Summary

The bidding war for Coherent (NYSE:COHR) is over, and II-VI (IIVI) won the battle. But what did Coherent get? And why did Lumentum (LITE) and MKS Instrument (MKSI) even bid on Coherent?

The laser market is competitive but also rewarding. Laser technology is used in various fields ranging from manufacturing displays to quality control measures.

With Coherent's acquisition, II-VI becomes one of the largest pure-play laser companies. Coherent's product portfolio complements II-VI's in industries as electrical vehicle manufacturing and battery welding, laser additive manufacturing, and aerospace and defense photonics.

Furthermore, II-VI gets access to Coherent's display manufacturing capabilities and globally distributed sales and service force.

I'm bullish on Coherent's stock because of the growing nature of the laser industry. Still, I project dampened growth for the near term due to the price they paid for Coherent and the required restructuring efforts to generate the synergies.

The laser market

In the upper part of the picture below are the charts for II-VI, Lumentum, Coherent, IPG Photonics Corporation (IPGP), MKS Instruments, and Novanta Inc. (NOVT).

The three graphs below the price are the correlation of Lumentum, IPG Photonics, and Novanta against II-VI. Over a time frame of 6 years, the stock prices and the expectations towards these companies highly correlate. They are in the same industry, so this behavior is expected.

Source: Tradingview

On average, these companies' share prices experienced a CAGR of 25% over the last six years. Let's look at their revenue over a 10-year period.

Source: Companies Annual Reports

Source: Companies Annual Reports

There are spikes in revenue that can be explained by acquisitions these companies have done in the past.

| Company | Acquisition | Date | Price paid | Top-Line Growth |

| MKSI | Newport | 2016 | $905mn | $603mn |

| COHR | Rofin | 2016 | $904mn | $520mn |

| LITE | Oclaro | 2018 | $1.8bn | $500mn |

| II-VI | Finisar | 2019 | $2.9bn | $938mn |

| II-VI (NEW) | Coherent | 2021 | $6.3bn | $1.2bn |

Now the important questions, did the synergies from those acquisitions contribute to larger growth or better margins than those of their competitors?

We will look at the companies' EBITDA and operating margins to answer our question.

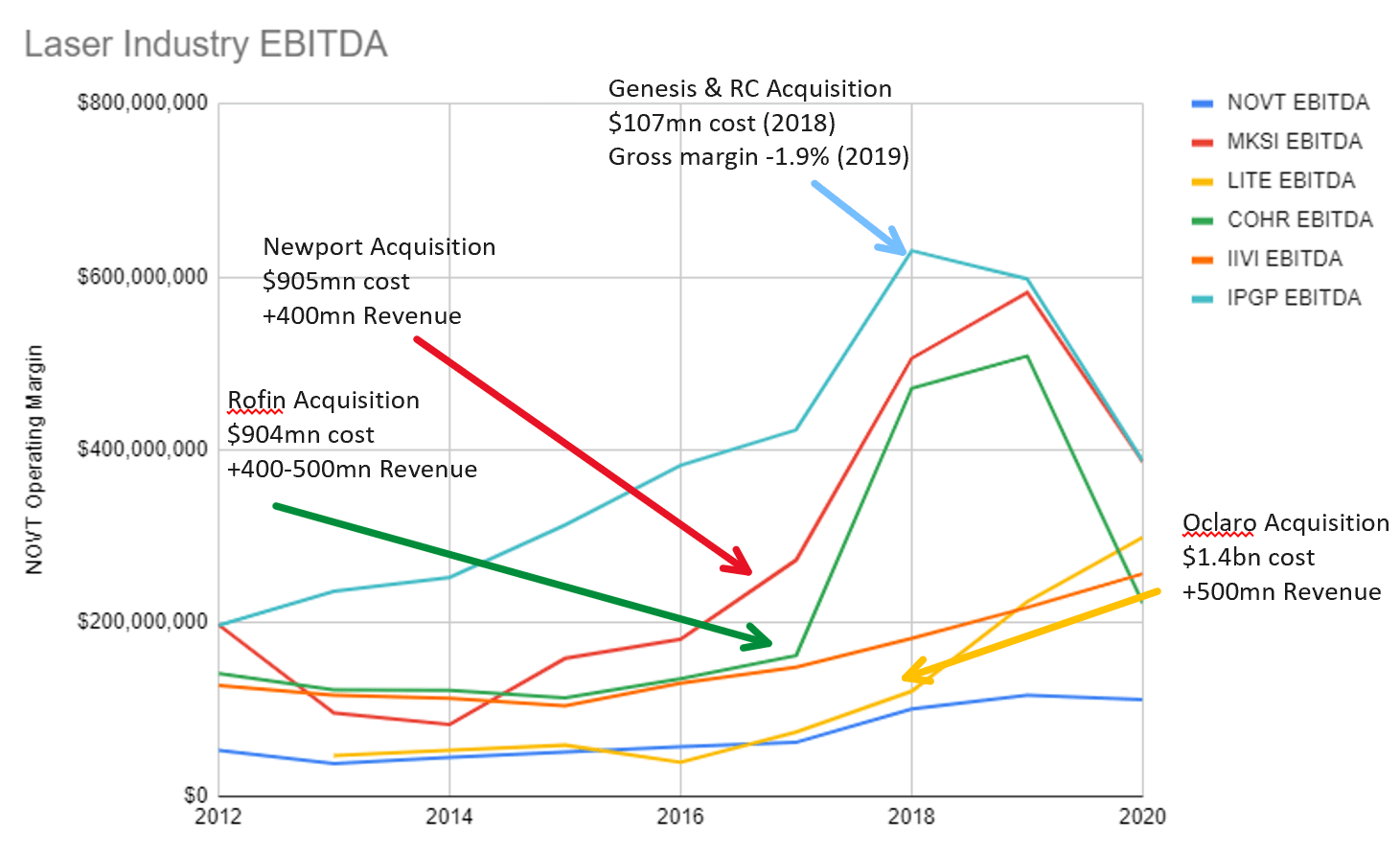

In the graph below, I added the acquisitions at the dates they were done.

Source: Companies Annual Reports

All companies experienced top-line growth until 2020. MKSI was able to maintain and even increase its growth after the acquisition in 2017. Coherent's growth fell back to pre-acquisitions levels in 2018/19. Lumentum was able to maintain high operating income growth after the acquisition. Even better, Lumentum was able to bring its operating margins up to industry standards of 20%.

Source: Companies Annual Reports

MKS Instruments made a few acquisitions in the past, and their operating margins are floating around the 20% threshold. Coherent and IIVI behave similarly over the 10-year horizon.

There is some cyclicality in this industry. Revenue and margins were flat or decreased between 2012 and 2016 and increased throughout the industry between 2016 and 2018/19.

The acquisitions added to top-line growth, and Lumentum could translate the acquisition into sustainable margin expansion even through 2020, which is remarkable. II-VI was able to keep margins flat throughout 2020

Final Thoughts

Acquisitions in the laser industry occur frequently. Judging from the resulting margins after those acquisitions, it seems that economies of scale play a role in improving profitability.

Lumentum acquired Oclaro in 2018 for $1.8bn, which was 3.5x sales at the time. Lumentum was able to profit from the synergies. MKSI and Coherent were somewhat successful with their acquisitions.

II-VI paid 3x sales for Finisar in 2019, and now they paid 5.25x sales for Coherent. Those two acquisitions make II-VI the largest pure-play laser manufacturer by market capitalization and revenue.

Source: Companies Annual Report

Coherent display manufacturing capabilities are an interesting add-on to II-VI's portfolio, but due to the smartphone market's saturation, I project mediocre growth in this segment.

Coherent has next-gen display technology in their portfolio, like micro-LED displays that will further nurture growth and demand. Micro-LED displays are rumored to be used in Apple's (AAPL) 2023 Apple Watch.

The display market is certainly interesting. Next, generations of smartphones, monitors, tablets, laptops, and TVs will implement newer display technologies. Still, other market players like Samsung (OTCPK:SSNLF) and LG (LPL) will fight vigorously for their market share.

Conclusion

I am bullish on the laser industry in general. Investors can expect returns in the mid-twenties for the upcoming years with the implementation of the 5G network, increasing bandwidth demand, improving display technologies, next-gen wearables, and portables, and the increase in the use of lasers in various other industries.

II-VI has to digest a lot with the acquisition of Finisar in 2019 and now the much larger acquisition of Coherent. Coherent had declining revenues from 2018 until mid-2020, its margins contracted, and operating cash flow decreased.

II-VI is under good management with Vincent Mattera, who leads the company well.

I always welcome constructive criticism and open discussions. Please feel free to comment or PM me about my calculations and/or sources that I use in my articles.