This article was highlighted for PRO subscribers, Seeking Alpha's service for professional investors. Find out how you can get the best content on Seeking Alpha here.

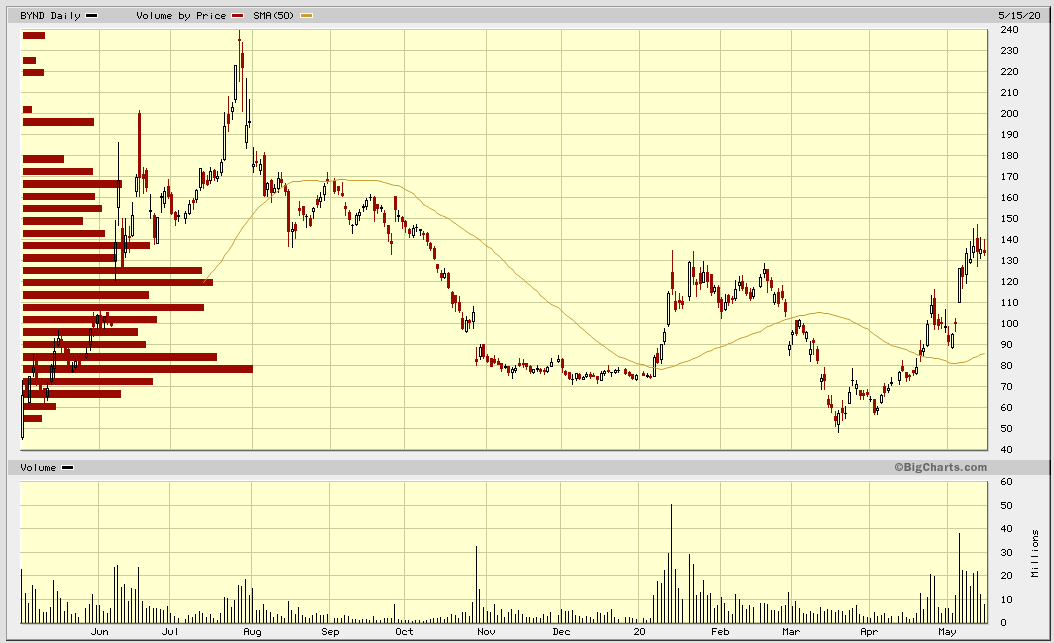

Beyond Meat's (NASDAQ:BYND) stock price has had a wild ride over the past year, with stock trading back into the $140's last week after having traded as low as $50 in March. As I explain in this article, I think the current price is markedly over-valued and I am short the stock as a result. Let's see why the stock has run up and why it may only be temporary.

(image source)

Why The Stock Is Up

In addition to bouncing off of the pandemic lows along with most stocks, BYND has benefited from two other factors.

1. Meat shortages

First and foremost, BYND is seen to benefit from the large number of temporary closings of meat processing plants which have caused local meat shortages and have forced farmers to euthanize parts of their herds.

The Wall Street Journal has a good write-up on this, which includes the following excerpts (all emphasis mine) and graph:

With meat shortages hitting burger chains like Wendy’s Co., what can shoppers expect at their grocery store’s meat counter?

The coronavirus pandemic has disrupted production at U.S. meatpacking plants, leading to higher prices and scarcity for popular items like ground beef and chicken breasts in supermarket meat cases. Grocers, seeking to head off panic buying, have begun limiting purchases and say they are preparing for intermittent shortages through May if not longer.

These shortages may intensify in the coming weeks given the lag between production at the slaughterhouses and distribution to stores. That means shoppers can expect higher prices, slimmed-down selections and nudges to choose plant-based meat alternatives or less popular cuts like sirloin steak.

[...]

Around 20 major meatpacking plants have temporarily closed during the past several weeks due to Covid-19 outbreaks among employees, cutting U.S. beef and pork production last week by about 35% from the same period last year, according to the U.S. Department of Agriculture. Agricultural lender CoBank estimated chicken production fell 7%.

Last week, President Trump issued an executive order that gave the U.S. Department of Agriculture greater discretion over meatpacking plants, allowing them to continue operating and shielding them from state and local pressure to shut down due to Covid-19 outbreaks among workers. Some plants remain closed and others only partially staffed, industry officials said, reducing overall meat production.

[...]

Overall retail prices of fresh meat, including beef, pork and poultry, have increased about 8.1% year-over-year for the week ended April 25, according to Nielsen. For the week ended Jan. 4, meat prices had been up 2.2% year-over-year.

(image source, graph is giving the yoy price change in any given week)

An 8% increase in prices is noticeable to consumers, particularly when many have lost their jobs, but it still doesn't close the price gap to the more expensive Beyond Meat plant based protein alternatives. Moreover, meat prices should drop in a few months when processing plants return to a semblance of normalcy and when farmers get back into a production equilibrium. Thus I expect that this factor will produce at most a small and temporary demand increase for BYND and the other alternative protein producers.

2. Cramer Endorsement / Only Pure Play Available

A second, more important factor in my opinion, is the new demand from new shelter-in-place day traders. As I've noted in previous articles, BYND is the only pure play stock in the alternative protein space, and hence when sentiment for the space increases, all the money is funneled into a single stock. That's what we're seeing now.

For example, Jim Cramer is a particular favorite guru among day traders and he has been high on the stock since mid April. Here's a CNBC story from May 6th discussing why Cramer is recommending the space. I've reproduced a few excerpts below (again all emphasis is mine):

CNBC’s Jim Cramer said Wednesday that investors cannot ignore the rising popularity of plant-based meat products.

“This movement is happening. You’ve got to get on the bus or ... get left behind,” Cramer said on “Squawk on the Street.”

[...]

“I think there are people who are getting appalled by what’s happened at the meat packers. ... I think these stories make you become not necessarily vegetarian but to think twice about beef,” Cramer said. “If you think twice about beef and then you try to Beyond, you kind of realize it’s very, very similar.”

While plant-based meat options have typically been more expensive than traditional meat, Cramer said the rising costs of beef, in particular, due to the coronavirus represents an opportunity for alternative producers.

He's reiterated this thesis almost everyday since, including this past Friday:

What do money managers get wrong when trying to value stocks like Beyond Meat (BYND)? They only look at the company through the four walls of the spreadsheet instead of looking at the scale of the opportunity.

Cramer said Beyond Meat justifies its valuation because it's more than just a company, it's an ethos. As meat packing plants struggle with coronavirus outbreaks, Beyond Meat has responded by lowering prices to take market share and introduce its healthier alternative to more consumers. It's not only what millennials want, it's what they're investing in.

Beyond Meat is the Tesla (TSLA) of food, Cramer continued, just as Shopify (SHOP) is for e-commerce. All of these companies have followings and market opportunities far greater than traditional metrics can calculate, and that's why their stocks continue to soar.

The result of these types of recommendations has been a marked increase in small traders holding the stock, as evidenced by the following RobinHood graphic.

(image source)

As I've argued above, I think the meat packing disruption will be short-lived and we'll soon see a return to a semblance of normalcy in meat supplies and meat prices. That will mean this particular impetus for traders to buy BYND will be short-lived. And once gurus are no longer pumping the stock, selling pressure from short term traders will begin to outweigh the long term underlying demand for the stock.

I do believe however, that Cramer has a point that BYND is a story stock and thus agree with his take "It's not only what millennials want, it's what they're investing in."

To me that means BYND will always sport a premium valuation, but it doesn't mean the recent price spike is sustainable.

And there are other reasons to be negative on stock, chief among them:

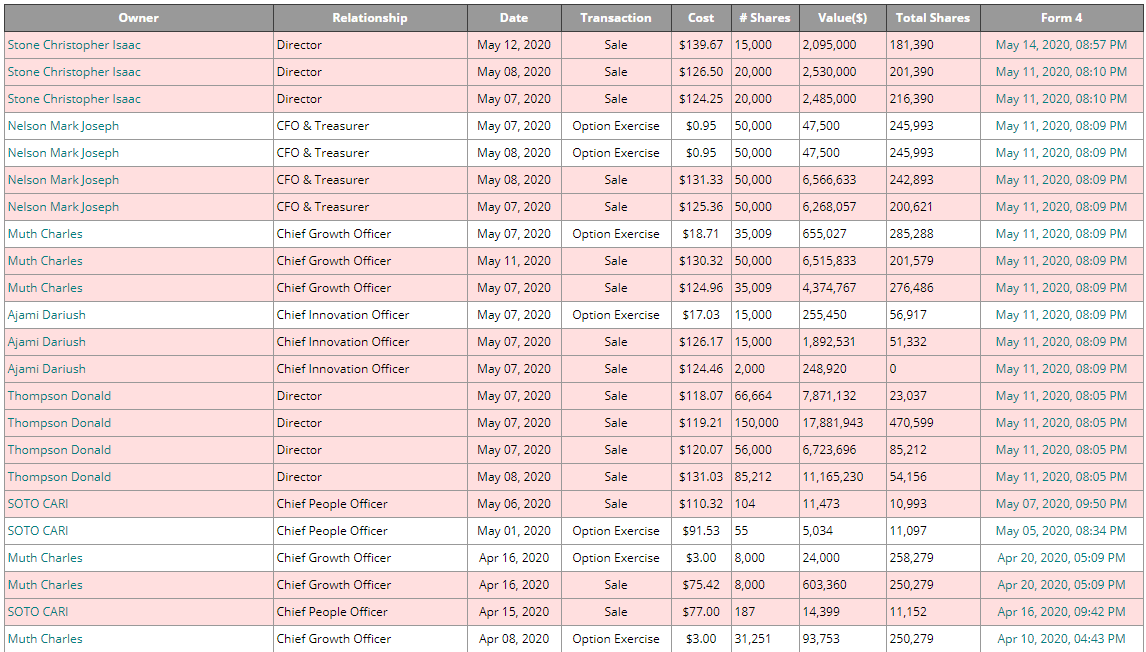

Insider Selling

It is often said "watch what they're doing, not what they're saying". Thus no matter how sanguine BYND insiders may sound, what counts is their accelerated selling. Here's a look at the insider transactions for the complete 1st Quarter and only the first half of the 2nd Quarter. Notice the steady selling that's been increasing rapidly lately:

(image source, BYND insider sales Q1 2020)

(image source, BYND insider sales Q2 to date 2020)

Competition Heats Up in Retail Stores

Another reason to be negative on the stock is the continued incursion into retail by BYND's competitors. (Recall that in the early days, BYND had the space almost entirely to itself.)

Most important is Impossible Foods' substantial expansion. I had previously written about Impossible entering select premium grocery stores, but now the rollout is much larger. As reported by TechCrunch on April 16, 2020 with my emphasis:

Starting tomorrow, 777 supermarkets in California, Illinois, Indiana, Iowa and Nevada will begin stocking the Impossible Foods plant-based meat substitute.

Fueling the increased distribution and a push to expand its product suite and geographic footprint domestically and internationally is a $500 million round of funding the company closed in March.

Some of that money is supporting the company’s debut at stores like Albertsons, Jewel-Osco, Pavilions, Safeway and Vons.

In all, the company said it would be in nearly 1,000 grocery stores by tomorrow. That includes all Albertsons, Vons, Pavilions and Gelson’s Markets in Southern California; all Safeway stores in Northern California and Nevada; Jewel-Osco stores in Chicago, eastern Iowa and northwest Indiana; Wegmans stores on the East Coast and Fairway markets in and around New York.

Since its debut in September, the company said it was the number one item sold at the locations it was available on the East and West coasts.

That expansion accelerated, when on May 6th, Impossible increased its penetration into the Kroger chain of retail stores. According to the vegconomist with my emphasis:

Impossible Foods is accelerating its retail expansion this week with the rollout of its flagship product at more than 1,700 grocery stores nationwide owned by The Kroger Co. The Impossible Burger rollout represents an 18-fold increase in Impossible Foods’ retail footprint so far in 2020.

In addition to being stocked on the shelves of Kroger-owned stores, the largest grocery retailer in the US, the Impossible Burger is now available online through kroger.com for Kroger Curbside Pickup and Delivery.

The company’s award-winning, plant-based meat is now on shelves in about 2,700 US grocery stores and through select online ordering systems

This will continue to put pressure on BYND's retail sales and margins.

I've provided snapshots from local Pavilions as part of my ongoing coverage of BYND and here are the offerings as of May 17, 2020:

(author's image, Pavilions mid shelf elevation May 17, 2020)

(author's image, Pavilions bottom shelf May 17, 2020)

(author's image, Pavilions bottom shelf May 17, 2020)

BYND has the most shelf space, but it's not particularly appealingly presented.

The Laura's offering is new to me, though admittedly I'm not shopping nearly as often given our shelter at home restrictions. In any case, there's no evidence that BYND's product is an overwhelming consumer favorite.

Taste Test

Conveniently, a recent taste test included all three of the brands stocked by Pavilions. The results of that test of four products conducted by myrecipes showed the LightLife product to be the winner, with BYND in third place and Laura's in fourth. Here are excerpts from the review of the LightLife and BYND products:

Best OverallLightlife’s Plant-Based Burger ($5.99 for 2)

We’ll be honest: it’s still not Angus. But Lightlife’s plant-based burger definitely has the most beef-like texture out of the options we tried. It also lacks any kind of strange aftertaste. At $3 a piece, these burgers are a little pricey, but they’ll beat the cost of one of these plant-based burgers at any fast food joint that might be serving them.

Most Visually Like Meat

Beyond Meat’s Beyond Burger ($4.99 for 2)

Since Beyond Meat is one of the big contenders in the meat-replacement arena, we were kind of excited to try this option out. To its credit, it definitely looks the most like a burger; the company even manages to somehow mimic fat marbling in the pea protein burger. But Beyond Burgers have a weird smell before they’re cooked, and kind of a strange aftertaste. It’s not quite off-putting enough to make it unappetizing, but it definitely detracts from the fantastic first impression that Beyond Meat gives. And since one of our tasters described the patty as “a raw burger fully cooked,” it’s possible that the texture could use a bit more tweaking.

For those interested, the LightLife product is made by Maple Leaf Foods (OTCPK:MLFNF) which is publicly traded (though LightLife is a small division of the company so the stock isn't a pure play on the space).

Valuation

Not to overplay the spreadsheet aspect that Cramer criticized above, but it's worth remembering that with the stock trading at $134.16, BYND is valued at 21X sales and with a EV/EBITDA ratio of 366. Even at a growth rate of 200% (which will be declining rapidly over the next four quarters as large customer gains are included in previous year's numbers) these are unsupportable valuation metrics.

(image source)

Trading Plan

I am short BYND, and have mentally divided my short into a trading basket and a long term basket. With the former shares I hope to cover in the $80's and $90's, while I plan to hold the latter shares for an eventual price target of sub $40.