi fears that enough customers will eventually leave the Apple app ecosystem to avoid the "Apple Tax." Several customers, including Nexflix (NFLX) and Epic Games, have made high-profile announcements that led Mr. Sacconaghi to have the following concerns:

Certainly, the headlines in the last few months haven't been encouraging. Netflix, Spotify (SPOT), and Fortnite have all stopped / threatened to stop paying the so-called 'Apple Tax' of 15 to 30 percent on App Store revenues.

These companies pay 30% for initial sales and 15% for ongoing subscriptions signed up via the App Store. Apple has 1.4 billion active device users, with 900 million of those using the iPhone. The promise of wearables like the Watch and its objective of becoming a medical device could further expand the revenue potential for subscriptions from Apple devices.

The key to the App Store story in the short run is that no individual app has a meaningful impact on revenues. Even despite the massive video streaming business of Netflix being on the path to generate more than $20 billion in revenues this year, the CFO is clear that no app even contributes 1% in annual App Store revenues.

On the FQ1 call, CFO Luca Maestri made the following statement about the risk of losing large app customers on the FQ1 earnings call:

In fact, more than 30,000 third-party subscription apps are available today on the App Store and the largest of them accounts for only 0.3% of our total Services revenue.

We're talking about the top mobile game and the top app that have made plans to avoid the costs of utilizing the App Store for discovery by the top consumers in the world. Most apps such as mobile games don't have the expertise or the name recognition to avoid paying a 30% fee in order to attract consumers. Being on the App Store provides the credibility and security to consumers when dealing with apps from unknown companies.

Margin Pressure For Now

My previous research pinned the Services gross margins at a lower level than what Apple reported for FQ1. The point of the original work was to demonstrate how even strong growth in high-margin Services was being swamped by the sheer size of the products division led by low-margin iPhones.

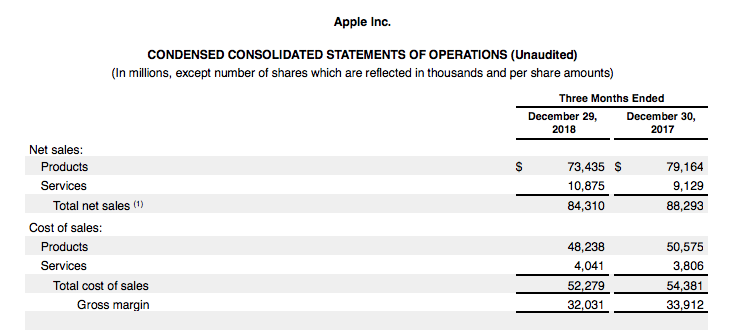

In the latest quarter, Apple provided the much-needed details on costs of sales for both Products and Services. Even with Services generating a gross margin of 62.8%, up from 58.3% last FQ1, iPhone sales weakness and margin pressure hurt the whole company and hid a huge jump in Services margins.

Source: Apple FQ1'19 earnings release

In FQ1, gross profit for Services actually jumped by $1.5 billion to $6.8 billion. All of the decline in corporate gross profits came from the weakness in iPhones that led the Products division to take a 180-basis point margin hit.

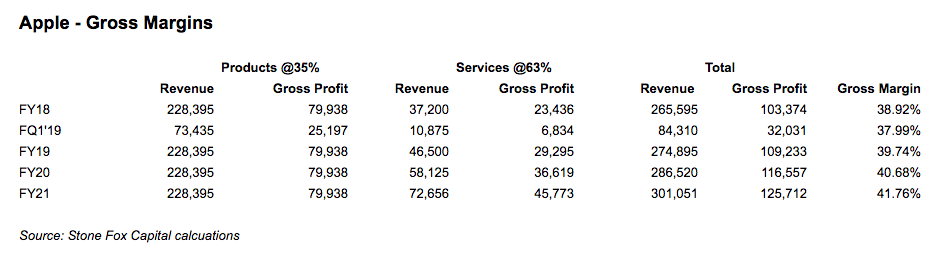

Going back to my previous margins work and using the 35% gross margin for Products and now using the new 63% for Services, the margin inflection point should take place to a larger extent this year.

Note, the spreadsheet uses 25% Services growth that's possible with China back to approving mobile games. Some risks exist to revenue estimates based on the weak FQ1 growth of only 19%. Also, the risk exists that the iPhone business doesn't rebound to recapture the 35% gross margin rate.

Upside potential exists that wearables eventually boosts Products revenue above the FY18 levels. In addition, some margin weakness in Products could be offset by higher margins by Services.

Just keeping revenue expectations equal with my work from November as gross margins accelerate from an expectation of crossing 40.0% in FY21 to now FY20. In addition, the gross margin reaches 41.8% in FY21, leading to a substantial boost to gross profits forecasts for FY21 in the $5 billion range.

Takeaway

The key investor takeaway is that Apple is definitely positioned to ride higher margins from Services to stronger corporate margins, and hence, gross profits. When combining higher profits with lower diluted share counts from a buyback targeted at $100 billion, shareholders will prosper with a large gain in EPS over the next few years.

Even after a rally to $170, Apple only trades at an EV of 11.1x FY20 EPS estimates of $12.75 that have plenty of upside potential from margin expansion. At this price, the stock is my Valentine's crush with a margin lift on the way.

Disclaimer: The information contained herein is for informational purposes only. Nothing in this article should be taken as a solicitation to purchase or sell securities. Before buying or selling any stock you should do your own research and reach your own conclusion or consult a financial advisor. Investing includes risks, including loss of principal.