Alteryx (AYX) is one of those tech stocks that did not benefit from the pandemic, as enterprise software spending wasn’t a priority the past year. After several earnings disappointments, AYX now trades at half of the all-time-highs reached in the summer of 2020. The stock appears to offer something rare in the tech sector: growth at a value multiple. The company maintains a solid balance sheet with plenty of cash. I rate shares a buy.

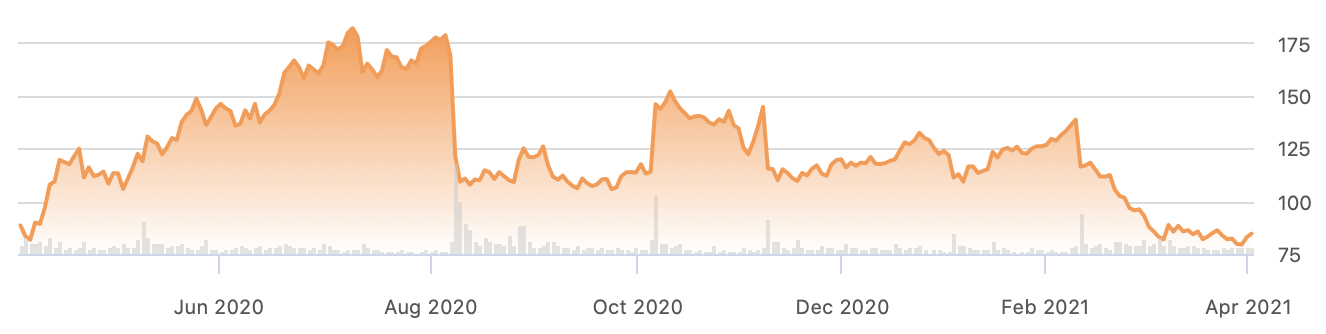

Alteryx Stock Price

AYX came public in 2017 under $16 per share and was a 10-bagger through the summer of 2020 before disappointing earnings sent the stock down about 40% in a single session. The stock rallied back up 25% through February of this year before crashing yet again due to another disappointing earnings report.

The stock has continued tumbling and now trades at 50% of where it did last summer. There clearly was a substantial mismatch between investor expectations and reality. At one point in the summer last year, AYX was trading at over 23x trailing sales, which made some sense in light of 43% first quarter revenue growth but less sense in light of the then-guidance for 10% to 15% second quarter growth. The fall of AYX’s stock price shows the danger of investing without paying enough attention to valuation.

Alteryx Stock Earnings

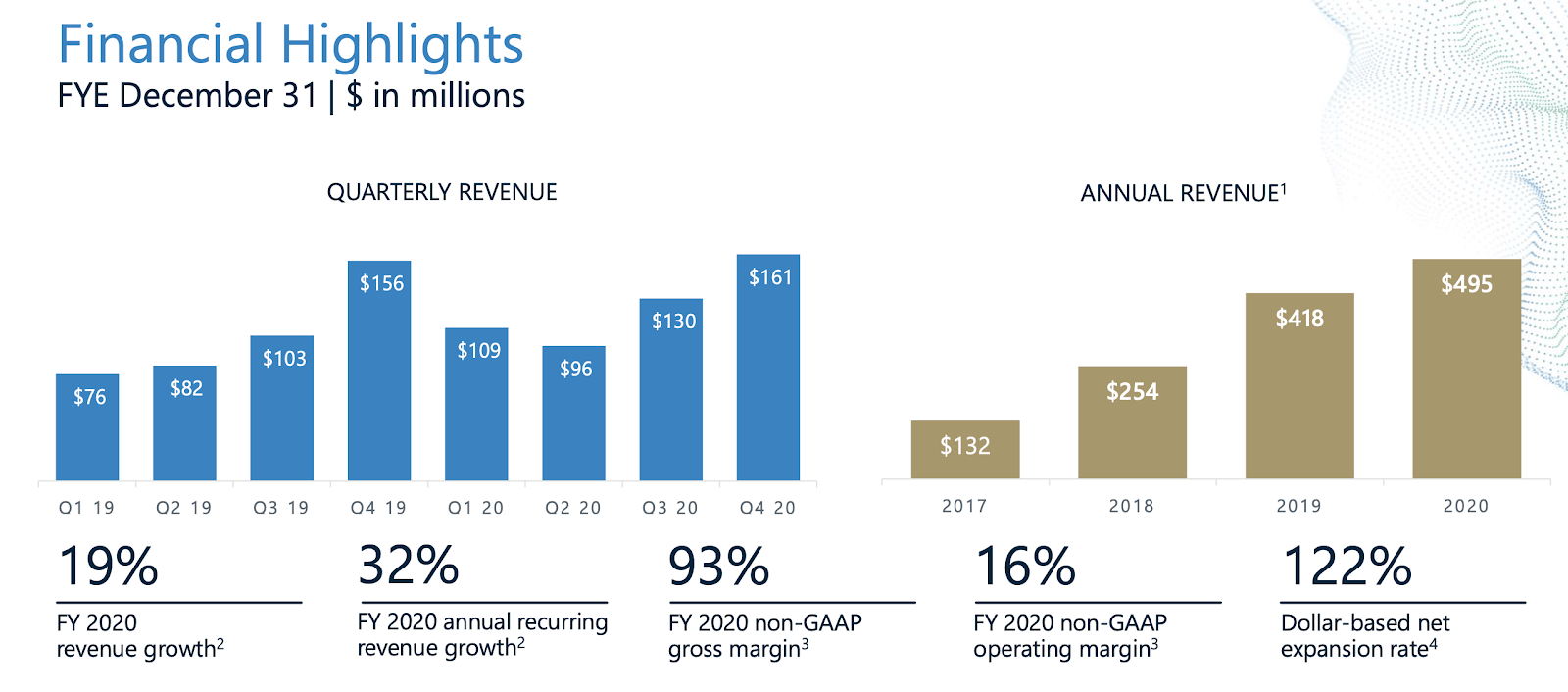

In the most recent quarter, AYX reported minimal revenue growth of 2.6% in the quarter and 19% for the year.

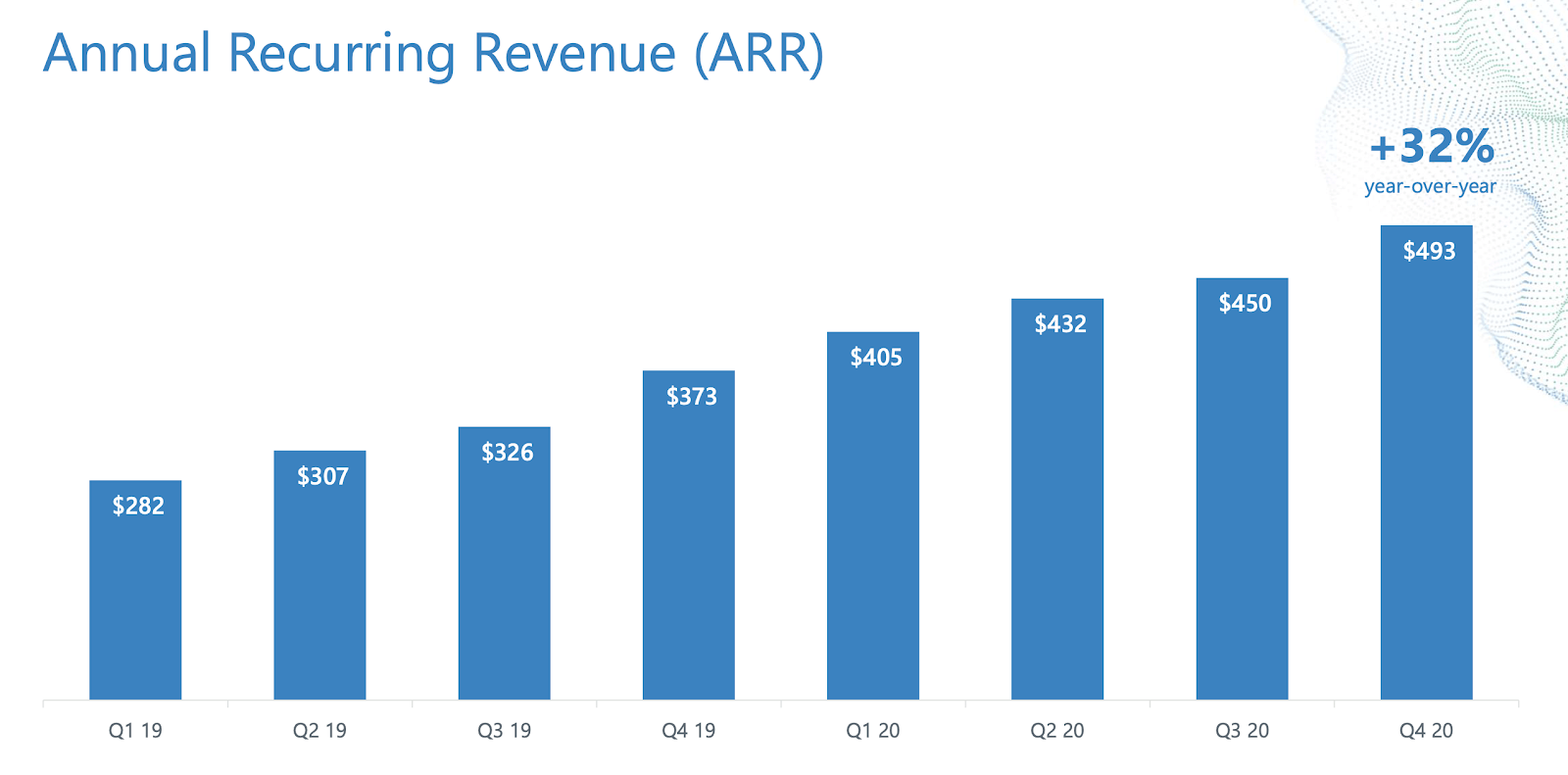

On the earnings call, management blamed the poor growth in part due to “continued effects of COVID and customer buying trends.” However, in my view much of the stock price reaction might be also due to misunderstanding of how AYX reports revenues. Investors might be better served by focusing on annual recurring revenue (‘ARR’) to gauge AYX’s business trends. ARR grew 32% YOY in the fourth quarter - a stark contrast to the aforementioned 2.6% growth in revenues.

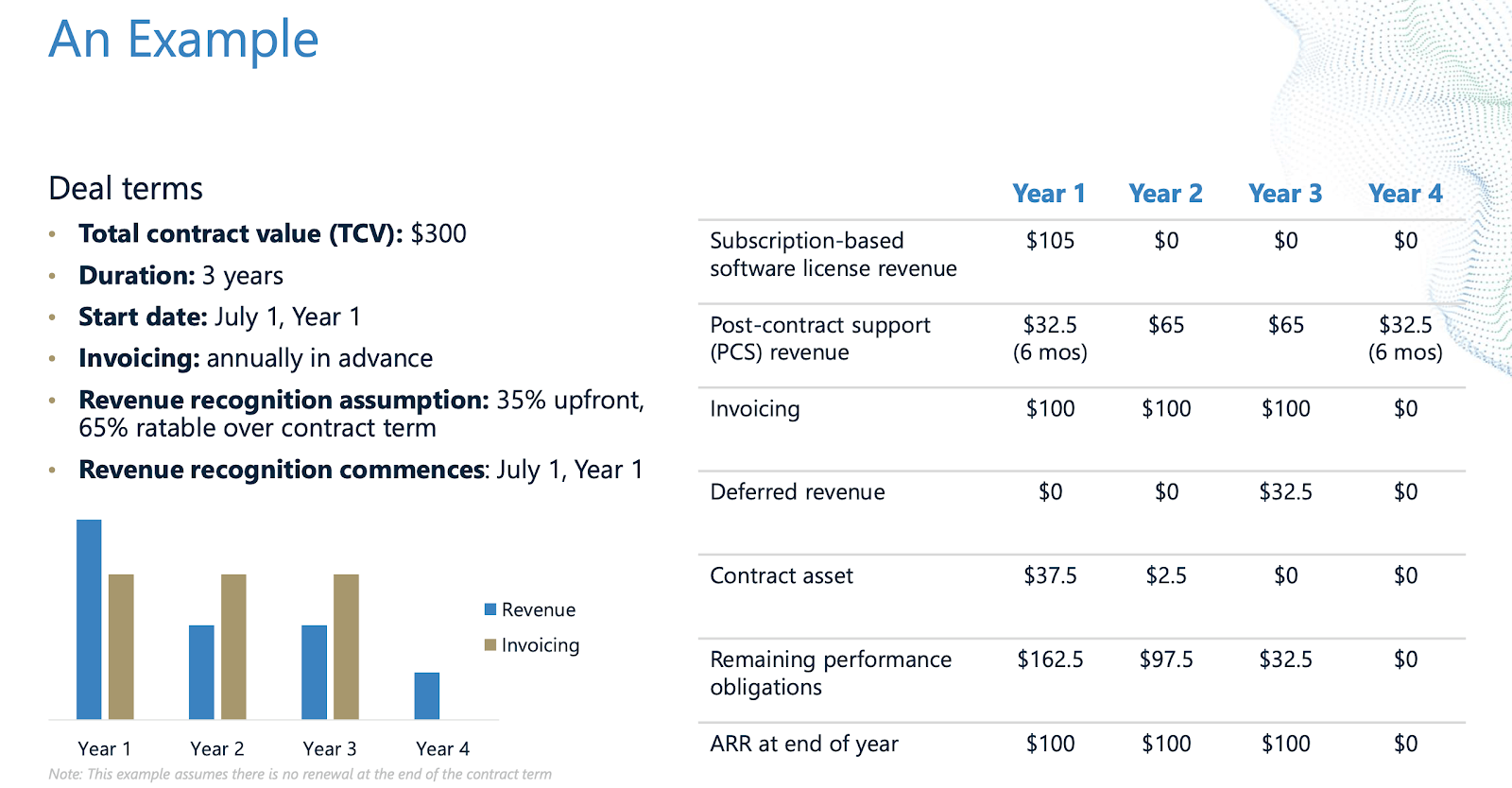

What’s the difference between ARR and revenue? We can see an example below.

AYX currently reports revenue by breaking out “subscription-based software license revenue” and “post-contract support” revenue, both of which can be seen in its GAAP income statement. The problem is that this makes it appear that revenue is declining after the first year. ARR, on the other hand, equally distributes the total contract value across the duration of the contract, which is arguably a better representation of business trends.

Is Alteryx A Buy Or Sell

So now the question is whether AYX, now trading at 12x trailing sales (price to ARR is roughly equivalent) is finally a buy? On a valuation basis, I am inclined to lean on the bullish side as price to trailing sales is less than half of the projected 26.8% ARR growth rate. Valuation isn’t everything - one must also make themselves comfortable with the AYX growth story.

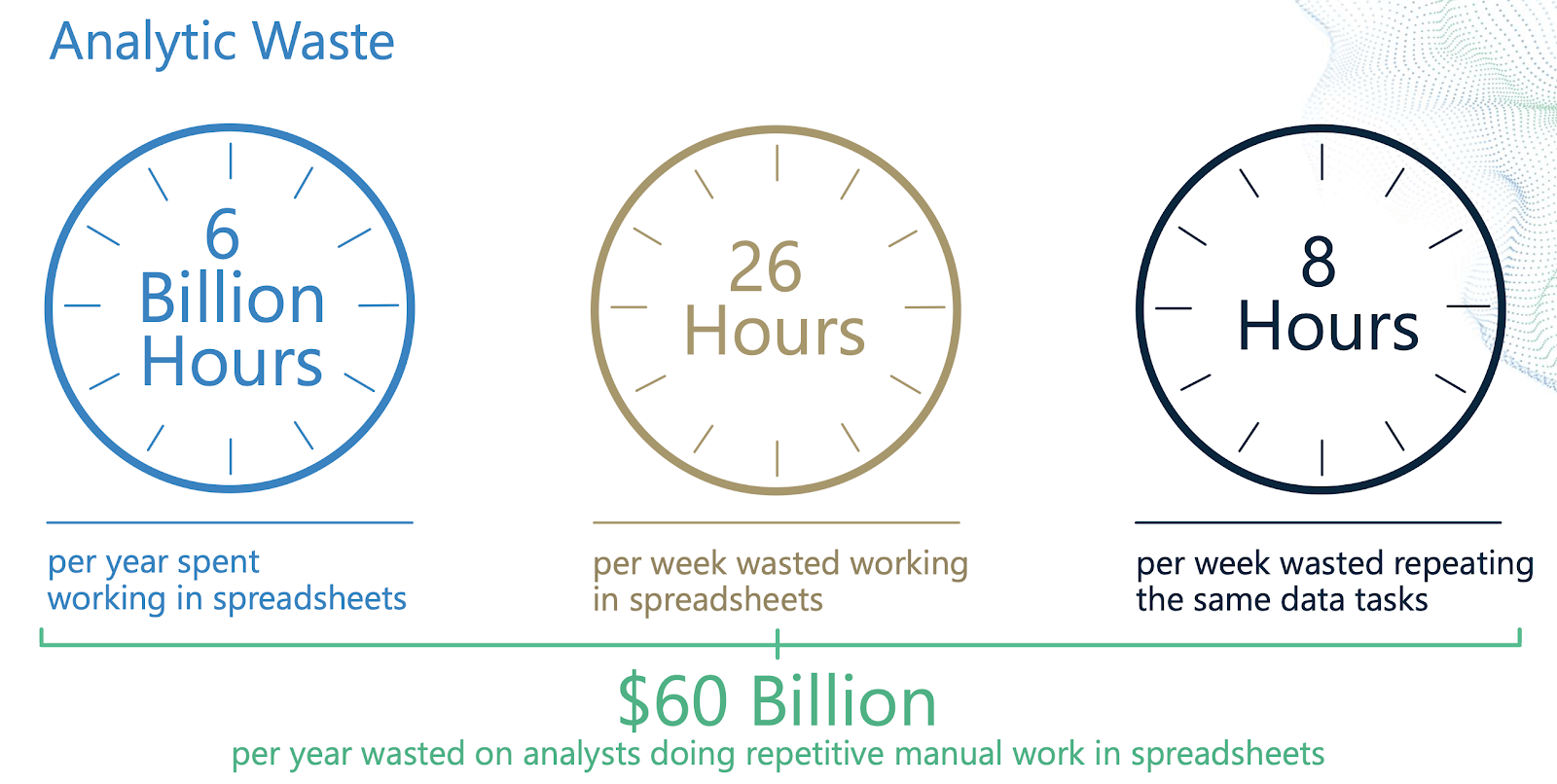

In a world of ever-growing data, old forms of data analytics lead to substantial wasted time: if you’re using spreadsheets, then you won’t be able to avoid repetitive manual work that wastes time.

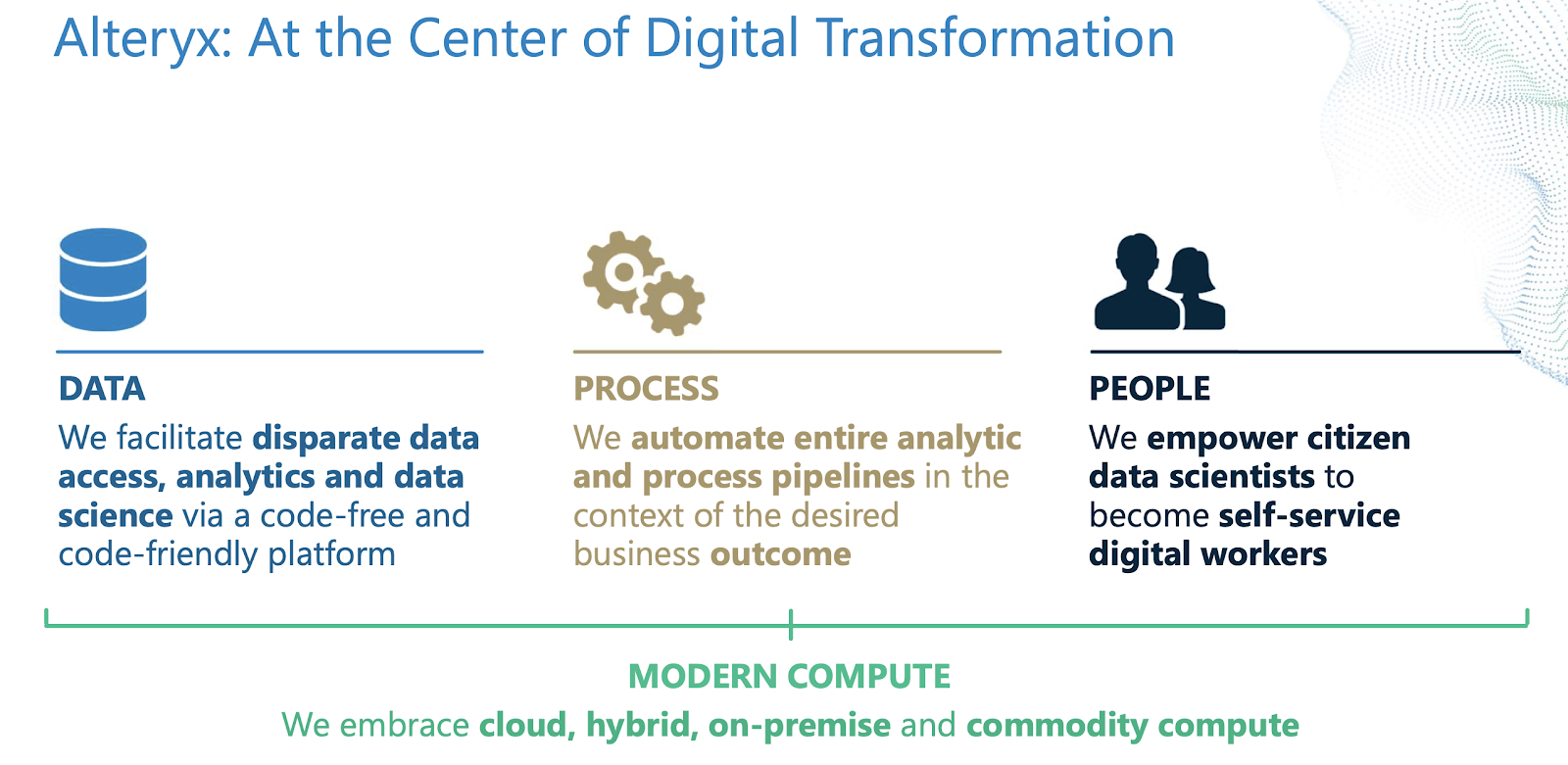

AYX’s product offers a code-free way to analyze and process data.

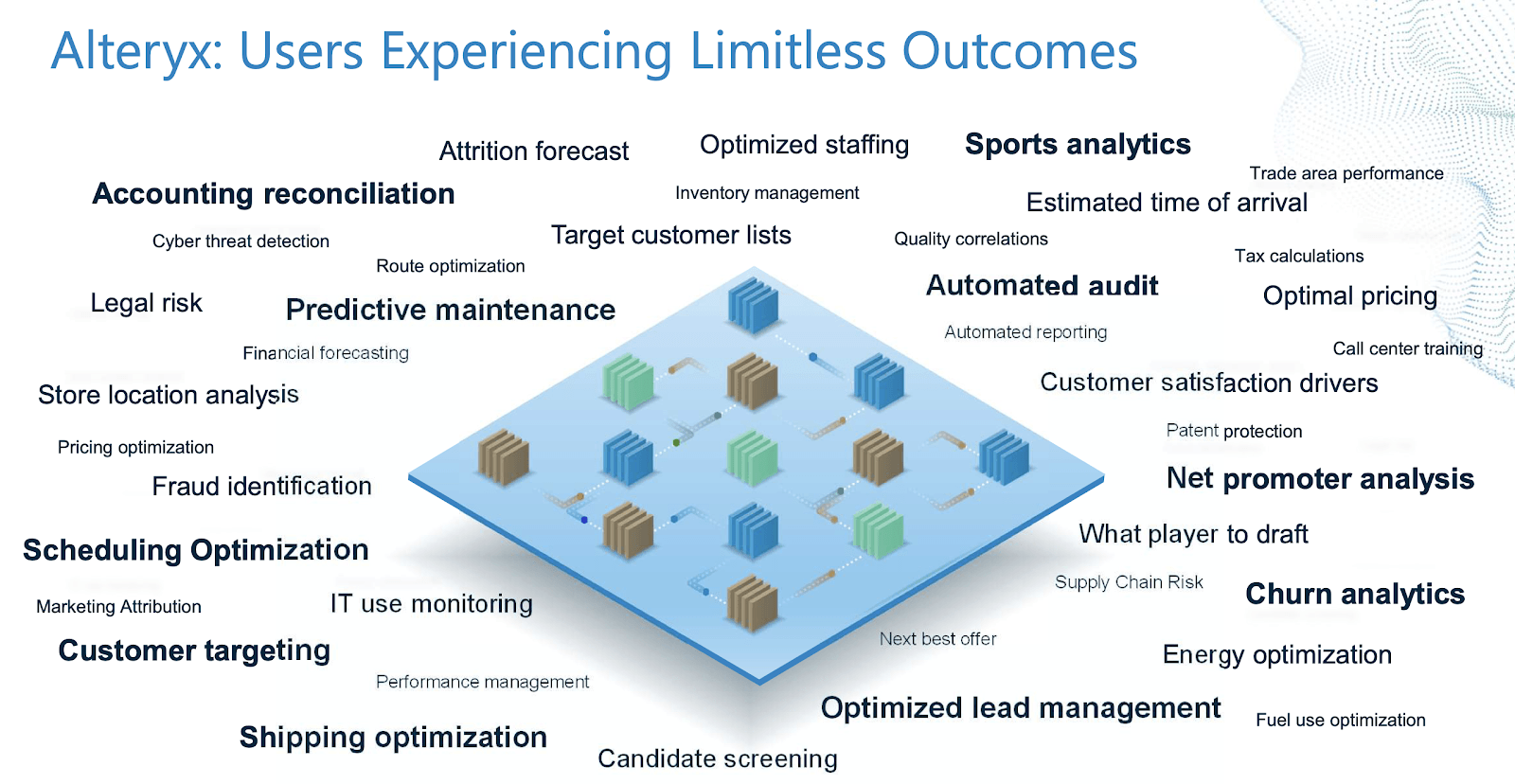

Data is everywhere and thus there are limitless use cases for AYX’s products, ranging from churn analytics to even sports analytics.

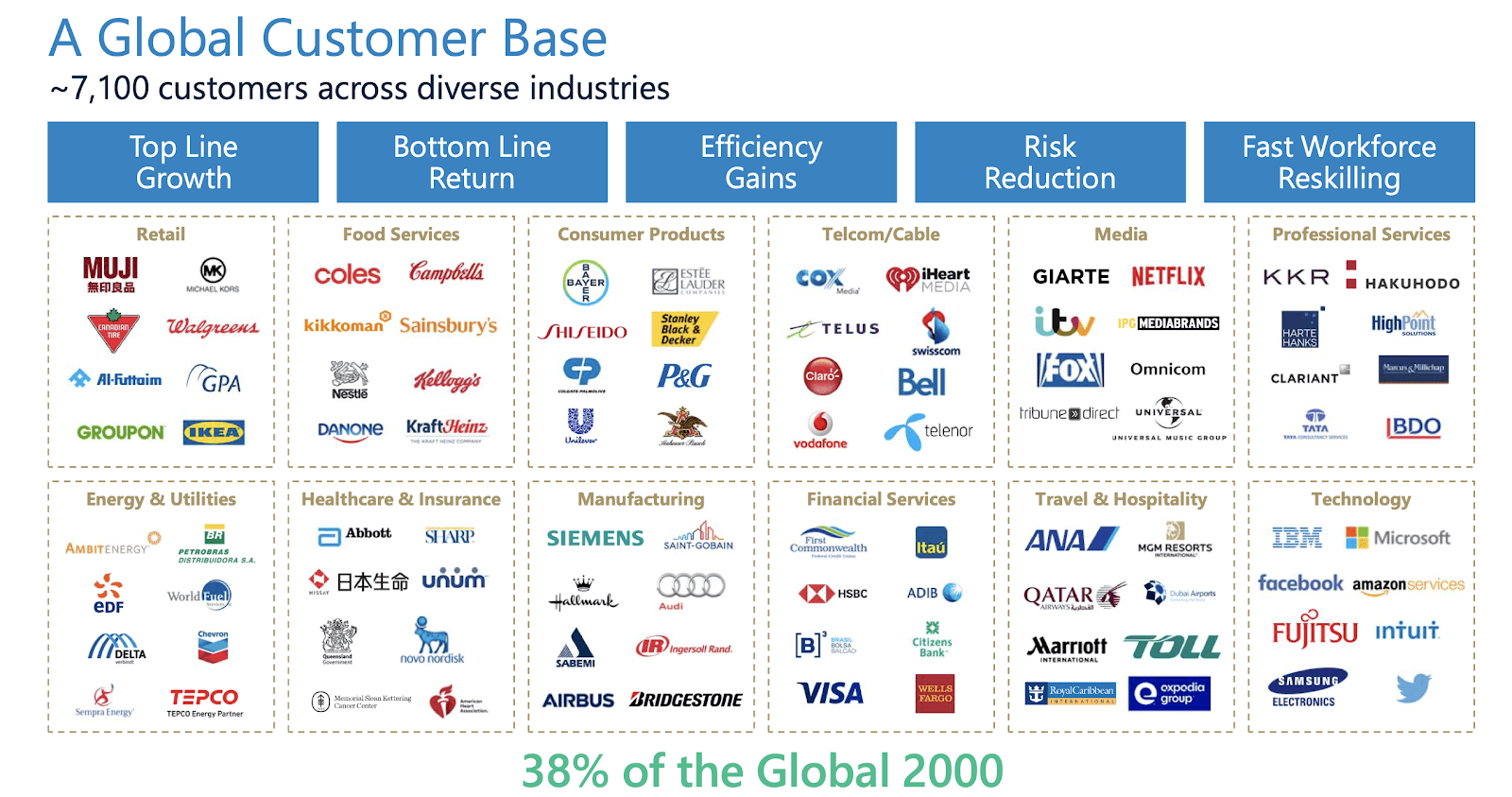

AYX has become a household name in the data analytics space as its customers include 38% of the Global 2000.

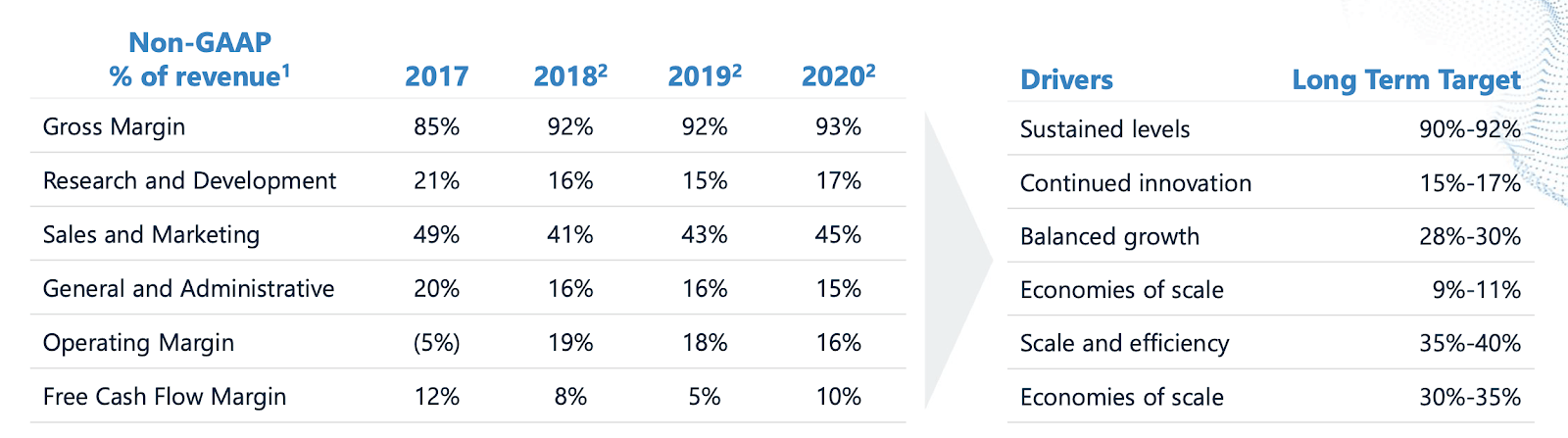

I see data analytics as being one with secular tailwinds for at least the next decade if not several decades. As a result, I am comfortable valuing AYX based on price to sales instead of price to earnings, as AYX is targeting 30+% long term free cash flow margins.

If we assume that AYX might trade at 30x earnings upon reaching such margins, then that equates to a price to sales multiple of 9x. With shares trading at 12x trailing sales, the stock is barely pricing in 1 year of growth. In other words - investors can buy AYX and get the growth for free, as the stock may be able to crush the market even without multiple expansion. My 12-month price target is $133, representing 15x forward sales (reflecting some multiple expansion from the current 12x sales multiple). Shares have 56% upside to that target.

Balance Sheet Analysis

AYX maintains a strong balance sheet with $755 million of cash versus $730 million in convertible notes. We can see below that the convertible notes carry minimal interest expense, but the 2023 notes are already “in the money” with an initial conversion price of $44.33 per share.

I do not see any financial risk from these convertible notes as they could be redeemed with shares. The 2023 notes would add 10.2 million to the diluted share count, which I have included in my valuation estimate above. AYX generated $75 million in cash from operations last year, leading me to conclude that the current cash position is more than enough to weather future storms.

Risks

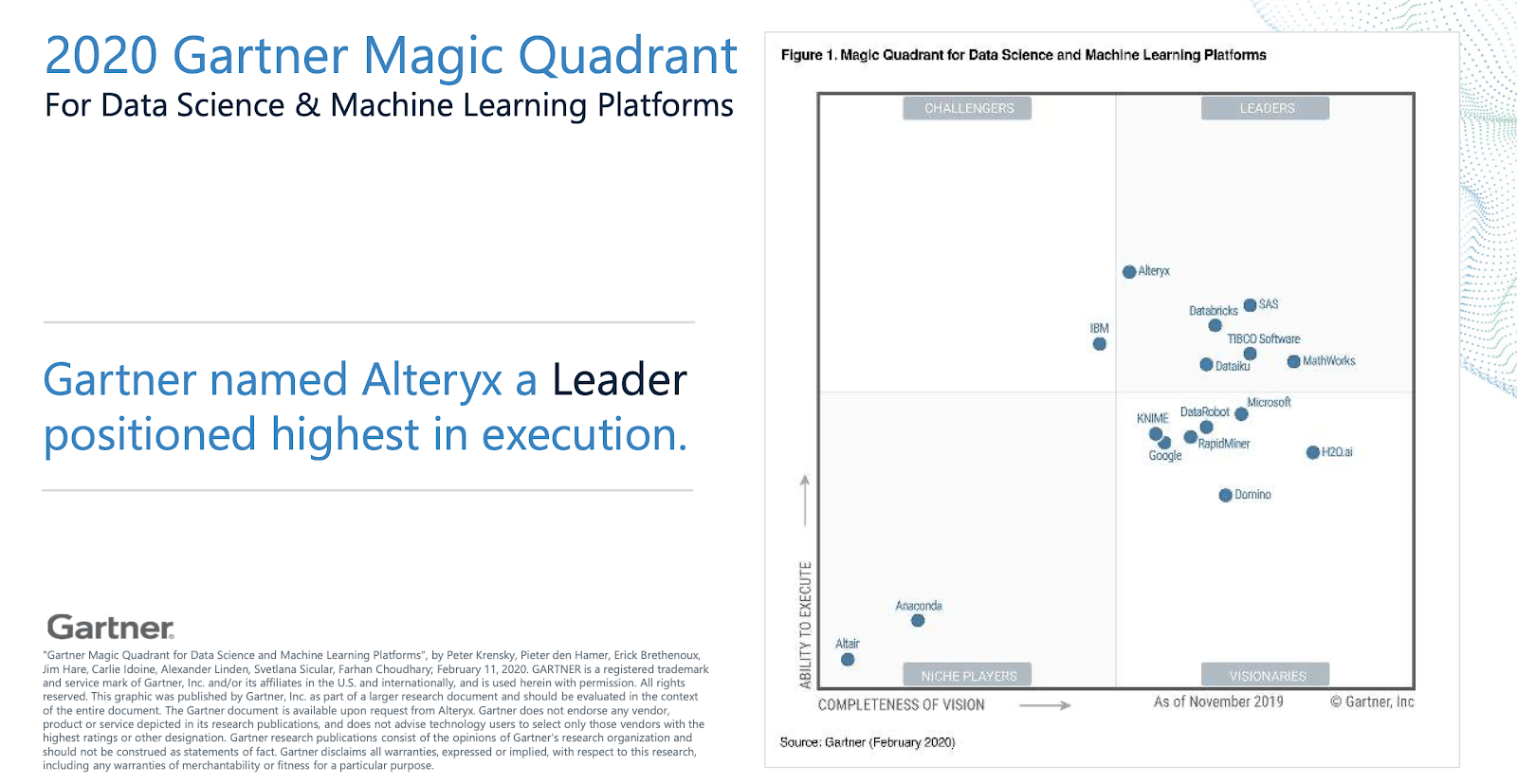

There are two main risks I see with AYX. The first is that it is not obviously the top player in its sector. Gartner rates AYX as having the highest in execution, but there are many competitors ranked better as “visionaries.”

It is difficult for generalist investors like myself to concrete evaluate which tech product is the best or positioned to succeed in the market. If AYX’s product ends up being overtaken by competitors, then forward growth rates will be negatively impacted and AYX may not be able to achieve its target of 30% free cash flow margins. While I am unconcerned by the decelerating revenue growth rate because of robust ARR growth, I would be highly concerned if ARR growth declines moving forward.

Conclusion

It may be scary to buy into AYX stock considering it is 50% lower than all time highs, but the selloff appears valuation-driven as opposed to fundamental deterioration. After the selloff, AYX appears undervalued in light of projected ARR growth. AYX has a clean balance sheet without any long term debt except convertible notes, and shares may deliver multiple expansion alongside growth. I rate shares a buy with 56% upside to my 12-month target.

The High Conviction List

AYX features rapid growth at a reasonable price. Want more stocks like AYX?

At Best of Breed, my portfolio includes over 25 stocks projected to crush the market over the next decade.

Get access to my highest conviction ideas. There's a 2-week free trial available.

Start Your 2-Week Free Trial