As the economy reopens and pent-up demand is unleashed, cyclical sectors like hotels, airlines and cruise liners have enormous potential to recover from the COVID-crash. Norwegian Cruise Line Holdings (NYSE:NCLH) is a top turnaround investment that could potentially see its stock price double as cruise liners resume operations.

The tech sector outperformed last year and was a driver of S&P 500's strong resurgence. What sector will be the next one to produce market-leading returns? I think the time has come to look at the worst performing sector from last year: Cruise liners.

I am especially hopeful about Norwegian Cruise Line Holdings whose price has quadrupled from last year's lows. Yet, the cruise line operator remains unloved and has massive rebound potential when the economy opens up and global cruises resume. I will make the case for Norwegian Cruise Line Holdings in this article, but the general argument of this article applies to all the other cruise liners as well.

Pandemic background, suspension of voyages and crisis countermeasures

Almost no other sector, maybe with the exception of airlines, has been as hard-hit by the pandemic as cruise liners, and the argument can be made that airlines have fared much better relative to cruise ships because they are already operating again.

The COVID-19 pandemic brought a complete stop to Norwegian Cruise Line Holdings' operations in 2020, an unprecedented event in the cruise line industry. Norwegian Cruise Line Holdings just last month said that all voyages through May 31, 2021 will be suspended as well.

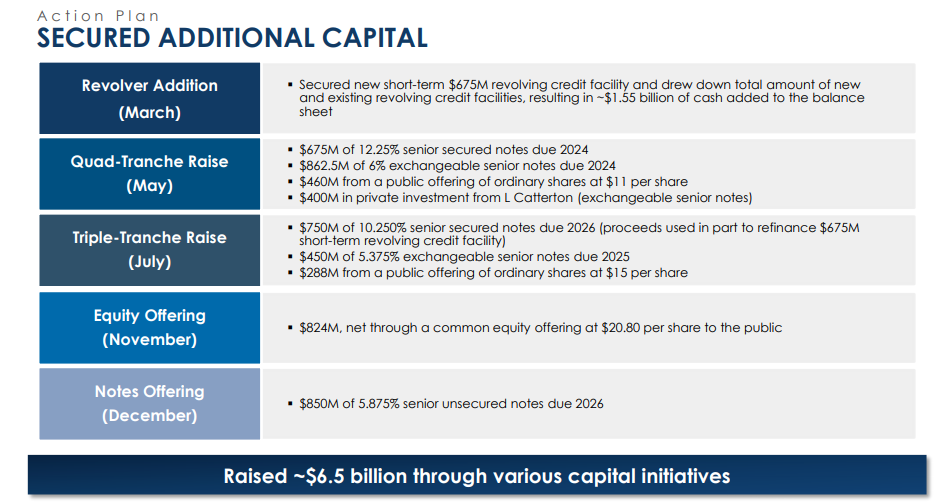

With costs continuing to run and revenues dropping nightmarishly in 2020, Norwegian Cruise Line Holdings turned to external capital, mostly debt, but it was also able to issue equity, thanks to a recovering share price. Norwegian Cruise Line Holdings raised $824 million by selling 40 million shares in November 2020 and $850M by selling 5.875% senior unsecured notes due 2026, the two most recent capital measures. The capital raised should secure the survival of the company at least until 2023. Norwegian Cruise Line Holdings' ability to raise equity and debt during this devastating shutdown is a very positive sign showing that debt and equity holders believe that challenges are only temporary in nature.

(Source: FY2020 Investor Presentation)

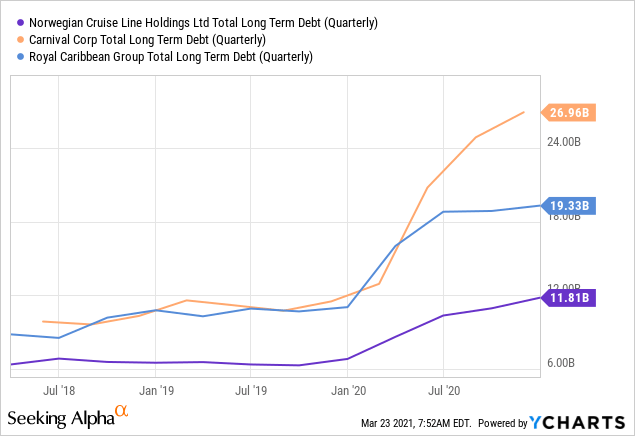

Norwegian Cruise Line Holdings isn't the only company raising debt in light of an industry-shattering pandemic … total debt of the three largest cruise line operators increased exponentially in 2020.

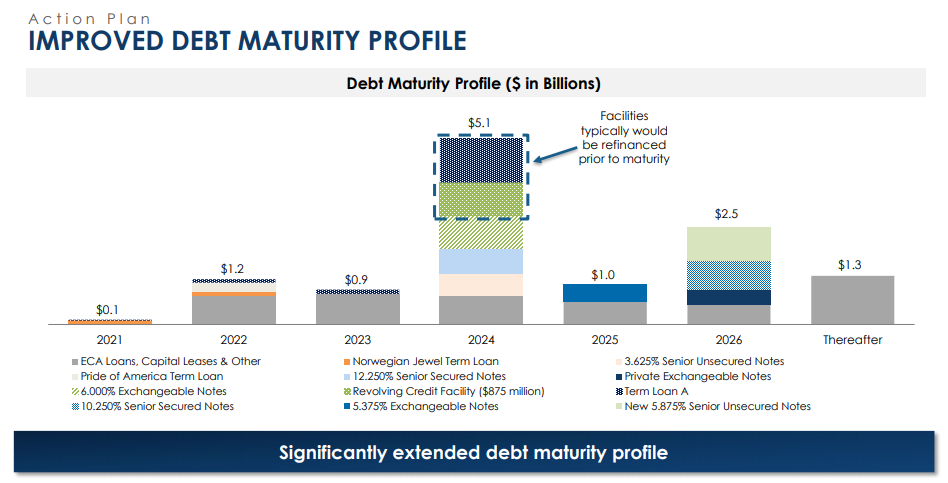

Despite a big increase in debt, Norwegian Cruise Line Holdings has the least amount of total debt outstanding compared to its two rivals, Carnival Corporation (CCL) and Royal Caribbean Group (RCL). Though its debt has increased the least in absolute terms, Norwegian Cruise Line Holdings is on the hook for a substantial amount of debt nonetheless, about $12 billion. Although the company managed to extend its debt maturities, the outstanding debt is massive and poses a risk factor that you as a potential investor should be aware about.

(Source: FY2020 Investor Presentation)

In total, Norwegian Cruise Line Holdings' debt has increased to $12.1 billion based on the largest full year report, about double what it had been before the crisis. Leverage ratios for all cruise liners are larger than they have been historically and NCLH has the highest leverage ratio of the three operators.

NCLH | RCL | CCL | |

Long-term debt bn | $12.1 | $20.1 | $28.4 |

Market cap bn | $10.9 | $22.7 | $30.8 |

Debt-equity-ratio | 2.7x | 2.2x | 1.3x |

(Source: Author)

Ballooning debt and collapsing revenues are rarely good reasons to buy into a business ... except in case of a pandemic-induced demand shock that has nothing to do with the actual validity and performance of the business under normal conditions.

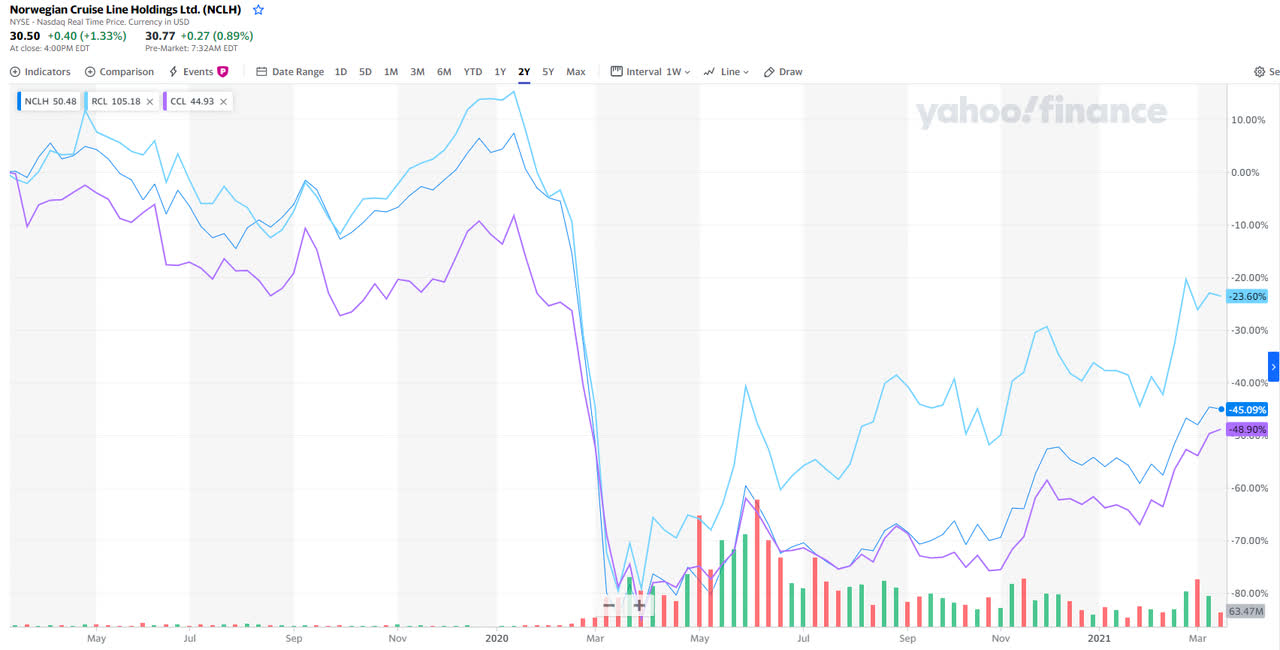

As soon as the economy reopens, no-sail orders are lifted, and voyages resume, Norwegian Cruise Line Holdings could soar, as could the share prices of the other two cruise liners. As of right now, Norwegian Cruise Line Holdings share price is still down by half compared to its pre-COVID-19 valuation, and it could easily double once the business operates normally again.

(Source: Yahoo)

Unprecedented revenue drop

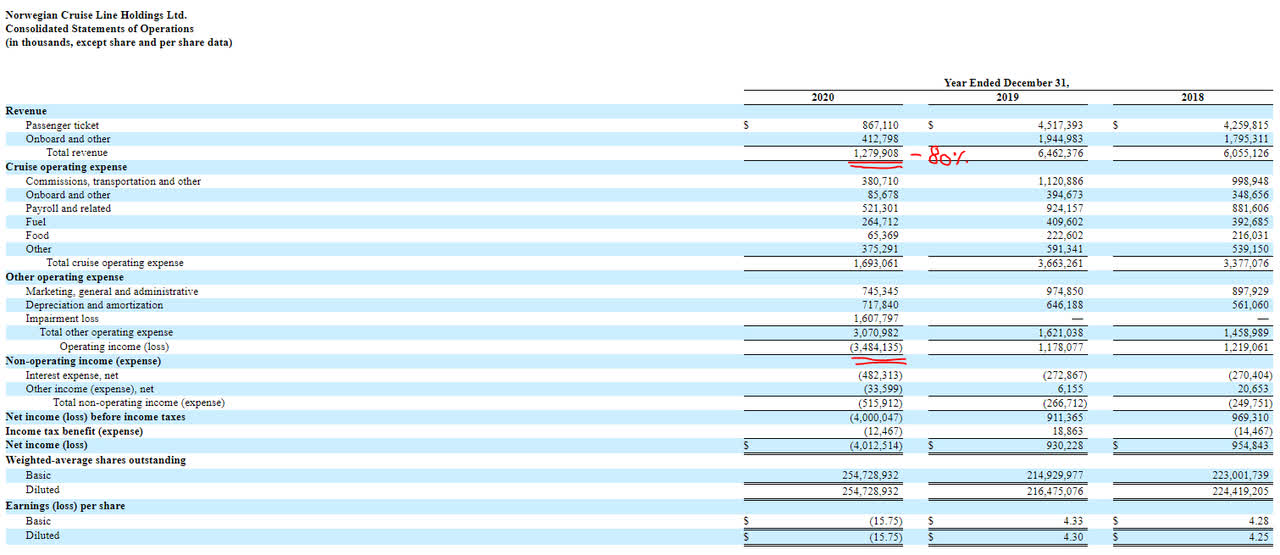

Looking at Norwegian Cruise Line Holdings' financials, you shouldn't be surprised to learn that they are just terrible: FY2020 revenues crashed 80% compared to 2019 and a stomach-turning $3.5bn operating loss remained at the end of the day ... the result of an unprecedented industry shutdown and revenue drop.

(Source: FY2020 Annual Report)

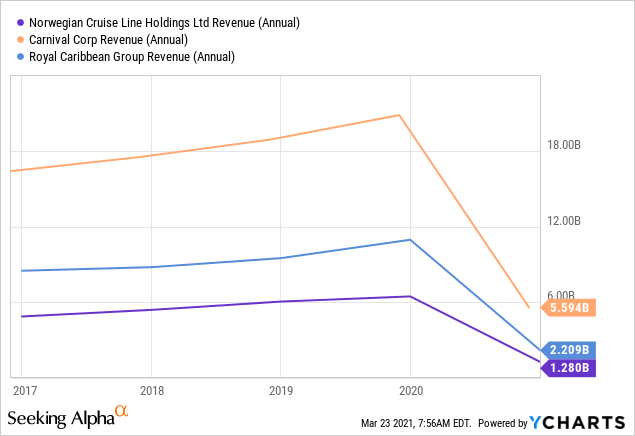

The revenue picture of other cruise liners looks very similar.

But again, once the economy reopens and voyages resume, Norwegian Cruise Line Holdings should see a similarly quick jump in revenues and a turnaround in operating income. Which brings us to the next question ...

When will voyages resume?

NCLH suspended all cruise voyages on March 13, 2020, in response to COVID-19. Voyages are delayed at least until May 31, 2021 and there could easily be another suspension, so don't just think June 1, 2021 is when the party begins. But whether or not cruises will resume on June 1, 2021 or not, the signs in the economy are unmistakably positive, no matter where you look: More than 100m people in the US have now received the vaccine and several US states have said they are lifting restrictions on businesses to operate normally again as we are moving closer to herd immunity. Herd immunity is a term used by medical professionals and it marks the point at which a population is no longer at risk of an infectious disease.

(Source: DW.de, CDC, Robert Koch Institute)

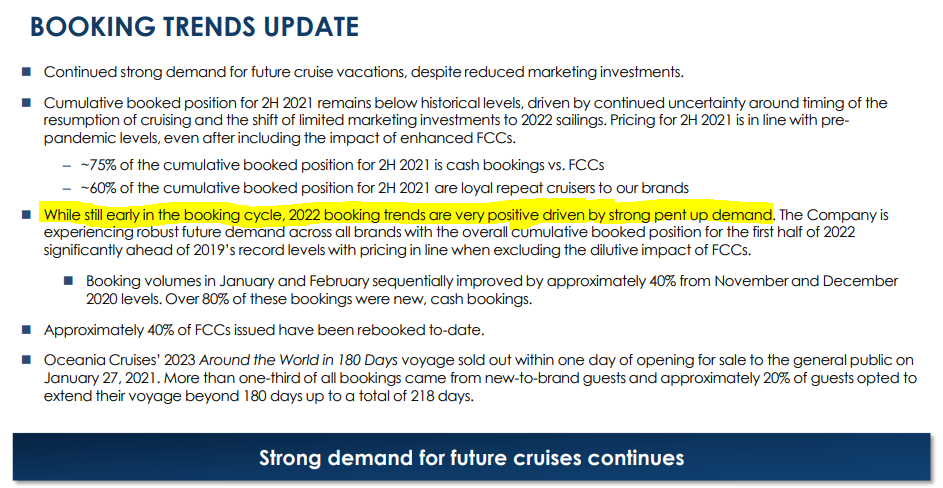

While we do not know the exact date today when global cruises will resume, we already see from booking trends, a forward-looking statistic, that people can't really wait to hop on the next cruise once they are available again. Norwegian Cruise Line Holdings' booking volumes in the first two months of 2021 were up 40% from the November-December period, with the majority being cash bookings. 2023 cruises are already selling out nicely at a time when people are still locked down.

(Source: FY2020 Investor Presentation)

Booking trends also show that customers are not intimidated by fear over COVID-19, which serves to devalue the argument that it will take years for bookings to recover. I think pent-up demand is therefore really underestimated, if not totally ignored, and Norwegian Cruise Line Holdings' depressed valuation is a reflection of this misguided position. As soon as voyages are officially resuming, booking trends indicate that people are going to jump at the opportunity to go on a cruise, and I am positive that this pent-up demand will have a supportive effect on pricing. After being locked down for so long, people are eager to go out and spend money. This isn't to say that everyone wants to go on a cruise, but what matters is that NCLH's core demographic, people aged 50+ with high disposable incomes, is eager to do just that as we have learned from the bookings trend update.

Valuation shows recovery potential

We have seen a repricing of cruise liners last year, but the recovery is far from complete and valuations can grow. To get a shot at securing those recovery gains, however, one needs to invest before the economy reopens and before voyages resume.

Earnings multipliers for cruise liners are very high, but that is because uncertainty about the resumption of voyages depresses earnings estimates.

NCLH | RCL | CCL | Averages | |

Market Cap bn | $10.9 | $22.7 | $30.8 | - |

Market Price | $30.50 | $91.45 | $28.93 | - |

P/E | 47.8x | 53.2x | 112.1x | 71.0x |

Book-share | $2.06 | $2.34 | $1.29 | 1.9x |

Dividend-share | 0 | 0 | 0 | - |

Yield | 0.00% | 0.00% | 0.00% | - |

(Source: Author)

Turning back to Norwegian Cruise Line Holdings, the cruise liner is expected to make another loss this year and earn -$6.07, on average. Estimates range from -$4.8 to -$7.32, but it is quite clear that 2021 is not going to be a great year for NCLH.

Earnings Estimate | Current Qtr. (Mar 2021) | Next Qtr. (Jun 2021) | Current Year (2021) | Next Year (2022) |

No. of Analysts | 9 | 9 | 14 | 14 |

Avg. Estimate | -2.12 | -1.97 | -6.07 | 0.52 |

Low Estimate | -2.32 | -2.28 | -7.32 | -0.62 |

High Estimate | -1.9 | -1.66 | -4.8 | 2.69 |

Year Ago EPS | -0.99 | -2.78 | -8.64 | -6.07 |

(Source: Financial IQ)

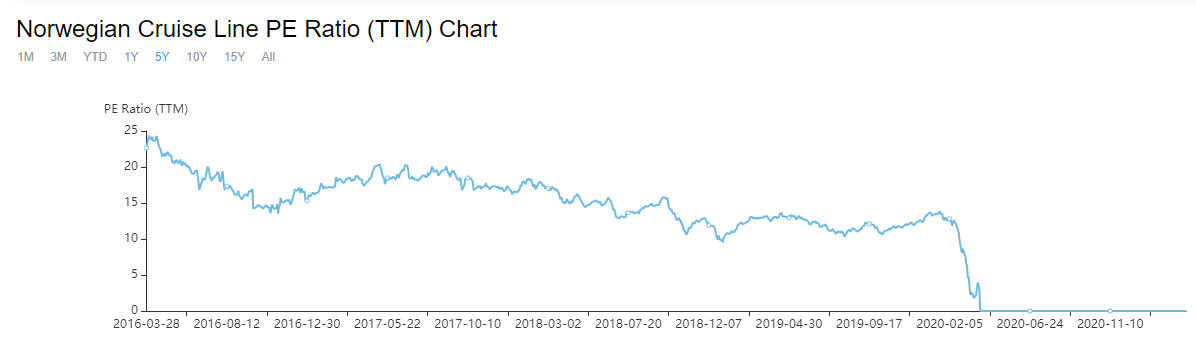

But under normal conditions, Norwegian Cruise Line Holdings should be able to earn $4.20-$4.40 for each share, about the same it earned in 2018 and 2019 when business was operating without interruptions. If we assume that Norwegian Cruise Line Holdings can earn just the same as it did in the past once cruises resume, today's valuation implies a P-E/Ratio of just 6.7x, much less than the historical average of 15-20x.

(Source: Gurufocus)

Business risks and challenges

Norwegian Cruise Line Holdings is subject to a number of risk factors that have a large influence on the cruise liners' ability to sustain its recovery path. I have discussed the two most important ones, exploding debt and customers' willingness to return to cruise ships after a pandemic. A third wave of COVID-19 infections and another government-ordered shutdown would surely delay the return to normal once more. Cruise liners still face a lot of challenges, but once voyages resume, the worst should be behind them.

Closing thoughts

Cruise liners are far from dead, all you need to do is look at booking trends and realize that people are eager to get out after a year of depressing lockdowns. Clearly, 2020 was an exceptionally horrible year for the cruise line industry with an unprecedented revenue drop, and you only need to look at the sector's ballooning debt to see it was an existential crisis.

But, there are reasons to be hopeful. Vaccine rollouts, positive book trends and a political and economic desire to reopen and return to normality should support and lift cruise liners higher, even though it remains uncertain at this point in what month voyages will, in fact, resume. Norwegian Cruise Line Holdings has strung itself along this far and should be able to profit from the factors discussed in this article.