Who is Genasys

We all use multiple communication platforms from native text/mobile voice on any phone to WhatsApp, fb messenger, Snapchat, Telegram just to name a few every day. In case of a public emergency event, the objective is to reach and warn every single person in the danger zone independent of service. Genasys (NASDAQ:GNSS) is in the business of providing critical communication services connecting public with the authorities during emergencies. It is comprised of two segments, a historical hardware (Acoustic Hailing Devices - AHD) segment and newer market-specific software platforms pre-integrated with above communication services. All its products are capable of delivering critical emergency announcements with adjustable geo-fencing and geo-locating to a target group for precision. For the government and national telecom operators, Genasys offers National Emergency Warning Systems (NEWS) for first responders, enterprises, and campuses the Emergency Management System (EMS), Enterprise Critical Communications (GEM), and Integrated Mass Notification System (IMNS). In Q2 2021, Genasys added evacuation planning and management to its platforms through its acquisition of Zonehaven.

To understand the evolution of Genasys today, it is best to look at the key acquisitions it made in reverse chronological order.

Zonehaven, as mentioned above, was acquired for $30 million in Q2 2021. It is a specialist in evacuation management as a service. Zonehaven's software works as the nerve center (in the crisis communication center) and connects police departments, city hall, firefighters, emergency, and 1st responders through a mobile app so every official knows in case of a natural disaster like wildfire or storm the exact plan of action, coordination, and real-time updates between different entities and public. While the software platform is comprehensive, it is worth noting Zonehaven is a small 2-year-old start-up with a team of 12 and virtually no revenues. Hence its software is not yet field-tested in multiple disasters and emergencies.

Genasys CEO Richard Danforth explained the rationale during FY Q3 2021 call: "I expect explosive growth from Zonehaven, and their pipeline is robust, and we're beginning to see it." Zonehaven is presented as a growth catalyst both as standalone and in combination with GEM and IMNS products by Genasys CEO: "By continuing to offer Zonehaven software as is, and integrating it with the GEM enterprise software and as a layer in our Integrated Mass Notification System, Genasys will have 3 key competitive advantages for securing local, regional, and national emergency management and warning contracts."

The second strategic acquisition is Amika Mobile for which the company paid $8.4 million and closed the acquisition in August 2020. Amika develops GEM software for enterprises from colleges to manufacturers to healthcare (for covid-19 tracking) for situational awareness, two-way communications across devices, networks, and services (such as SMS, Twitter, VoIP, overhead signs, Websites, broadcast TV, radio...) and integration with 3rd parties, the real strength of GEM. It allows the customer-specific use cases to be tailored and configured combining inputs disparate sources from weather forecasting to local or federal police systems, to fire departments, to automatic video cameras with image recognition as required by the customers.

The main unknown is again low number of deployments to date. Integration, even though accelerated by well-documented APIs takes time to get it right, there is a lot of project management involved from both customer and Genasys side and software must be maintained to ensure compatibility. The more 3rd party integration the more complex it is to keep software up to date.

Genasys was the turning point for LRAD corporation, which was the former name of the company. LRAD acquired a Spanish company called Genasys which developed mass notification software (IMNS) for purchase price of $3 million in 2018. Before rebranding, LRAD invented, patented, and sold directional Acoustic Hailing Device (AHD) technology since early 2000s to deliver long-range sound with extreme clarity up to several kilometres away.

AHD has very broad civilian, military, and law enforcement applications, and Genasys offers LRAD 100, which has a range of 600 meters to 2000x, which can carry sound up to 5.5 kilometers. Genasys sells LRAD devices in more than 100 countries to generate between 15 - 25 million per year. For an overview of use cases, LRAD devices are used, and the technology behind the products that differentiate from older technologies, the company has put together a number of in-life customers and trial videos.

Compared to pre-2018 where LRAD was mainly a hardware hailing device business, Genasys, if they can successfully integrate the 3 companies, will become a vertically integrated critical communication as a service company with an addressable market of $11 Billion (source: August 2021 investor presentation) and a mid/long-term target of achieving $100 million within 3 to 5 years. Post-Zonehaven acquisition, the CEO believes company will achieve 100 million in sales in 3 years than five in the latest earnings call "I've said before multiple times that the company would be $100 million in 3 to 5 years. The Zonehaven acquisition will get us there closer to 3 than 5. So I think."

Opportunities Are Increasing

The main reason Genasys management believes it can achieve 3x growth is the European Union (EU) mandatory directive to set up a national emergency warning system in 25 countries with a decision deadline in 2022. The Public Warning Service (PWS) set-up is typically a central government agency managing the front-end while individual mobile operators picking the back-end suppliers. Genasys has the credibility, knowledge, and experience from Australia where 2 of the 3 mobile operators have been using its mass communication PWS solutions for several years already. While a few countries are running a single tender to pick both front- and back-end suppliers, most of the EU countries allow each telecom operator to choose own supplier which means Genasys will be competing for 4-5 separate tenders in most countries.

Assuming 30+ total tenders with average value of $0.5-1 million per year per tender just within EU, the 100 million revenue goal by 2025 sounds rational. However, Genasys is not competing alone, the PWS contract for France went to a French company and Estonia chose another supplier due to lower price recently. Still, 23 countries to go until June 2022...

Competitive Landscape

Genasys has many competitors. Large telecom suppliers like Nokia (NOK), Ericsson (ERIC), Huawei, ZTE (OTCPK:ZTCOF), and specialists like Airbus (OTCPK:EADSF) all develop and offer their critical communication platforms. However, these platforms are mainly for mobile networks for SMS and voice and lack integration with social networks. None of them have end-to-end solution portfolio or the flexible and open integration Genasys software offers out of the box. Crucially, mobile network equipment makers, Nokia and Ericsson, partner with Genasys for mass notification instead of head-on competing.

The most significant mass-market notification competitor of Genasys is Everbridge (EVBG) according to the company's FY 2020 10-K report: "We compete against several domestic and international competitors, including Everbridge, OnSolve, Whelen Engineering Company Inc., Hoermann, and others."

Everbridge has phenomenal top line growth since 2012 as a serial M&A machine. Since Everbridge is public, a closer look into its fundamentals will be useful to understand the competition and market dynamics better.

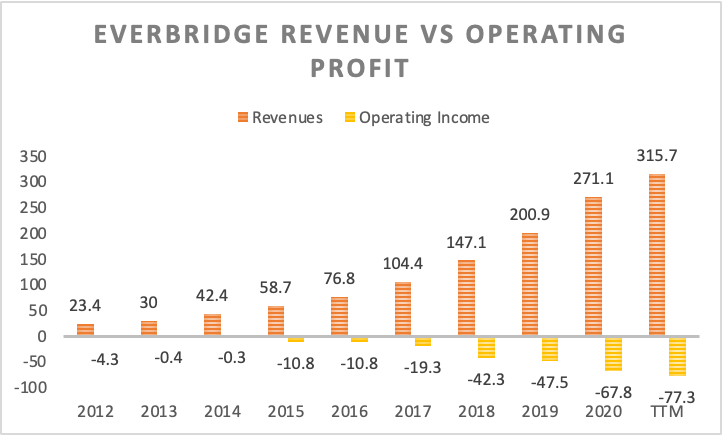

The first graph compares Everbridge's revenues with the underlying profits from 2012 to now. While the top line growth looks impressive, the widening continual loss from operations looks concerning.

Figures source: Seeking Alpha

Figures source: Seeking Alpha

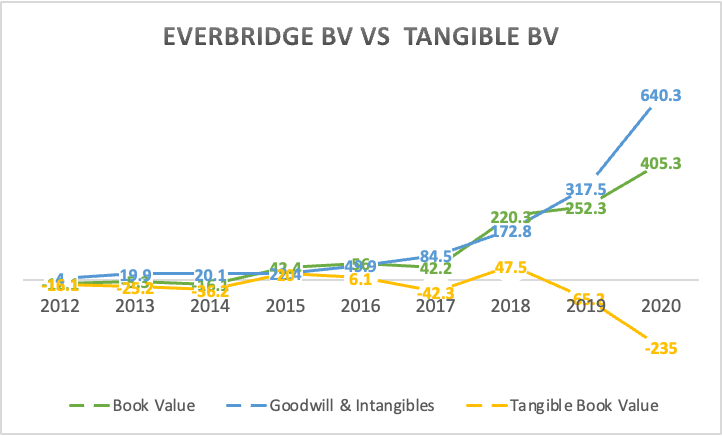

The second graph below is about comparing the book value with tangible book value by subtracting goodwill and intangibles from equity. If Everbridge tangible equity is increasing, that is a positive sign. It means acquisitions are generating positive cash flow and contributing. Unsurprisingly, as the company has not yet been profitable, tangible book value is increasingly negative. Everbridge has paid a lot for top line growth, taken on significant debt to finance acquisitions (standing at 646.5 million in latest report and paying more than 24 million in yearly interest expenses). A lot of shareholder value has been destroyed since 2012 as the price of acquisitions is far above the value generated so far.

Figures source: Seeking Alpha

The story of Everbridge is so far unprofitable and overpriced acquisitions should be a warning bell. Of the $25.9 million purchase price allocation currently recorded on Genasys' balance sheet for Zonehaven, $25.6 million is goodwill and intangibles and no revenues to speak of yet (source: Q3 2021 10-Q).

While Genasys has been very disciplined, Zonehaven's acquisition cost compared to Amika Mobile and Genasys looks almost exuberant bordering on irrational even if it is a unique, fully complementary strategic acquisition. Mass critical communication customers are price-sensitive, paying a major price premium for an asset means Genasys needs high prices to earn back the investment. Genasys management highlighted this issue themselves when they lost Estonian national public warning contract: "The country of Estonia made an award. Although Genasys was rated number 1 technically, we were second at price and the award went to the lowest price bidder." Technical capabilities and lowest price, thus setting up the company for low-cost structure, go hand in hand in this market.

What is Genasys' Intrinsic Value

Genasys won several important contracts in the first half of 2021 against incumbent competitors, most notably a multi-year major automotive manufacturer with 25,000 people across 24 plants in US and 12 in Canada and Riverside County, California with its GEM solution. Follow-on orders for LRAD with multi-year contract from US military keep coming where Genasys is the incumbent for AHD for all branches from coast guard and Navy to the Army. More importantly, Genasys looks future-ready, differentiated in number of software solutions and key features to address any use case/customer, and has a medium-sized moat called LRAD.

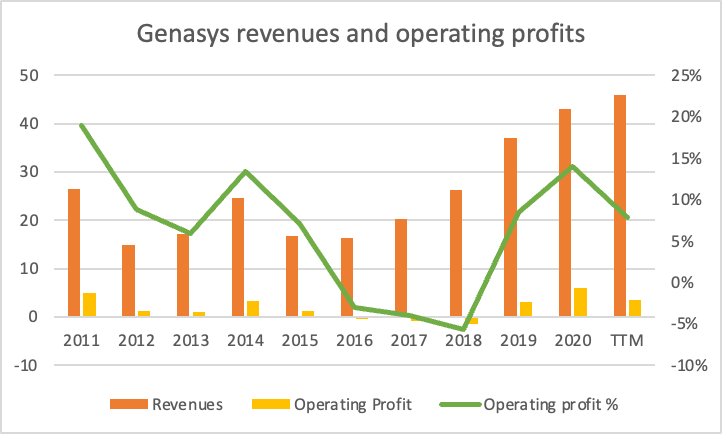

Genasys also has a good track record of profitability, at least versus Everbridge. It has been unprofitable only for 2 years in 2017 and 2018. Revenues are consistently growing since 2016 and reached above $40 million in FY2020. Healthy operating profit % between 10-15% in the past 3 years.

Figures source: Seeking Alpha

Calculating intrinsic value is highly dependent on the model and assumptions used. Since Genasys is going through a major transformation of business model and products, I believe the most apt approach for value investors is looking at the value of its assets first rather than the earnings power to put a floor on the price.

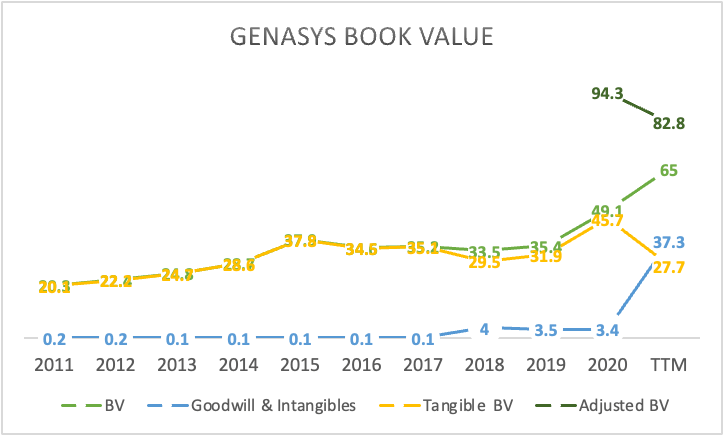

For the asset-based valuation, we are going to compare its current book value, tangible book value, and adjusted book value. For adjusted book value calculation, R&D and SG&A will be treated as long-term assets. For R&D, we will sum last 4 years (about $17 million - typical for software) and for sales and marketing investments, we will take the last 3 years (about $36 million - to set up a global sales organization) in the assumptions. The intrinsic value of Genasys then is approximately:

- Book Value: $65 million ($1.93/share)

- Tangible Book Value: $37 million ($1.11/share)

- Adjusted Book Value: $83 million ($2.46/share)

Genasys' intrinsic value has kept increasing nicely since 2012 where normal and tangible book values were identical until 2021 and the current share price of $5.24 looks fair.

Figures source: Seeking Alpha

Conclusion

The world is full of hazards. Genasys has built critical and mass communication solutions to act fast and manage the public and help mitigate these hazards completely or minimise the risks to human life and property. We like the company's management, the strategic transformation it has gone through to become a one-stop-shop critical communication platform, its long-term financial performance, and the repeat customer orders it has received from Australia and law enforcement agencies. Provided they can act on price, start valorising Zonehaven, and win the next EU public warning tenders, Genasys has room for future growth.