Introduction

Intuit (NASDAQ:INTU) is one of our favourite software stocks and we initiated our coverage on the company on Seeking Alpha with a Buy recommendation last month (see "Intuit: Multi-Year Double-Digit Compounder"). The investor day held Thursday (03 Oct) provided more operational data and strategy details that add to our confidence in the Buy case, and we share the highlights below.

Reiterating Guidance

Intuit management reiterated the guidance for FY20, which included a 10-11% year-on-year revenue growth, a 10-12% (non-GAAP) EBIT growth and an 11-13% (non-GAAP) EPS growth - reassuring given concerns around a slowdown in the U.S. economy and wider global trade tensions over the last few months:

| Intuit FY20 Guidance NB. Intuit FY ends 31 Jul. Source: Intuit results press release (FY19Q4). |

For the medium term, the company continues to expect double-digit organic revenue growth and for operating income dollars to grow faster than revenues. Management also disclosed they have now formulated "bold" financial and operational targets for 2025, although these are not disclosed.

Improving Customer Retention

Intuit also shared operational data that showed both its Consumer and Small Business & Self Employed ("SBSE") segments have either maintained or improved their customer retention rates in their online offerings.

In the Consumer segment, the TurboTax Online flagship has improved its customer retention by 2% to 79% during FY19, after a similar 2% improvement during FY18;

| Intuit Customer Dynamics – TurboTax Online (Consumer)

|

In the SBSE segment, QuickBooks Online has maintained its customer retention at 79%, despite strong growth in the self-employed market, which typically has lower retention (49% in FY18):

| Intuit Customer Dynamics – QuickBooks Online (SBSE)

Source: Intuit investor day presentation (Oct-19). |

A high retention rate is important in laying the foundation for cross-selling extra products to customers and for growing customer numbers overall. It also reflects Intuit products' continuing competitiveness against rival offerings.

Strong QuickBooks Online Growth

The investor day also provided a more detailed breakdown on the 33% year-on-year growth in QuickBooks Online subscribers during FY19, with U.S. subscribers growing 25% year-on-year, and total non-US subscribers growing 58%, including a 78% year-on-year growth in the U.K.:

| QuickBooks Online Subscription Growth (FY19)

Source: Intuit investor day presentation (Oct-19). |

The strong growth in U.K. subscribers was helped by the U.K. government's "Make My Tax Digital" initiative. It is also particularly relevant because of the U.K.'s status as probably the most contested market between Intuit, incumbent Sage Group (OTC:SGGEF) and new disruptor Xero (OTCPK:XROLF). The U.K. is Sage's home market, and one of the first markets for Xero's international expansion; it is the second largest market by revenues for both companies.

QuickBooks Online's strong growth in the U.K. shows its ability to out-compete both Sage and Xero. With another year of near-80% growth (it grew subscribers by 84% in FY18), its U.K. subscriber number has likely overtaken Xero's. (QuickBooks Online had 545k subscribers as of July; Xero had 463k as of March and, assuming it also continued its prior-year growth rate of 48%, would only have reached 510k subscribers in July.)

Intuit cited one of the reasons behind its U.K. success as its status as the first product to be compliant with “Make My Tax Digital”, which is a sign of Intuit's superior R&D capabilities over competitors.

Broadening of QuickBooks Customer Pathways

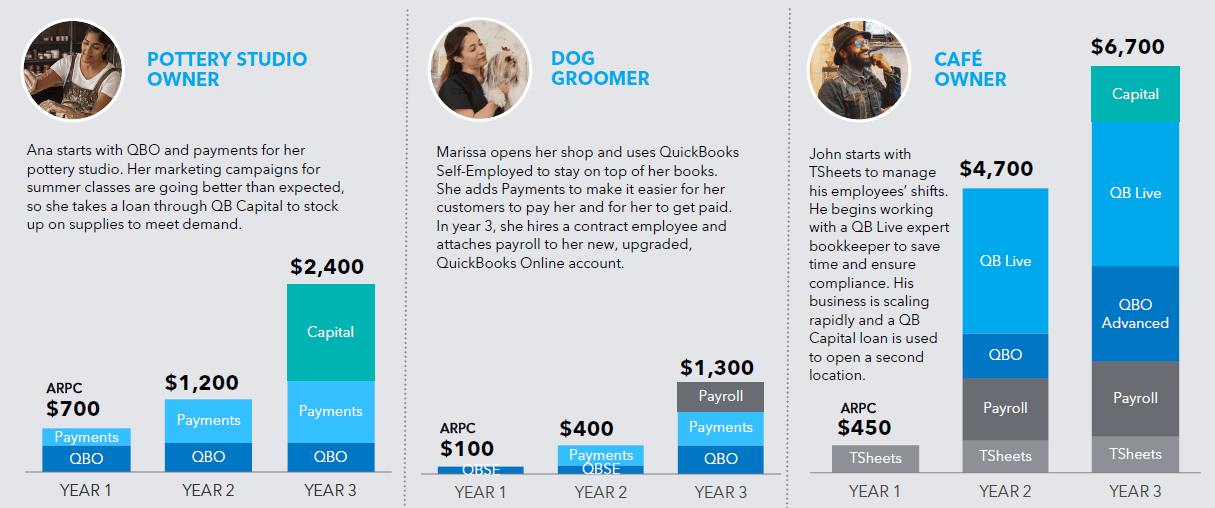

The investor day also covered how Intuit’s suite of products (including third-party apps on its open platform) has helped broaden the pathways by which customers join the Intuit platform and purchase more products over time.

Traditionally, QuickBooks customers have followed a path of buying accounting, payments and then payroll products:

| QuickBooks Customer Trajectory – Traditional

Source: Intuit investor day presentation (Oct-19). |

With more new products added, there are more pathways for customers to follow. Capital (i.e. small business finance) is an important cross-sell, and even customers who follow the traditional path of accounting, payments then payroll may start doing so earlier. In addition, products such as TSheets (employee scheduling) offer additional entry points onto the platform; 1.2m employees are on TSheets as of July, representing a growth of 60% year-on-year:

| QuickBooks Customer Trajectory – New Additions

Source: Intuit investor day presentation (Oct-19). |

Management also clarified its strategy towards third-party apps and its own apps on the Intuit platform. In general, Intuit would leave the choice to customers, allowing multiple apps (including its own) to be available. Development of its own apps will focus on its core competencies of payments, payroll, time-tracking and capital; "everything else we partner on".

Capital was also highlighted as a top-3 priority among small businesses (as shown below); cashflow was mentioned as the #1 cause for business failure among them. This confirms the potential of QuickBooks Capital, Intuit’s small business finance offering, which has made $441m worth of loans in the less than 2 years since it launched.

| Small Business & Self Employed Problems (Intuit View) Source: Intuit investor day presentation (Oct-19). |

Valuation

Since our Buy recommendation on 17 Sep, Intuit's share price has fallen 1.7% amid a wider market correction, but outperforming the S&P 500 and the NASDAQ over the same period:

| Intuit Share Price vs S&P 500 & NASDAQ (Since 17 Sep)

Source: Yahoo Finance (04-Oct-19). |

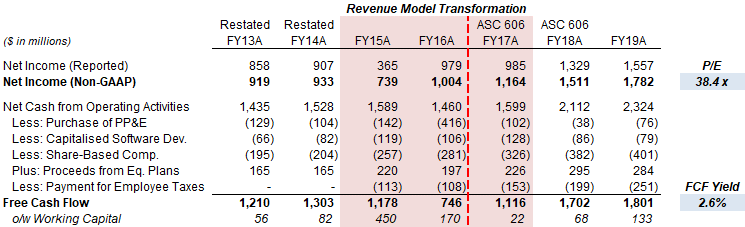

At $263.00, Intuit shares are trading on 38.4x P/E and a 2.6% FCF Yield; dividend yield is 0.8% (the annualised dividend is $2.12):

| Intuit Earnings, Cashflows & Valuation (FY13-19)

NB. Intuit changed its revenue model on QuickBooks and ProConnect in FY15. Source: Intuit company filings. |

As explained in our last article, Intuit’s high valuation multiples are justified by its sustainable low-teens EPS growth and its resilience during downturns.

Conclusion

Further operational data and strategy details from Intuit's investor day adds to our confidence on our Buy case.

We expect Intuit to continue its strong structural growth from a resilient existing customer base, large pools of new customers, and cross-selling extra products. We expect Intuit to deliver a low-teens annual return from a low-teens EPS growth, stable multiples and a 0.8% dividend yield.

We re-iterate our Buy recommendation.

Note: A track record of my past recommendations can be found here (updated).