This article was first released to Systematic Income subscribers and free trials on 27-May.

In this article, we discuss the action in PIMCO CEFs over the month of April, in particular the changes in leverage and coverage. April was a very unusual month as taxable fund borrowings surged, driving the average taxable fund leverage to 40% - a high over the past year and very likely the highest average level on record. We also discuss our stance in the suite over the past year which followed a valuation + catalyst approach. We continue to like the recently launched PIMCO Dynamic Income Opportunities Fund (PDO).

Leverage Update

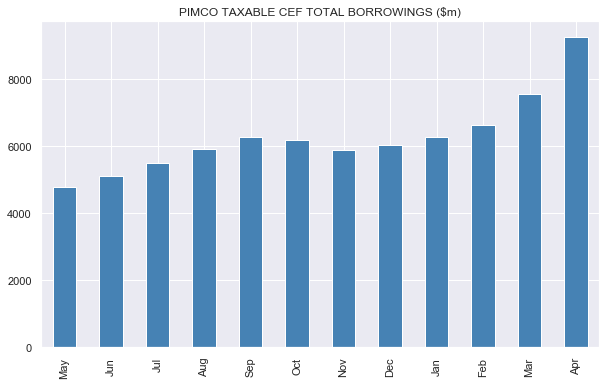

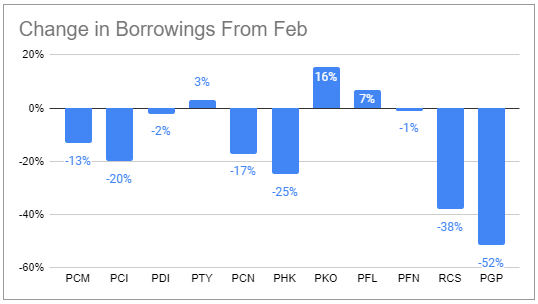

Total taxable CEF borrowings continued to scale up sharply.

Source: Systematic Income, PIMCO

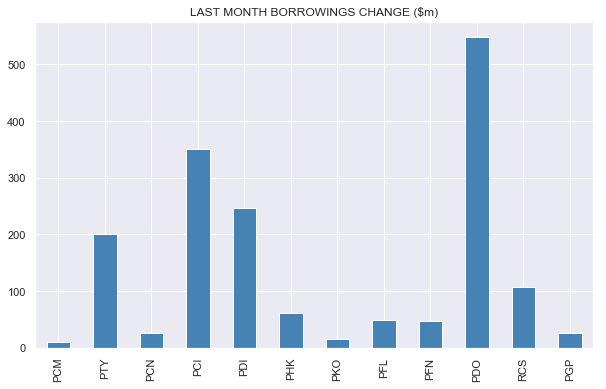

In contrast to the previous month, however, PDO was not responsible for the majority of the increase, though the fund did soak up the biggest share of the borrowings increase.

Source: Systematic Income, PIMCO

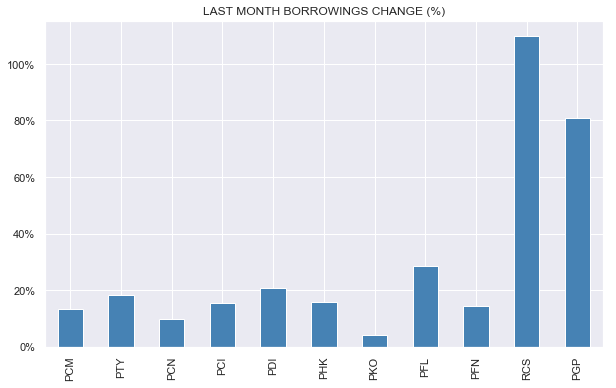

In relative terms we see something interesting - the more idiosyncratic PIMCO Strategic Income Fund (NYSE:RCS) and PIMCO Global StocksPLUS & Income Fund (NYSE:PGP) showed huge increases in borrowings with RCS more than doubling its borrowing levels over the month.

Source: Systematic Income, PIMCO

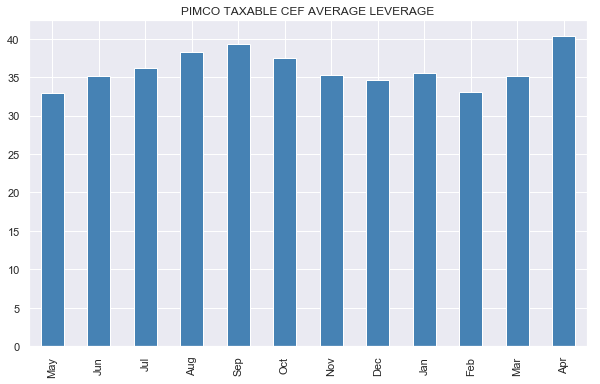

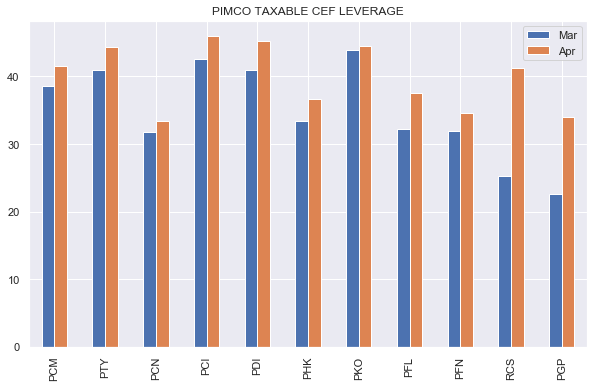

The average leverage of the suite increased from about 35% to 40%. Even if we remove PDO from the sample (which would bias the average leverage of the previous months lower) the numbers are pretty much the same.

Source: Systematic Income, PIMCO

The chart below shows that the increase in borrowings was well in excess of any move in asset prices and led directly to a sharp increase in leverage across the entire suite.

Source: Systematic Income, PIMCO

Just to highlight how unusual this is - first, the size of the average leverage jump was a huge 5% and, secondly, all funds increased leverage whereas typically some funds increase leverage and others cut leverage.

The biggest hikes in leverage were in the more idiosyncratic funds PIMCO Strategic Income Fund and PIMCO Global StocksPLUS & Income Fund which were already running at low "official" leverage. The reason we put official in quotes is to highlight that the disclosed leverage figures for these two funds understates the amount of asset exposure they actually take. For RCS this is because TBA dollar rolls (or exposure via agency MBS derivatives financing) don't make it into the official leverage figures.

And for PGP, the fund gains exposure to stocks not via ETFs or individual stocks (which would show up in official leverage figures) but via total return swaps whose mark-to-market doesn't reflect the actual notional equity exposure (due to it being a swap of cash flows which nets out to a much lower number that is not representative of the company's actual equity exposure).

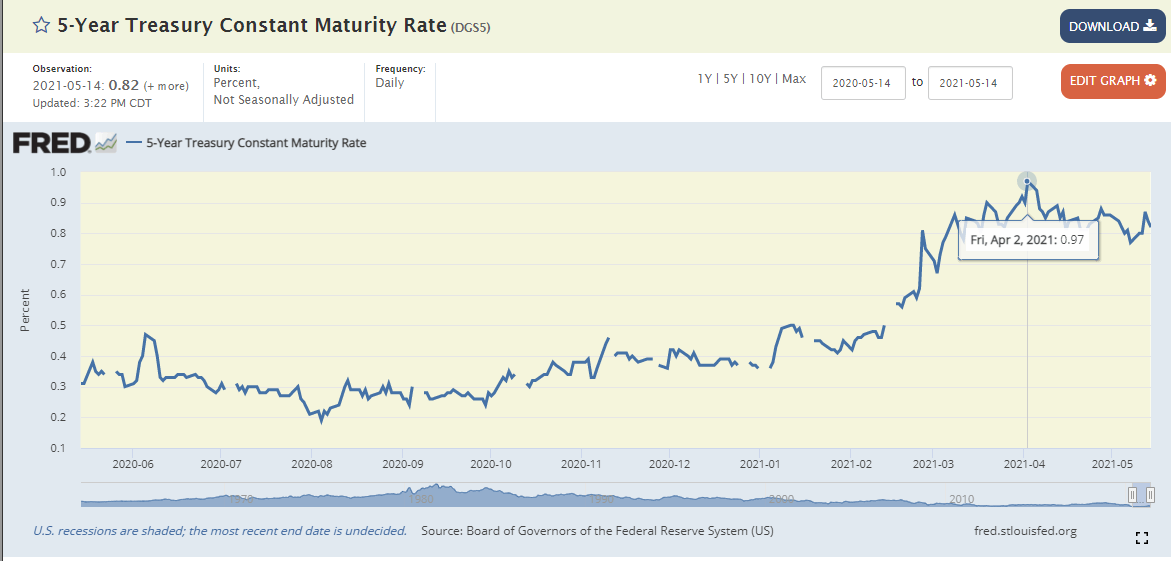

We don't know the nature of the new assets added in April. For RCS we can speculate that they may be in agency specified pools (as additional TBA exposure wouldn't show up in the official leverage figure) since TBA dollar roll financing has grown more expensive as the market has recovered over the last few quarters with the Fed continuing to soak up a lot of the agency demand. This might make sense if fund managers want to 1) take advantage of higher Treasury yields which peaked in early April relative to the past year as we can see in the chart below:

Source: FRED

...and/or 2) want to improve the resilience of the funds by adding high-quality assets that will hold up well in a risk-off market environment and offset a potential drop in credit assets.

This explanation is not entirely satisfying, however, for two reasons. First, agency spreads (over Treasuries) are incredibly tight and so do not present attractive relative value opportunities. And secondly, a risk-off move in markets, in our view, is more likely to come from an inflation surprise or a monetary policy mistake (e.g. taper tantrum 2.0) rather than a traditional cyclical weakness which would actually lead to higher rates, causing agencies to fall rather than rally. This is exactly what we saw a couple of weeks ago as both Treasuries and credit assets sold off.

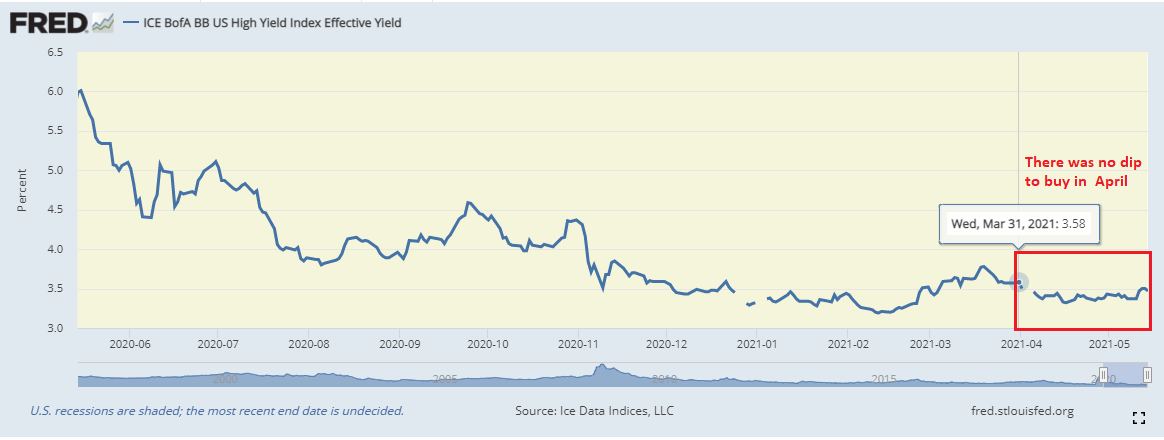

It is also possible that the funds added credit assets; however, credit yields did not present new attractive opportunities through April as we can see below.

Source: FRED

It is possible that PIMCO has found a particularly attractive opportunity which it pounced off and stuffed into all of its funds, particularly funds running at a low leverage level such as RCS and PGP.

Finally, it is also possible that PIMCO funds have begun to be stretched for income and the managers want to boost income levels over the medium term as a way to avoid a potential distribution cut. This also implies that this rise in leverage may be a kind of capitulation by PIMCO away from their trend lower in leverage from September into February which may have been structured to give the fund additional dry powder to add assets. Given that we haven't really had a significant sell-off in credit assets for around a year - the wait might just have been too long to bear.

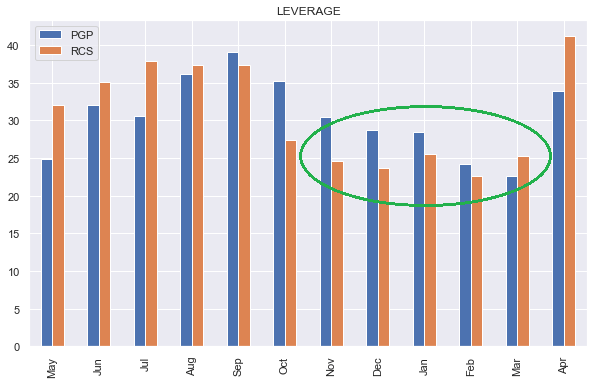

This "capitulation" may explain the strange trend in leverage across PGP and RCS over the past year which deleveraged significantly but have now added back all, or nearly all, of their lost borrowings.

Source: Systematic Income

Coverage Update

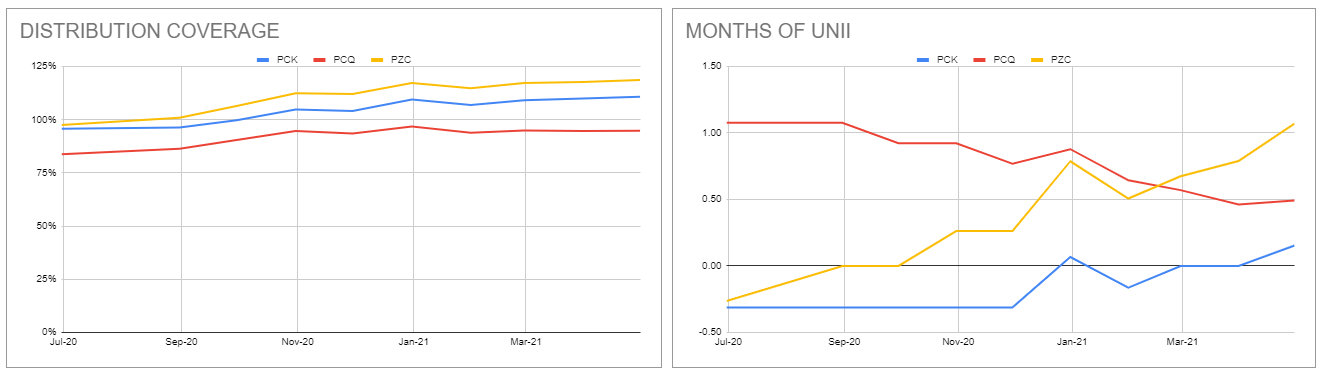

There were few significant moves in 6-month rolling coverage across either the muni or the taxable suites. In the California sub-sector, PIMCO California Municipal Income Fund II (NYSE:PCK) and PIMCO California Municipal Income Fund III (NYSE:PZC) coverage ticked up slightly while PIMCO California Municipal Income Fund (NYSE:PCQ) was flat. PCQ has been underperforming the other two funds in both coverage and UNII trends due to its unsustainably high distribution rate on NAV.

Source: Systematic Income CEF Tool

In the New York sub-sector coverage for all three funds ticked down slightly, though it remains well above 100% for all three.

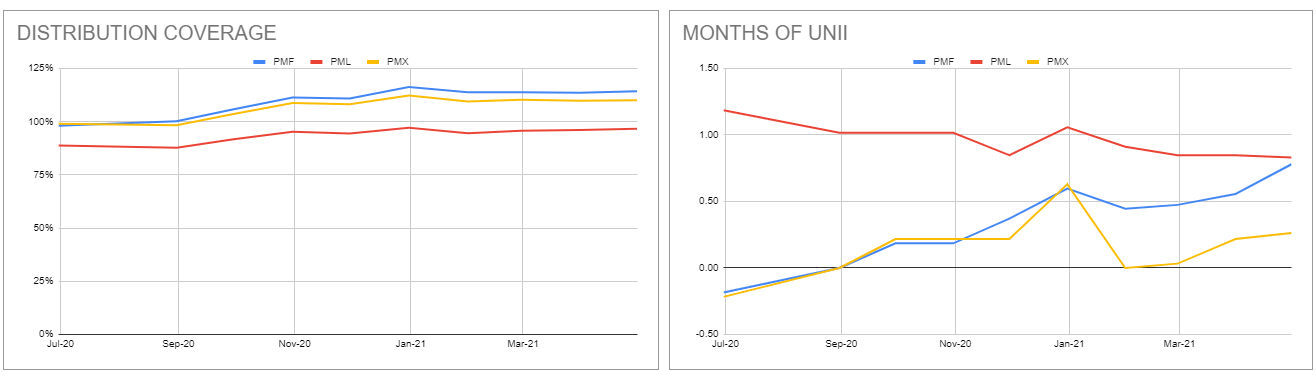

The action in the national tax-exempt sub-sector mirrors that of the California sub-sector with PIMCO Municipal Income Fund II (NYSE:PML) underperforming the other two funds in both coverage and UNII terms. PML UNII has been on a downtrend and will likely give up its first place in the coming months to PIMCO Municipal Income Fund (NYSE:PMF). The gap between PML coverage and the average of the other two funds has grown from 9% a year ago to 15% now. The reason for this is simple - PML has a much higher distribution rate on NAV than the other two funds without any good reason for this. This means that PML remains more vulnerable to a distribution cut or a disproportionate cut versus the other two funds.

Source: Systematic Income CEF Tool

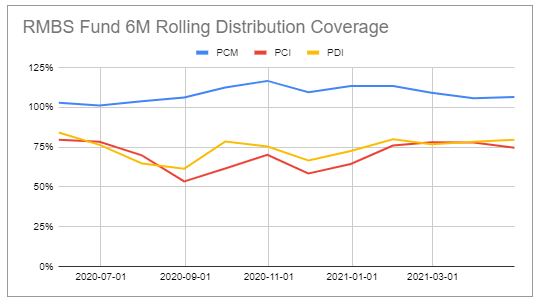

In the taxable suite, PIMCO Dynamic Credit and Mortgage Income Fund (NYSE:PCI) coverage fell 3% while PIMCO Dynamic Income Fund (NYSE:PDI) coverage increased 2% and PCM Fund (NYSE:PCM) increased 1% as well. Interestingly, current 6-month rolling coverage for these funds is roughly where it was a year ago.

Source: Systematic Income CEF Tool

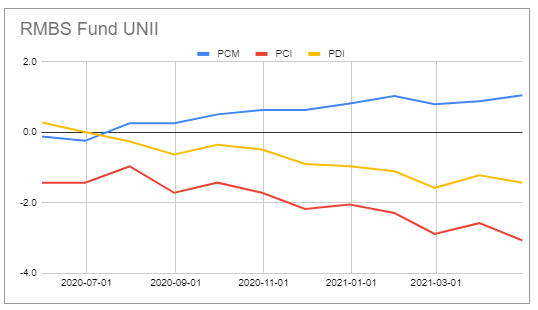

PCI and PDI UNII has continued to drop while PCM has moved higher which is simply the other side of the sub-100% and over-100% coverage coin so it doesn't add a ton of additional information.

Source: Systematic Income CEF Tool

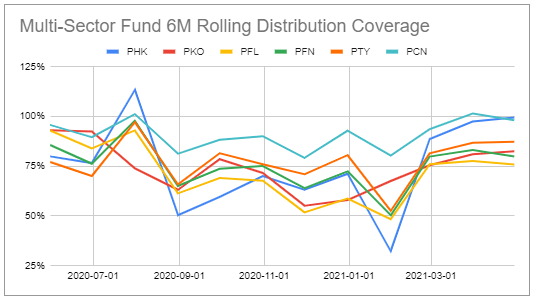

Coverage of the other multi-sector taxable funds moved marginally 1-3% while UNII moved lower across the board which, again, echoes the sub-100% coverage dynamic.

Source: Systematic Income CEF Tool

The new fund PDO does not yet have 6-month (or 3-month, for that matter) figures but its 2-month coverage was reported at 111%. We expect PDO coverage to remain significantly above the average of the other taxable funds due to its much lower distribution rate and elevated leverage.

The key dynamic for coverage moves in the near term is going to be uplift in borrowings discussed above which will likely support or raise coverage in the coming months, all else equal.

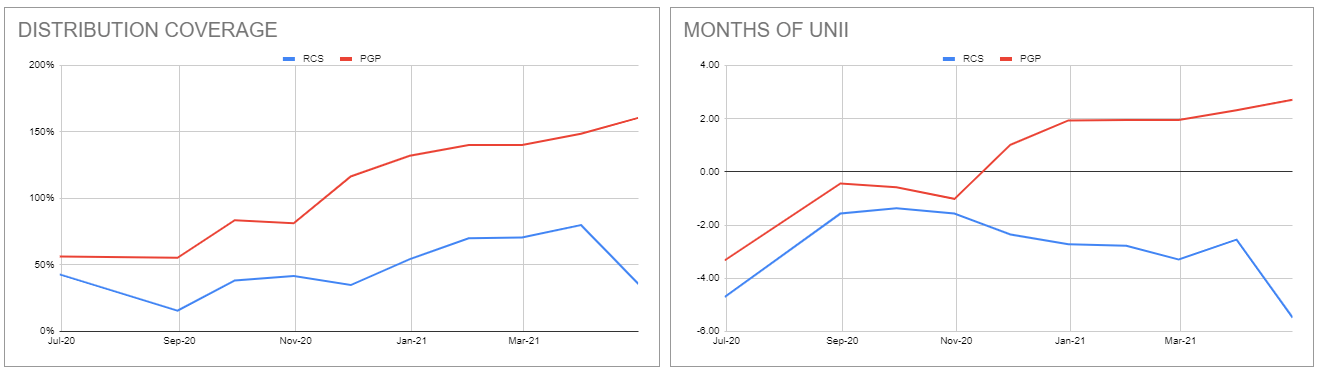

The story is more interesting for the two more idiosyncratic funds, the agency overweight RCS and the hybrid (equity + credit) PGP. RCS coverage has collapsed from 80% to 36% while that of PGP has continued to grow.

Source: Systematic Income CEF Tool

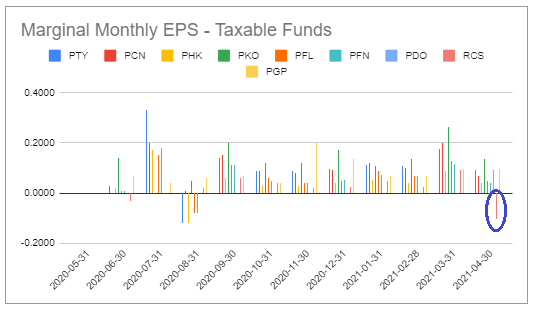

This is a direct result of the fund reporting a drop in its fiscal-year net investment income from $0.33 to $0.23. In other words, the fund reported negative income for April that is nearly the equivalent of two of its monthly distributions. The chart below, which captures monthly EPS, shows how unusual this is. And while negative monthly income is not unheard of for PIMCO CEFs due to their ability to push income in and out of their swap portfolios, the combination of such a large negative number and the fact that only RCS has been affected is a bit unusual, at least relative to the pattern of the last year.

Source: Systematic Income CEF Tool

Past experience suggests that RCS coverage will bounce back, particularly given the fund's large increase in borrowings.

Valuation Update

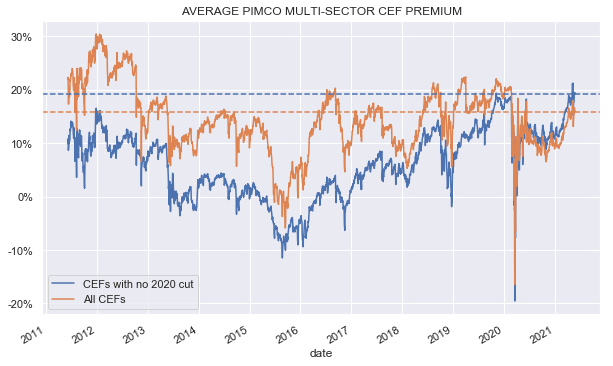

The taxable suite is currently trading at elevated valuations. As usual we present the valuation of two populations - all PIMCO taxable CEFs and the valuation of those CEFs that did not have distribution cuts in 2020. This is because the funds with distribution cuts saw significant drops in their premiums, as we would expect, and their inclusion would make the overall sector appear cheaper than it really is. The upshot here is that PIMCO taxable valuations are just off decade highs (and possibly historic highs though the further back we go the less representative the sample becomes as fewer funds were trading that far back).

Source: Systematic Income

Within the taxable suite we continue to like PDO whose valuation is not only more attractive (though not as attractive as it looks due to its sharing the highest management fees and leverage costs in the taxable suite) but is also more firmly anchored due to its term structure. We discussed valuations in the PIMCO tax-exempt suite in a separate recent article.

Returns Update

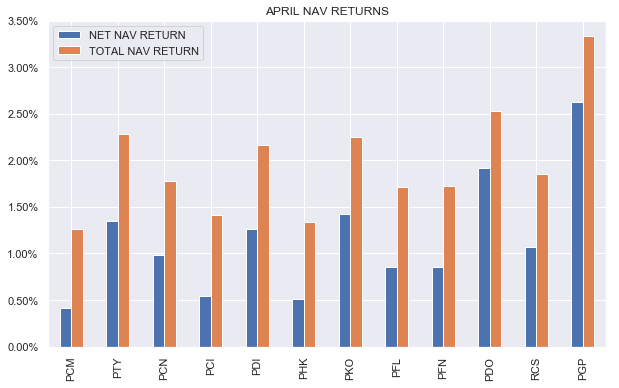

April was a strong month for PIMCO taxable returns, in large part driven by the fall in Treasury yields. All funds registered increases in NAVs, with the equity-overweight PGP outperforming.

Source: Systematic Income CEF Tool

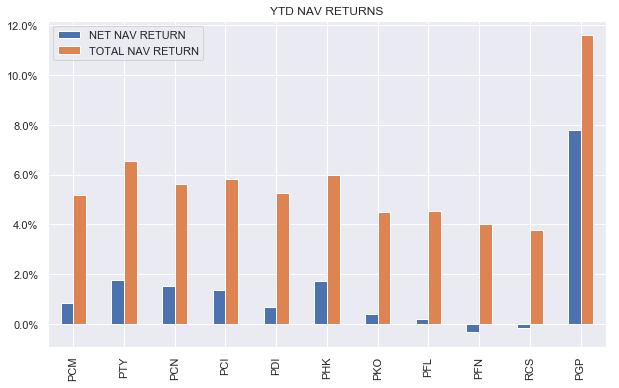

A key theme for the taxable funds and the broader credit fund sector is whether PIMCO will be able to generate returns in excess of their distributions. Our expectation is that unless yields fall, the taxable funds are likely to see some NAV drag since we expect their distributions to be well above their portfolio yields. The strong leverage increase that we saw in April will help in this regard; however, it is unlikely to fully make up the deficit. There is some hope that these funds will be able to generate additional returns through NAV-accretive at-the-market offerings or tactical positioning so further NAV deterioration is certainly not set in stone but it's clearly an uphill climb from where we are. Year-to-date most funds have seen growth in NAVs which is not surprising given the fall in credit yields since then.

Source: Systematic Income

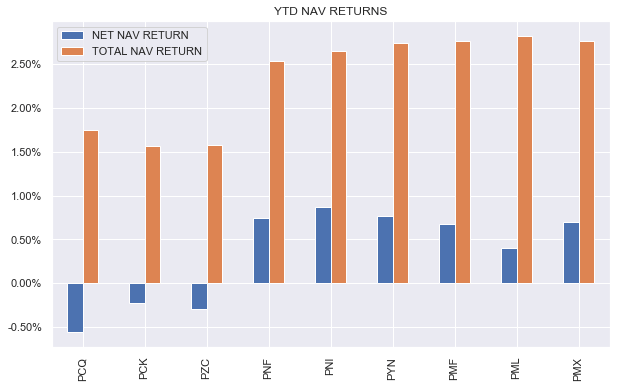

In the tax-exempt space, the California sub-sector has delivered negative net NAV returns as total NAV returns have exceeded distributions year-to-date. It is clear that the much higher NAV distribution rate of PCQ has caused the largest drag on the fund's NAV despite a slightly higher total NAV return in the sub-sector.

Source: Systematic Income

Discount Action

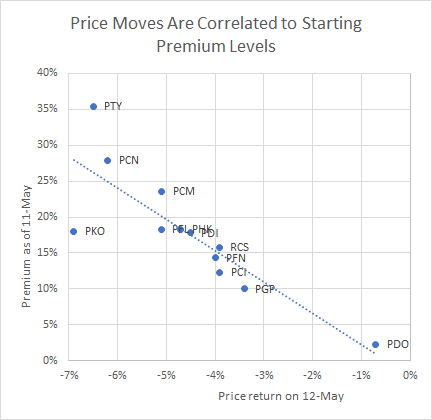

Last week presented a great test case for the behavior of various funds. Our mantra over this persistent rally in CEF discounts has been that higher premiums add fragility to the funds' price action. In other words, a fund trading at a higher premium is much more likely to see a sustained move lower in price during a period of market weakness than funds trading at a cheaper valuation. This price drop can permanently lower portfolio wealth and limit the number of opportunities for rotation. This is particularly true if the fund's premium is due to its high distribution rate. A large distribution cut that right-sizes the distribution is nearly certain to lead to substantial discount widening or premium deflation, delivering a double-whammy to investors of lower distributions as well as poor returns.

The relative price action on 12-May was a case in point. The pattern in price moves was pretty linear – the higher the starting premium the bigger the price drop. This is exactly the dynamic that points to the greater fragility of higher-premium funds.

The strong relationship between the size of the price drop (x-axis) and the initial premium level (y-axis) is not a coincidence. Had the sell-off continued, we expect this relationship to persist, delivering much larger losses to funds like PIMCO Corporate & Income Opportunity Fund (NYSE:PTY), PIMCO Corporate & Income Strategy Fund (NYSE:PCN) and PIMCO Income Opportunity Fund (NYSE:PKO).

Source: Systematic Income

The obvious outlier in the chart is the PIMCO Dynamic Income Opportunities Fund (that we switched into recently on the service) which did not move very much at all. The chief reason for the fund's greater price stability has to do with its term structure, in our view, which anchors the discount more firmly than that of the other funds. Term CEFs are part of our higher-rates playbook that we have put into action on the service.

Our Stance

Our allocation to the suite has been driven by a valuation + catalyst approach. This allocation approach entails allocating to funds trading at an attractive valuation while also featuring a catalyst for outperformance.

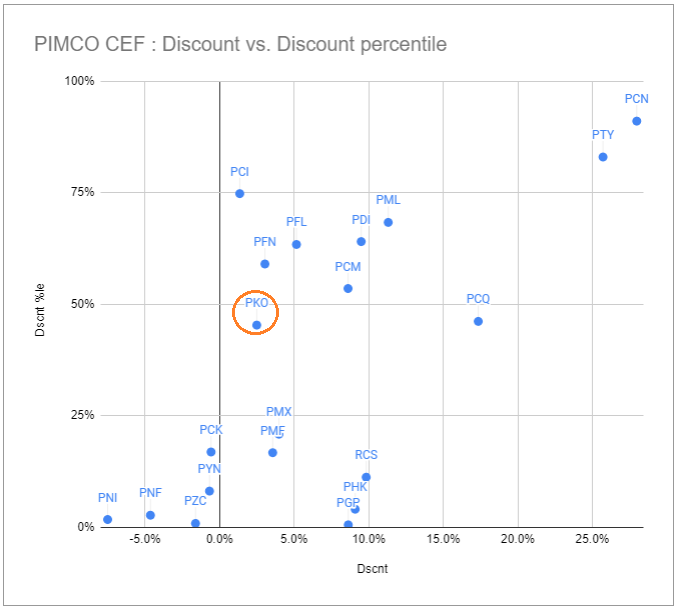

Over the past year we have rotated across three different funds in the PIMCO taxable suite. In June, we highlighted the PIMCO Income Opportunity Fund as our pick in the suite due to its attractive valuation at the time as shown below.

Source: Systematic Income CEF Tool

As well as its increase in borrowings.

Source: Systematic Income CEF Tool

In our view, what the market was not recognizing was the obvious fact that the fund was able to take advantage of the distressed market environment and actually buy assets at the time while many other funds in the taxable suite were busy deleveraging and locking in permanent capital losses for their shareholders. This increase in assets was going to boost the fund's income profile as well. Investors who were paying attention to leverage and borrowing figures were able to recognize that PKO offered an unusually attractive option at the time, not only due to its ability to take advantage of cheap asset valuations but also due to the fact that it remained the most attractively valued fund in the suite - an unusual combination.

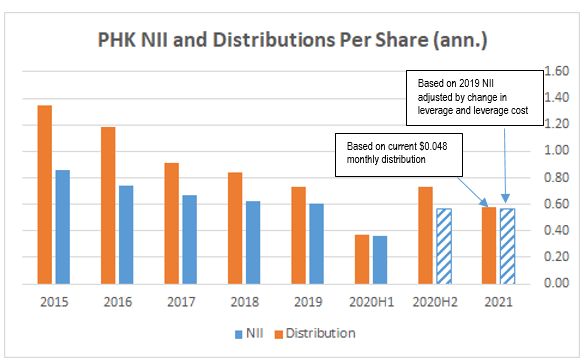

Fast-forward to August when we highlighted the PIMCO High Income Fund (PHK) as the most attractive option in the suite at the time as PKO had repriced higher in line with out expectations and was no longer as attractive. The thesis was the fund's low fee profile (both on the management fee and leverage cost) meant that PHK didn't have to take as much risk to generate the same yield as the other funds in the suite. Secondly, the fund's interest rate positioning via interest rate swaps was particularly attractive in a flat yield-curve environment and could deliver significant gains in a reflationary market environment. And thirdly, the fund's valuation was very depressed due to its repeated distribution cuts. Many investors stayed away from the fund for this very reason, failing to recognize that the fund's distributions had right-sized by 2020 and were on much firmer footing as we can see below.

Source: Systematic Income

Finally, in April we highlighted the new PIMCO Dynamic Income Opportunities Fund (PDO). By then PHK had grown to one of the highest premiums in the suite and the yield curve had steepened significantly, meaning much of the PHK juice was already squeezed. PDO, in our view, offered the same "PIMCO alpha" in a more robust vehicle due to its low premium and term structure.

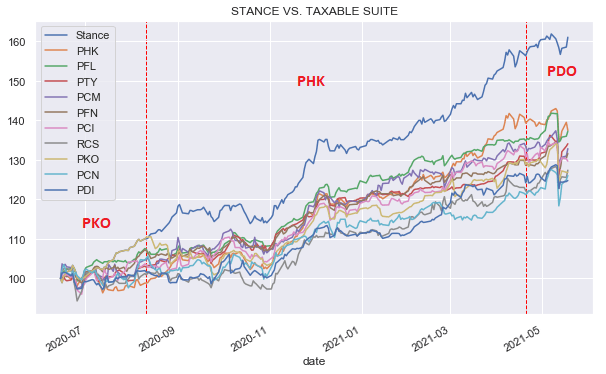

The chart below summarizes this stance over the past year within the taxable suite. The blue line shows the returns of our stance in the sector i.e. the allocation to PKO which is rotated into PHK which is rotated into PDO with the rotations (timing of the articles) marked by red lines. The chart shows the effectiveness of the valuation + catalyst approach which has outperformed all individual funds in the suite.

Source: Systematic Income

Takeaways

PIMCO taxable funds had an unusual month over April, registering a sharp increase in borrowings and driving the average leverage level to, what we believe is, an unprecedented 40%. The timing for this large increase is not immediately obvious since credit valuations remains historically expensive. This increase, if sustained, will marginally improve the distribution coverage of the suite. In the taxable suite, we continue to like PDO due to its more attractive valuation with the term structure providing a stronger valuation anchor in case of a sell-off.

Check out Systematic Income and explore our Income Portfolios, engineered with both yield and risk management considerations.

Use our powerful Interactive Investor Tools to navigate the closed-end fund, open-end fund, preferred and baby bond markets.

Read our Investor Guides: to CEFs, Preferreds and PIMCO CEFs.

Check us out on a no-risk basis - sign up for a 2-week free trial!