Article Thesis

Wells Fargo & Co. (NYSE:WFC), one of the worst performers among major banks in recent years, has seen its shares rise quite a lot in recent months. Optimism about the bank's future profitability, as well as announced capital return plans, have made the market realize that shares were undervalued going into 2021. Right now, shares are a little more expensive, but not overvalued at all. With the dividend doubling in the foreseeable future, Wells Fargo could be on track for becoming a major income investment once again - a status it had lost when it cut the dividend last year.

How Much Is Wells Fargo's Dividend Per Share?

A little more than a year ago, that answer was $0.51 per share per quarter, which equated to an annual payout of a little more than $2 per share. During the pandemic, however, Wells Fargo decided to cut its dividend by about 80%, which is why the payout shrunk to just $0.10 per share per quarter. The most recently announced dividend, with a pay date of June 1, was at that level as well. Wells Fargo has, however, pre-announced a dividend hike that will occur during the second half of the current year. Wells Fargo has, like all other major banks, passed the Fed's stress tests, which is why the bank has been cleared to ramp up its shareholder returns massively over the coming quarters. The bank announced that it plans to increase its dividend to $0.20 per share per quarter, which equates to a $0.80 annual payout, and which doubles the current dividend rate. On top of that, Wells Fargo also plans to spend up to $18 billion on buybacks to reduce its share count, which I see as a positive as well.

What Is The Ex Dividend Date For Wells Fargo?

It is not yet certain when the new dividend will be officially announced and paid, but past dividend increases following clearance by the Fed were usually announced in late July, with payment dates in early September. I thus would not be surprised to see Wells Fargo officially declare a $0.20 per share dividend a couple of weeks from now, as this would match historic patterns.

My assumption is thus that the announcement will occur during the last week of July, and if history serves as a guide, then the ex-date should be somewhere in the first half of August. No exact dates are announced yet, however, and there is no guarantee that the future pattern will be the same as the historic pattern.

Is Wells Fargo A Good Dividend Stock To Buy Now?

Calculating with a $0.20 quarterly payout, Wells Fargo offers a forward dividend yield of 1.8% at current prices. This is more than what one can get from the broad market, as the S&P 500's dividend yield is just 1.3%. A yield of a little below 2% is, however, not an overly high yield. It also isn't an industry-leading yield, as the following comparison shows:

| Bank | Dividend per share, forward | Dividend yield, forward |

| JPMorgan (JPM) | $1.00 per quarter | 2.6% |

| Bank of America (BAC) | $0.21 per quarter | 2.0% |

| Goldman Sachs (GS) | $2.00 per quarter | 2.1% |

| Morgan Stanley (MS) | $0.70 | 3.0% |

Source: Author's calculation

We see that major banks such as JPM and BAC offer higher yields than Wells Fargo on a forward basis, as Wells Fargo was not the only bank that signaled a dividend increase. Together with Morgan Stanley, which also pre-announced a dividend hike by 100%, Wells Fargo offered the highest dividend growth rate, however. On top of that, Wells Fargo also has a pretty low dividend payout ratio, at just 22%. Morgan Stanley, the highest-yielding stock among these five, has a dividend payout ratio of 40% on a forward basis, for comparison.

The low dividend payout ratio of Wells Fargo is, of course, the result of the dividend cut last year, but at the same time, the low dividend payout ratio should allow the bank to increase its dividend meaningfully in coming years as well. It is pretty unlikely that Morgan Stanley doubles its dividend again next year, whereas that seems possible for Wells Fargo if things go right. In fact, at $0.40 per share, the dividend would still be slightly lower than the dividend payout before the pandemic. It is very much possible that we will see more nuanced dividend increases from Wells Fargo in 2022 and beyond, but it undoubtedly is true that a dividend payout ratio in the low 20s should allow the bank to ramp up its dividends considerably in the future. Whether management decides that this is the best strategy, or whether they prioritize buybacks is another question.

Wells Fargo's stock has still not fully recovered from the accounting scandal a couple of years ago, as its shares still trade at a 30%+ discount to the all-time high right now. The Fed still constricts the assets that Wells Fargo is allowed to have on its balance sheet, and on top of that, expenses are at an above-average level, which is why Wells Fargo's efficiency ratio is significantly worse than those of its major peers. This is, however, a problem that should eventually get solved. It is, I believe, unlikely that the asset cap will remain in place for many years to come, and management seems to be focused on reducing expenses to bring the bank's profitability more in line with its peers. Combine the potential for asset growth, expense reduction, and buybacks that can be done at a relatively inexpensive valuation, and Wells Fargo could grow its earnings per share considerably in coming years.

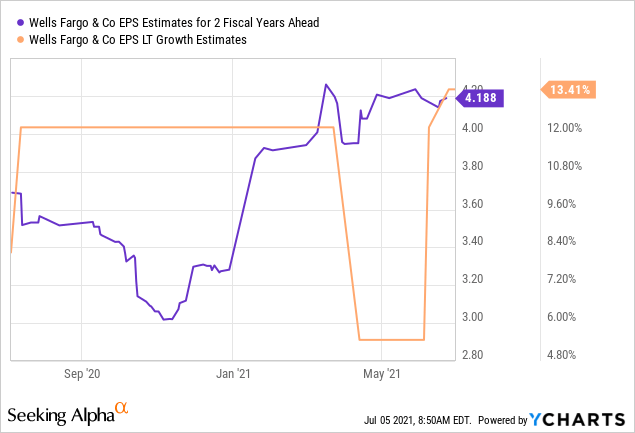

Analysts are currently forecasting EPS of $4.19 for 2023, and with long-term growth being forecasted at 13% a year, Wells Fargo's earnings per share may grow to somewhere between $5.25 and $5.50 by 2025.

If Wells Fargo were to pay out 40% of its earnings per share by the mid-2020s, then this could result in dividend payments of north of $2 per share per year. In other words, investors buying at today's prices may see a dividend yield on cost of about 4% to 5% a couple of years from now, which would not at all be unattractive. The forecasted earnings per share growth could also result in meaningful share price upside. Put an 11-12x earnings multiple on the 2025 estimate, and shares have upside potential to around $60 over the next four years, which would result in a high-single-digit share price growth rate relative to the current share price of $45. There is no guarantee, of course, for that to happen, and this scenario rests on management's ability to bring the bank back on track and to reduce expenses meaningfully. For those that believe in CEO Charles Scharf's ability to execute on these goals, Wells Fargo could seem like a very solid investment at today's price. The stock was, of course, an even better pick last year when shares traded in the $20s, but even following gains of 80% since we called WFC a buy in October 2020, shares do not seem like a bad investment today.

Takeaway

Getting a dividend increase of 100% is great, but it should be noted that WFC's dividend yield is still lower than the yields offered by many of its peers. Nevertheless, thanks to a combination of a low dividend payout ratio that leaves a lot of room for dividend hikes, and a solid earnings growth outlook, Wells Fargo could be a solid investment at current prices for those that plan to hold shares for a couple of years. Shares are not looking extremely cheap any longer, but it would not be surprising to me if shares generate meaningful returns over the next couple of years.

Is This an Income Stream Which Induces Fear?

The primary goal of the Cash Flow Kingdom Income Portfolio is to produce an overall yield in the 7% - 10% range. We accomplish this by combining several different income streams to form an attractive, steady portfolio payout. The portfolio's price can fluctuate, but the income stream remains consistent. Start your free two-week trial today!

The primary goal of the Cash Flow Kingdom Income Portfolio is to produce an overall yield in the 7% - 10% range. We accomplish this by combining several different income streams to form an attractive, steady portfolio payout. The portfolio's price can fluctuate, but the income stream remains consistent. Start your free two-week trial today!