Editor's note: Seeking Alpha is proud to welcome Vince Yeh as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA PREMIUM. Click here to find out more »

Editor's note: Seeking Alpha is proud to welcome Vince Yeh as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA PREMIUM. Click here to find out more »

Introduction

Bicycle Therapeutics is a disruptive new entrant in the oncological targeted drug delivery space. Their small molecule drug conjugate platform can fiercely compete with the highly clinically successful antibody-drug conjugates. In this article, I will highlight Bicycle’s competitive advantages and explain my long investment thesis.

Basis of Bicycle’s Technology

The basis of Bicycle’s technology is a novel iteration of phage display, where the short peptide sequences displayed on the end of the phage particle are chemically cyclized through appropriately spaced cysteine residues onto a small organic molecule scaffold to form bicyclic structures of various sizes and shapes. The advantages of this on-phage peptide cyclization are several-fold: 1) Bis-cyclized peptides can bind to proteins with much higher affinity and specificity than linear peptides or mono macrocycles. This is important as Bicycle is developing peptide drug conjugates to deliver toxins to cancer cells. They are relying on the bicyclic peptides to binding to specific cancer cell surface proteins tightly to concentrate drugs to cancer tissues and bypass healthy tissues that do not express such proteins. 2) Cyclized peptides make them harder to digest by proteases in the blood. This allows these compounds to be stable in circulation until it reaches the intended cell surface protein (e.g., cancer cells). 3) Because these bicyclic structures can be created in different sizes (e.g., one larger than the other, or tri-cyclic etc.), this significantly increases addressable chemical space, and therefore, increases the probability of finding tight binder to proteins. The theoretical chemical diversity of the Bicycle phage platform is 108 to 1010.

The following two figures from a Bicycle presentation nicely summarize the uniqueness and advantages of bicycle peptides. I provide further details in the science section towards the end of the article.

What has Bicycle done thus far? Are the data substantiating the thesis?

There are currently e.g., three clinical assets. Two in oncology based on targeted delivery of toxins and one in ophthalmology partnered with Oxurion. I will walk through the highlights of each one and provide my own take.

BT1718 – BT1718 targets a tumor cell surface protein, the tumor-associated membrane type 1 matrix metalloproteinase MT1-MMP (or MMP-14). MT1-MMP is overexpressed in many tumor types e.g. Lung (NSCLC, 58%), breast (TNBC, 76%), bladder (95%), ovarian (96%), endometrial (100%). The figure below from The Cancer Genome Atlas shows the expression levels of MT1-MMP in a variety of cancer types. This means that this product can be used in a fairly large number of patients. On the back of the envelope calculation for the addressable patient population: NSCLC, 191K patients per year * 58% MT1-MMP positive ~ 110K patients per year. TNBC ~ 76K patients, bladder ~ 70K patients, and ovarian ~ 21K patients. The numbers are based only on US cancer incidences. If we assume $100K per year of typical ADC costs, we are looking at > $28 billion/year total potential addressable market for this product alone.

MT1-MMP RNA levels in various cancer types. Data from Human Protein Atlas

BT1718 is composed of a highly specific and potent MT1-MMP targeting bicyclic peptide conjugated with a potent toxin mertansin DM1. DM1 incidentally is a clinically validated toxin used in Trastuzumab emtansine (Kadcyla, marketed by Roche). Using a clinically validated toxin such as mertansin de-risks some of the clinical uncertainties of BT1718. Since we know from previous clinical ADC studies, DM1 is known to kill tumor cells in patients, and in many cases, extending survival time. Bicycle has published the MT1-MMP targeting imaging reagent that demonstrated high tumor uptake and retention vs normal tissues and outperformance as compared to an MT1 targeting antibody. The results from the paper provided pre-clinical validations of their technology, and the imaging reagent can presumably be used as companion patient selection tool for BT1718.

In a recent ESMO 2019 conference disclosure, the company provided a preliminary Ph1 readout of BT1718. The compound showed high tumor concentration of active drug DM1 (sampled via biopsy) and rapid systemic clearance of BT1718 which replicated their pre-clinical results in animal models hence validating that the technology is translatable from animals to humans.

Encouragingly, BT1718 is showing tumor size reduction in a number of lesions, and that has led to stable disease in 54% of patients in 8 weeks of treatment. Through this study, the company has further refined their patient selection strategy of enriching Ph2 patients with squamous cancers with higher than 150 in H-Score. As in all early oncology trials, these results can only be taken with faint enthusiasm as they need to be expanded and duplicated in many more patients and tumor types. Human tumors are a lot more heterogeneous and complex than animal models. All I can take away at this point is that the bicycle peptide drug conjugates can deliver and concentrate toxin drug DM1 in tumor lesions in concentrations similar to animal models. Going forward, I will be keenly watching clinical trial results that show treatment with BT1718 can lead to significant tumor size reduction hence leading to patient survival.

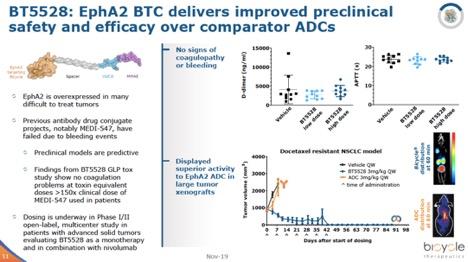

BT5528 – This peptide toxin conjugate targets EPH A2 receptor, a cell surface receptor involved development events in normal biology, but highly expressed in several hard to treat cancers such as NSCLC and cervical cancer. The construct of BT5528 contains another clinically well-validated toxin MMAE, which incidentally is the active component of Seattle Genetics’ highly successful ADCETRIS. Using these clinically validated cytotoxins such as MMAE and maytansinoid DM1 as drug payloads significantly reduce clinical development risks. The company is not exploring unknown cancer-killing mechanisms. Hence, Bicycle only needs to demonstrate in the clinic that their peptide-based conjugates can consistently deliver sufficient drugs to shrink tumors and have lower adverse events as compared to ADCs carrying these toxins.

EPH A2 receptor RNA levels in various cancer types. Data from Human Protein Atlas

Bi-specifics, the next value driver?

As a primer, bi-specifics is a term given to biologic based therapies that can bind to two specific proteins at the same time. Typically, they are highly engineered monoclonal antibodies with one Fab region binding to a protein of interest and another Fab region binding to another distinct protein. The most studied of bi-specific in the clinic is Amgen’s immune-oncology drug Blincyto for the treatment of acute lymphoblastic leukemia (ALL). The drug bridges T cells (via CD3) to ALL cells (via CD19), causing T cells to kill ALL cells. Bi-specifics is a vast area of drug development and can address numerous unmet medical needs.

As far as I know, Bicycle is the only company out there developing small molecule-based bi-specifics (MW < 2-3 kDa) thus far. Since they are based on the company’s proprietary bicyclic peptides, they share some of the aforementioned advantages: extensive tissue permeation and distribution, ease of synthesis and manufacture, etc.

Their first bicycle bi-specific targets tumor antigen nectin-4 on one arm, and simultaneously activates CD137 (4-1BB). This compound is designed to bring activated CD4 and CD8 T cells, dendritic, and natural killer cells to tumor expressing nectin-4, causing tumor cell death and hopefully, immune memory hence preventing tumor recurrence. The company has shown some very encouraging preliminary data in their latest investor deck, but I will be keenly reading their scientific publication when it comes out.

In my opinion, bi-specific drugs, if it works in the clinic, can be a lot more value-creating than bicycle-toxin conjugates since these products can, in theory, produce durable clinical responses or even cures in cancer as seen in other immune-oncology drugs such as Keytruda & Optivo. Therefore, bi-specifics can provide a substantial upside optionality for Bicycle.

Beyond oncology

Plasma kallikrein inhibitor for diabetic macular edema (DME). This target is one of the first applications that the Bicycle technology founder Christian Heinis and Greg Winter published demonstrating the flexibility and specificity of the peptide display technology. The market for disease-modifying treatments for DME is vast. For example, Eylea, one of the anti-VEGF treatments, will likely reach $4.7 billion in sales in 2019. Bicycle has disclosed some preliminary results in their deck, but I will be closely watching their scientific publications in this area.

Big pharma and biotech collaborations

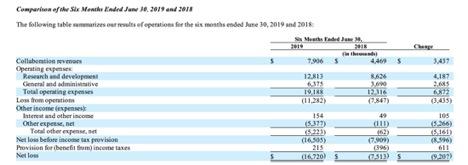

Big pharmas such as Astra Zeneca Sanofi have recognized the potential of Bicycle’s platform in generating new drug leads. Research collaborations have been structured with two large pharmas and other biotech entities. For example, in Astra’s case, Bicycle will screen for targets in respiratory and metabolic disease spaces. Bicycle has earned $7.9 million for the first half of 2019, which helped off-set 40% of their operating expenses. Table below from 2019 second quarter 10Q.

Valuation

Since Bicycle has insignificant revenues at this moment, I will be using comparable companies that have been sold to big pharmas as guideposts for valuation. The current market cap is $150 million and an enterprise value of only ~ $60 million I think the market improperly assigns the probability of success of Bicycle assets hence awarding the company miniscule valuation. An investor based on current valuation will likely see multiple fold upside if the company delivers even the base case scenario.

Bull case – $5.4 billion in valuation. 36-fold upside based on current valuation. To reach such a valuation, I make the following assumptions: BT1716 shows positive Ph2 clinical results comparable to an ADC such as Immunomedics’ sacituzumab govitecan. Bi-specific BT7480 shows positive Ph2 data similar to Micromet’s Blinatumomab, and kallikrein inhibitor THR-149 shows positive results in a Ph2 trial in DME. The comparable transactions are the following: Novartis purchase of Endocyte (an SMDC company) for $2.1 billion. Amgen’s purchase of Micromet for $1.16 billion in 2012. This deal was done a while ago, if Bicycle shows good traction of their bi-specific in the clinic, the valuation should be much higher. And finally, a recent UCB purchase of Ra Pharmaceuticals for $2.1 billion. Ra pharma owns a competitive peptide display platform with a successful C5 inhibitor program in Ph2. If all three Bicycle assets show promising Ph2 results, in principle Bicycle can command a similar sum of each transaction values.

Base case – $2.1 billion in valuation. 14-fold upside based on current valuation. To reach such valuation, I assume that only one of their peptide toxin conjugates shows traction in Ph2 trial hence reaching a similar level as Novartis purchase of Endocyte.

Bear case – $100 million in valuation or lower. >-30% based on current valuation. To reach such valuation, I assume that their lead asset BT1718 fails in Ph2 and the company needs to raise cash to pivot to radio nuclei conjugate for example, and market sells off shares to cash level or below. Endocyte endured this kind of gut-wrenching drop before their pivot.

Bicycle’s balance sheet and future funding needs

Bicycle’s has ~ 110 million in current assets on its balance sheet which is healthy for newly IPOed biotech. Their cash used for operations for the first nine months of 2019 is ~ 23 million. I assume their cash burn of approximately 30 million and 40 million for 2019 and 2020 respectively. Therefore, Bicycle may have a little over two years of funding before the next funding raise. The ideal scenario is that BT1718 and/or BT5528 show robust Ph2 results a couple of years out which should allow them to sell shares at much higher prices to raise enough funds to reach FDA approval.

Management: Bicycle is managed by an experienced team

CEO – Kevin Lee. A former Pfizer veteran where he served as senior vice president and chief scientific officer of the Rare Disease Research Unit. In that role, he held responsibility for more than 20 novel programs across the full spectrum of research and development, established Pfizer’s rare disease strategy, conceptualized and implemented the company’s gene therapy strategy with the creation of the Genetic Medicine Institute and founded the Rare Disease Research Consortium.

CSO – Nick Keen. He joined Bicycle from Novartis, where for the past five years he served as the Cambridge (U.S.) head of oncology research. During his tenure at Novartis, Nick was responsible for leading research from basic target identification and drug discovery through to enabling early clinical trials.

Chairman - Pierre Legault, MBA, CPA, is an experienced biotech veteran. In addition to Bicycle, Pierre is the Chairman of Poxel, a biopharmaceutical company developing innovative drugs for metabolic diseases, including type 2 diabetes and non-alcoholic steatohepatitis. He is chairman of Artios, a DNA damage repair company. Pierre is also a member of the board of directors of Clementia Pharmaceuticals, Urovant Sciences and Syndax Pharmaceuticals. In the past, he was a member of the board of directors at Forest Laboratories, Tobira Therapeutics, NPS Pharmaceuticals, Regado Biosciences, Armo Biosciences, Iroko Pharmaceuticals, Cyclacel Pharmaceuticals, Eckerd Pharmacy and Nephrogenex, where he also served as the chairman and chief executive officer from 2012 to 2016. From 2010 to 2012, Pierre served as the CEO of Prosidion.

Science and Technology Deep Dive

In 1966 Hollywood produced a movie named “Fantastic Voyage” where the plot depicted the journey of a group of miniaturized scientists traveling through a comatose patient’s circulation system to find and fix a clot in the patient’s brain. Although we do not have the miniaturized submarines to drive physicians to the diseased tissue for repair yet, medical scientists have been working on tissue targeted delivery of medicine for a very long time. The need is none higher than in the oncology area where most used medicine are highly toxic compounds to kill the diseased cancer cells. The first class of targeted drugs are antibody drug conjugates (ADC), where highly toxic small molecule payloads are attached to antibodies. The payloads are designed to release in cancer cells selectively. As of writing, there are six ADCs approved for various cancers and the leader of this class of compounds, Seattle Genetics has built themselves into a highly successful enterprise (EV ~ $17.5 billion).

Limitations of ADCs and how small molecule drug conjugates can address

The biotech industry has gravitated towards antibodies as a delivery vehicle is mainly two-fold, 1) the vast combinatorial diversity of mammalian immune system allows scientists to raise tight binding antibodies to practically any antigen one can imagine. In the case of cancer, most studied antigens are cancer-specific or over-expressed tumor cell surface proteins, think HER2 or EGFR. 2) IGg antibodies is one of the first class of proteins that the biotech industry figured out how to engineer proficiently on an industrial scale. Pioneers such as Genentech and Amgen have built huge enterprises based on their antibody therapies such as rituximab or trastuzumab. The clinical outcome of ADC treatments in hematological cancers has been impressive. As five out of six approved ADCs thus far are for various blood cancers, the clinical efficacy for solid tumors, on the other hand, is spottier. Numerous empirical and theoretical evidence have been provided to explain this, the most convincing data that I have seen suggest insufficient ADC distribution to the tumor masses. For an ADC to be efficacious, it needs to reach vast amounts of tumor cells within the main mass or metathesis sites. The ADC needs to 1) survive circulation to reach tumor capillaries, 2)Extravasate (diffuse out of capillary layer), 3) Diffuse throughout the tumor mass and bind to the cell surface antigens, and 4) Internalize and efficiently release toxin payload. All these variables need to go right, as any point of failure can lead to treatment failure or even worse, causing tumor to further mutate and evade ADCs or other treatments. Further challenges mount up as numerous solid tumors such as pancreatic and certain breast cancers, for example, exhibit desmoplasia (a large amount of fibrous connective scar tissues) and high interstitial pressure. This phenomenon poses considerable challenges in ADC extravasation and efficient diffusion and maybe some of the causes of insufficient ADC concentration in solid tumors. In addition to challenges in efficacy, ADCs also pose challenges in the safety and tolerability front. ADCs typically have circulation half-lives of weeks. Patients have potent toxins floating in their system for weeks on end. More troubling yet, IGg antibodies are taken up by any cell in the body through salvage recycling by the neonatal Fc receptor (FcRn) pathway. In that recycling process, toxins on the antibody can fall off and causing cell death in healthy cells with Fc receptors.

These issues stated above are where Bicycle Therapeutics aims to solve with SMDCs.

Small vs. big

In terms of molecular weight, small molecule drug conjugates (SMDCs) typically range one to two kDa vs. ADCs ~ 150 kDa, greater than 100 x smaller in size difference. Due to the size difference and other properties, SMDCs have two major advantages as compared to the ADCs.

1) SMDCs can permeate tumor tissues more thoroughly and rapidly than ADCs leading to potential better antitumor efficacy. Several research groups such as Neri at ETH and Bicycle and their academic collaborators have published papers where they do side by side comparison of ADC vs. SMDC targeting the same antigen in animal models and show that SMDCs can deliver more drugs to tumors vs. ADCs. See the data below as an example from a Neri paper.

2) SMDCs can have higher safety margins than ADCs. SMDCs typically have circulation half-lives around half an hour to an hour and are eliminated from the system via the kidneys through urination. On the other hand, ADC usually have half-live of weeks and are cleared through liver and macrophage metabolism. Long half-lives expose patients to toxic drugs for prolonged periods, and antibody metabolism in the liver can lead to drug release in un-intended organs.

Are there examples of SMDC success in the clinic?

The first peptide drug conjugate that made it to the market place is Lutathera, a somatostatin receptor targeting peptide conjugated with radioactive metal lutetium 177 for the treatment of gasteroenteropancreatic neuroendocrine tumors. Past clinical results of Lutathera demonstrated that the peptide drug conjugate indeed concentrates in the tumor, and radioactive metal selectively kills tumor cells. Novartis purchased the company that developed Lutathera, Advanced Accelerator Applications, for $3.9 billion in late 2017. This drug proved to be a commercial success with ~ $1 billion in sales in 2019. To further expand the targeted SMDC pipeline in late 2018, Novartis purchased another SMDC company Endocyte for $2.1 billion to gain access to PSMA targeting radionucleotide drug conjugate PSMA-617 for the treatment of metastatic prostate cancer.

Although Bicycle is not actively pursuing the development of radionucleotide conjugates in the clinic, the company has published pre-clinical papers with the radioligand pioneers Haberkorn of Heidelburg University that demonstrated effective tumor targeting of their MT1-MMP targeting ligand. In principle, ligands discovered through Bicycle’s phage display technology can easily be converted to tumor-targeting radionuclide conjugates.

Comparable companies and potential competitors

ADC companies

Bicycle play in the targeted drug delivery, especially in oncology. Therefore, any ADC company is a competitor. As stated above, Bicycle SMDC profiles are completely different than all the ADCs in the clinic, but several ADC companies have very advanced development candidates and can gain a significant foothold in the market place as Bicycle products work their way through the clinics. If and when the Bicycle products gain approval, in addition to competing on scientific merits (efficacy, safety etc.), they will also need to compete with ADC companies entrenched salesforce, insurance reimbursement, and physicians’ prescribing habits, etc.

ADC products that are close to the finish line

Immunomedics (IMMU)- sacituzumab govitecan is a TROP-2 targeting ADC currently being re-submitted for approval for third line TNBC. Similar to MT1-MMP (target of BT1718), TROP-2 is a none specific tumor cell surface target, meaning several tumors over-express this protein. Therefore, sacituzumab govitecan can be used to treat several cancer indications, and it is being develop for HR+/HER2- breast cancer (Ph3), and urothelial (Ph2), etc. Currently, IMMU has an EV ~ $3.5 billion. I assign >90% probability of success in FDA approval.

Seattle Genetics (SGEN)- Enfortumab vedotin is the first agent to target Nectin-4, which is expressed on many solid tumors, with especially uniform expression on bladder cancers. This product received FDA Breakthrough Therapy Designation (March 2018) and is currently in Ph3. This compound competes directly with Bicycle’s BT8009 currently pre-clinical.

Peptide display companies

Aside from phage display, there are other peptide display techniques. Most notably, mRNA peptide display techniques invented by Nobel prize winner Szostak’s group. Similar to Bicycle’s phage display, mRNA display produces vast libraries of cyclic peptides (mostly mono-cyclic), which allow scientists to screen for tight protein binders. There are currently two main companies developing this technology.

Peptidream (4587.T-JP:Tokyo Stock Exchange) – This is a Tokyo based company founded on professor Suga’s inventions. Unlike Bicycle, Peptidream is already profitable and supports a sizable market cap of $5.8 billion. Peptidream licenses its peptide display technology to a host of big pharmas (Merck, Novartis, Genetech, etc.) and charges a healthy fee. Although they do not explicitly state their drug development status, their many partners are in early developments of several peptide drugs and peptide drug conjugates. I view this company as the most direct and fierce competitor to Bicycle.

Ra pharmaceuticals (RARX) – This is a Cambridge, MA based company founded on Szostak’s technologies. Instead of pursuing cancer therapies, Ra is developing complement C5 inhibitors to compete with Alexion’s Soliris. Due to their recent clinical trial success of Zilucoplan, Ra was purchased by Belgium’s UCB pharma for $2.1 billion. Since UCB does not have an oncology franchise, I do not view RARX as a direct competitor of Bicycle.

Final thoughts

I rate Bicycle shares a buy. I think the market does not fully understand the potential of Bicycle’s technology platform and the probability of their clinical assets succeeding in trials. As stated above, the toxin drugs that Bicycle is using for the first two SMDCs in the clinic are highly validated. In addition, SMDCs such as Lutathera has already demonstrated clinical and commercial success. One can infer the current EV is tiny as compared to the potential addressable markets of Bicycle’s products. As with any early-stage publicly traded biotech shares, I expect the share prices to be highly volatile. I have started an initial position and will add when the company shows further progress in the clinics. I plan to hold shares for at least three to five years.