Source: Google Images

An examination of the consumer-defensive investment segment reveals a venerable all weather portfolio asset. Brown-Forman (NYSE:BF.B) remains a fantastic Blue-Chip Stock in the alcoholic beverages industry with prominent consumer staple brands ranging from Jack Daniel's, Woodford Reserve, Herradura, Old Forester, Finlandia, among others. BF.B is one of the largest American owned companies in the spirit and wine business having been in business for over 150 years. The company operates in over 170 countries, the U.S being their primary market comprising roughly 50% of total revenues. BF.B offers investors an economically durable investment asset, a stable dividend, venerable capital appreciation, and a encouraging long-term growth outlook. This article will outline my bullish investment thesis on BF.B, discuss the characteristics of this great investment, as well as analyze pertinent financial and valuation data.

Investment Thesis

Brown-Forman persists as a force to be reckoned with in the liquor and spirits business. Although widely recognized for the company's Jack Daniel's Whiskey, BF.B has a vast product portfolio that extends to every segment of the liquor market whether it be tequila, whiskey, vodka, wine, or liqueur. BF.B's product portfolio boasts prominent spirit brands ranging from Jack Daniel's, Gentleman Jack, Old Forester, and Woodford Reserve. BF.B's popular Jack Daniel's product line remains a core asset of its liquor business, with Jack Daniel related products comprising 78% of every nine liters sold. Despite Jack Daniel's being the market leader in the United States, the brand continues to drive consistent mid single digit sales growth of around 5-6% annually, reinforcing the quality and high consumer demand for BF.B whiskey. BF.B has demonstrated a track record of enduring product innovation as the company has expanded upon its signature Jack Daniel's brand with flavorful variants ranging from Gentlemen Jack, Tennessee Fire, Single Barrel Select, and Tennessee Honey. BF.B also benefits from significant brand recognition. Having been in business for over 150 years, BF.B has cultivated a strong brand reputation for quality spirits, allowing the company to benefit from enduring customer loyalties.

Source: Brown-Forman

Source: Brown-Forman

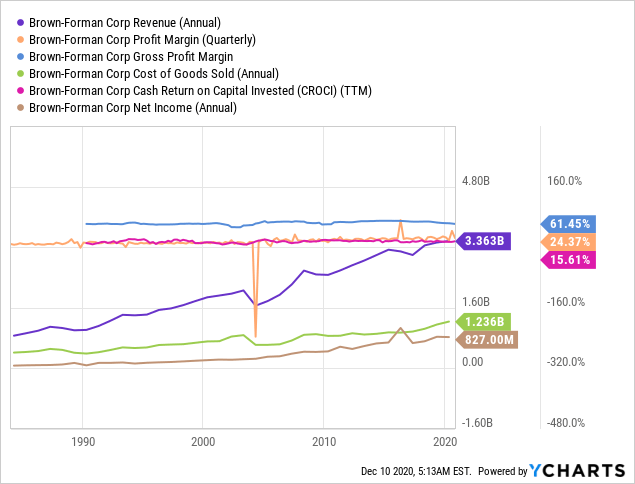

From a industry standpoint, the liquor business offers its own unique advantages over other types of businesses. The liquor sector benefits from steady product demand, limited product and operating expenditures, high profit margins, and steady revenue expansion opportunities. The liquor business boasts astronomical profit margins due to low operational expenses: requiring outlays really only on new product experimentation, marketing, low cost product materials, and a bottling and distribution network. BF.B has consistently expanded profit margins over time and boasts an attractive gross profit margin of 67% and 23% net profit margin. In addition to high margins, BF.B takes advantage of inelastic product demand; the company has witnessed consistent revenue expansion for the past four decades. Increasing revenues originate from strong customer loyalty from both frequent drinkers and occasional spirit enthusiasts. From an investment perspective, BF.B is a very stable and lucrative investment asset, as its revenues are not negatively affected by detrimental swings in the economic cycle. In actuality, based on sales during prior recessions and downturns revenues remain stable or even increase as liquor provides individuals with a short-term reprieve from present financial difficulties. Whereas many businesses experienced precipitous revenue declines during the Covid pandemic, BF.B's sales remained strong.

Furthermore, BF.B has continually diversified its spirit portfolio over time, the company benefits from very capable executive oversight, instead of being complacent with existing brands BF.B has continued to expand its liquor offerings through enduring product innovation. The company has diversified its product line from 3 original whiskey brands to more than 17 brands. Brown-Forman's product portfolio has continued to adapt and meet the increasing consumer demands for different alcoholic beverages such as tequila, offering brands like El Jimador or Herradura.

From a growth and revenue standpoint, it is reasonable to expect consistent mid to high single digit annual revenue growth going forward which will originate from a number of areas; in past years, BF.B has continued to demonstrate mid single digit net sales growth in its mature American Market from its Jack Daniel whiskey, and the company's Woodford Reserve and Old Forester brands are also strong performers. BF.B also has encouraging growth opportunities in the premium bourbon and tequila segments which grew underlying 2020 net sales by 22% and 13% respectively. Taking a look at income statement related details reveals decades of steady revenue expansion, high margins, as well as a high cash return on invested capital of 15% indicating highly effective executive oversight. Overall BF.B exhibits good performance across the board.

Data by YCharts

Data by YCharts

From a return standpoint, BF.B's stock elicits significant investment appeal; the company has witnessed strong year over year capital appreciation and a track record of increasing dividends. BF.B has increased its dividend yield for 32 consecutive years, demonstrating an unrelenting commitment to shareholder returns. Although BF.B offers a conservative yield of only .96%, the dividend has a prolonged track record of expansion and the current payout ratio is very sustainable at 36% leaving plenty of room for expansion in the future. From a capital appreciation standpoint, the stock delivered for investors experiencing capital appreciation of over 370% over the past 10 years. Typically speaking, consumer staple stocks tend to exhibit only incremental capital appreciation; however, BF.B out surpasses many peers and delivers for investors with a secure underlying business coupled with strong capital appreciation.

Source: Google Stock Charts

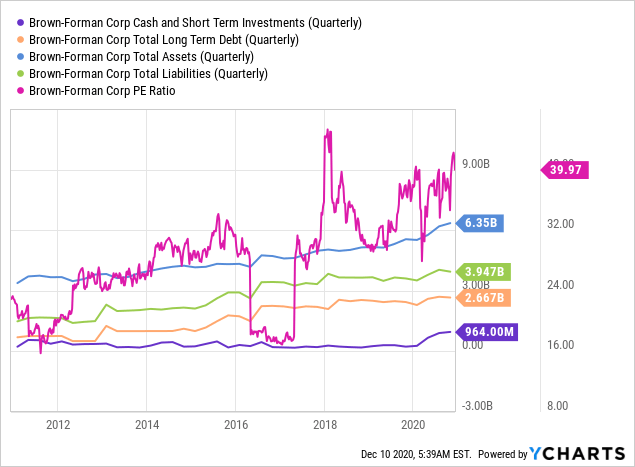

An examination of BF.B's financials reveals a healthy balance sheet; the company has almost a billion in liquidity reserves and a manageable debt load that is well covered by operating cash flow. In terms of valuation, its no surprise BF.B has always traded at a hefty premium. At todays levels, the stock is unquestionably expensive by any means of analysis whether it be P/E, price to book, or discounted cash flow analysis. The stock is trading at a P/E ratio of 39x earnings which is an astronomical valuation for a company delivering mid single digit revenue growth. A reasonable buying price point would be somewhere in the P/E range of 25-30x earnings, if you examine historical valuation data over the past 20 years the stock price has oscillated within that range fairly consistently rendering a buy target of around $50-$55 that would, in my opinion be fair price point for the stock, taking into consideration BF.B's trading premium. Based on a discounted cash flow analysis, the stock is overvalued by roughly 60% as the current share price of $76.75 far exceeds the future cash flow value of $47.81.

Data by YCharts

Data by YCharts

Final Determinations

Brown-Forman operates a phenomenal business, with healthy financials, strong competitive advantages, and a stable long-term outlook. The company's high margins, economic durability, and unrivaled brand equity demonstrate a capable and highly lucrative investment. BF.B remains a fantastic Blue-Chip Stock, However, at this point in time the stock is too expensive; the margin of safety as it relates to valuation is unfavorable. I don't see the share price having significant upward mobility at these levels, but am always keeping an eye on the stock to buy more at a favorable valuation. The short-term trajectory of the share price is not very favorable but for the buy and hold long-term investor the prospects remain strong, especially if you continue to accumulate shares at a more moderate price point.