Introduction

During the March 2020 stock market crash, I was able to broaden my exposure to regulated utilities at a favorable price by initiating a small position in PPL Corporation (NYSE:PPL). I had absolutely no intention to sell the position and – quite the contrary – planned to bring it to size after completion of my due diligence. I was intrigued by the geographic diversification and the above-average operating margin (on average 40 % in the years 2015 to 2020). However, fears of regulatory headwinds made me reconsider, and I came to the conclusion that the UK division could prove problematic going forward. Also taking into account the leverage of over five times net debt to EBITDA in conjunction with the volatile earnings and the substantial interest burden, I decided to sell the position and move along.

In March 2021, management announced a strategic repositioning, comprising of the sale of the UK division to National Grid plc (NGG) and the subsequent acquisition of Rhode Island-based Narragansett Electric Co. This made me reconsider, and I got interested in the company once again.

In this article, I outline the impact of the deal on both the balance sheet and the income statement. Furthermore, I provide valuations for PPL OldCo, PPL NewCo and the two swapped assets, comparing them to other regulated utilities. I estimate PPL’s dividend, taking into account average earnings and margins from the past several years, reduced interest expenses, shares repurchases and savings in corporate overhead. Fellow Seeking Alpha contributor Ray Merola has authored a similar piece on PPL earlier this year. I found his research substantiated but figured that my point of view – approaching the result from a different route while extending on the debt situation – should also prove helpful to both existing and potential new investors.

PPL OldCo – a brief overview

PPL is a well-established regulated utility operating in Kentucky, Pennsylvania and – until recently – in West England and Wales. Over the course of the last six years, revenues went nowhere, as can be noticed from the following figure:

Figure 1: Revenues of PPL Corp. (data from the company's most recent 10-K, compiled by the author)

Figure 1: Revenues of PPL Corp. (data from the company's most recent 10-K, compiled by the author)

Similarly, PPL’s operating earnings and net earnings did not grow measurably and came in rather volatile. On average, PPL generated USD 1.6 billion in net earnings per year. The UK business unit accounted for 51% and 56% of operating and net earnings, respectively, assuming that corporate expenses are split 50/50 among the two segments units.

PPL’s margins appear to be very robust. On average, over the course of the last six years, the UK segment reported operating and net margins of 71% and 44%, respectively. The margins of the two US divisions are substantially weaker, as can be learned from the following table:

EBITDA margin | EBIT margin | Net margin | |

UK division | 83 % | 71 % | 44 % |

Kentucky division | 42 % | 27 % | 12 % |

Pennsylvania division | 46 % | 30 % | 17 % |

Weighted average - US divisions | 44 % | 28 % | 15 % |

Table 1: Average margins of PPL Corp.’s operating segments (2015 – 2020) – the weighted average margins have been computed by taking into account the relative contributions of the respective divisions (data from the company's most recent 10-K, compiled by the author)

A brief examination of the balance sheet exposes the substantial leverage that PPL is operating with. Considering an average EBITDA of USD 4.2 billion over the course of the last six years and a net debt of USD 24.1 billion as per the 2020 10-K, net debt to EBITDA amounts to approximately 5.7x.

The deal with National Grid plc

PPL agreed to sell its UK division to National Grid for pre-tax proceeds of USD 10.7 billion in cash (approximately USD 10.4 billion after tax). In addition, USD 266 million in cash and cash equivalents as well as roughly USD 8.9 billion in debt are transferred to National Grid. The sale has already been completed, and the assets and liabilities are no longer accounted for on the most recent balance sheet. A part of the proceeds has already been directed towards debt retirement, and PPL’s net debt has decreased substantially.

As part of the transaction, PPL acquires Narragansett Electric Co. from National Grid for roughly USD 3.8 billion in cash, while assuming USD 1.5 billion in net debt. This part of the deal is expected to close in early 2022.

In the following table, selected balance sheet items of PPL OldCo (as per December 31st 2020), PPL NewCo (as per June 30th, 2021) and pro-forma PPL NewCo (upon completion of the transaction) are outlined:

(USD millions) | PPL Dec 31 2020 | PPL June 30 2021 | PPL NewCo pro-forma |

Short-term debt | 3,236 | 2,200 | 2,200 |

Long-term debt | 21,553 | 11,095 | 12,595* |

Cash and equivalents | 708 | 7,629 | 3,829** |

Table 2: Selected balance sheet data of PPL Corp. * includes the debt assumed due to the acquisition of Narragansett Electric Co. ** the cash consideration for Narragansett Electric Co. has been deducted (data from the company's most recent 10-K and 10-Q filings and from the presentation outlining the transaction, compiled by the author)

Evidently, the debt situation improves materially and a substantial amount of cash remains on hand. Management appears to be committed towards disciplined investments in renewables, and/or share repurchases (slide 4 of the presentation). In July 2021, PPL’s board of directors authorized share repurchases of up to USD 3 billion (page 69 in the second quarter 10-Q).

Valuation metrics

PPL OldCo reported net debt of USD 24.1 billion at the end of fiscal 2020 (Table 2) and had 770 million shares outstanding. Taking into account a share price of USD 29 and six-year average EBITDA and EBIT figures of USD 4.2 billion and USD 3.1 billion, respectively, the market valued PPL OldCo at EV/EBITDA and EV/EBIT multiples of 11.0 and 15.2, respectively.

Upon closing of the transaction, the Narragansett assets are expected to yield adjusted net earnings of roughly USD 150 million per annum. In stark contrast, PPL’s UK division yielded USD 966 million in net earnings on average over the course of the last six years.

The sale of the UK division is valued at EBITDA/EV and EBIT/EV multiples of 10.5 and 12.3, respectively. These valuation metrics are based on the sum of the cash consideration of USD 10.7 billion and the debt of USD 8.7 billion assumed by National Grid as well as, on average, EBITDA and EBIT figures of USD 1.8 billion and USD 1.6 billion, respectively.

Assuming that the Narragansett assets exhibit similar margins as the Kentucky and Pennsylvania divisions (Table 1), the USD 150 million in expected net earnings would translate to EBIT and EBITDA figures of USD 288 million and USD 447 million, respectively. Taking into account the cost of the purchase of Narragansett Electric Co. and the net debt assumed by PPL (i.e. USD 5.3 billion in total), the acquisition is valued at EBITDA/EV and EBIT/EV multiples of 11.9 and 18.4, respectively.

With Narragansett’s contribution, I expect PPL NewCo’s EBITDA and EBIT to come in at roughly USD 2.8 billion and USD 1.8 billion, respectively.

The current balance sheet exhibits a sizable amount of cash on hand that will be, at least in part, directed towards share repurchases. However, in the course of calculating EV, I did not account for share repurchases (that would reduce the equity part of the calculation) since the cash on hand is accounted for anyway when computing net debt, which is also part of the calculation.

With a share price of USD 29, the market values PPL NewCo at EBITDA/EV and EBIT/EV multiples of 11.8 and 18.8, respectively, which is slightly higher than the valuation of PPL OldCo. From a conservative point of view, one could remove USD 1.7 billion of the remaining cash from the EV calculation since capital expenditures due to renewables have also been announced. This would increase the multiples to 12.4 and 19.7.

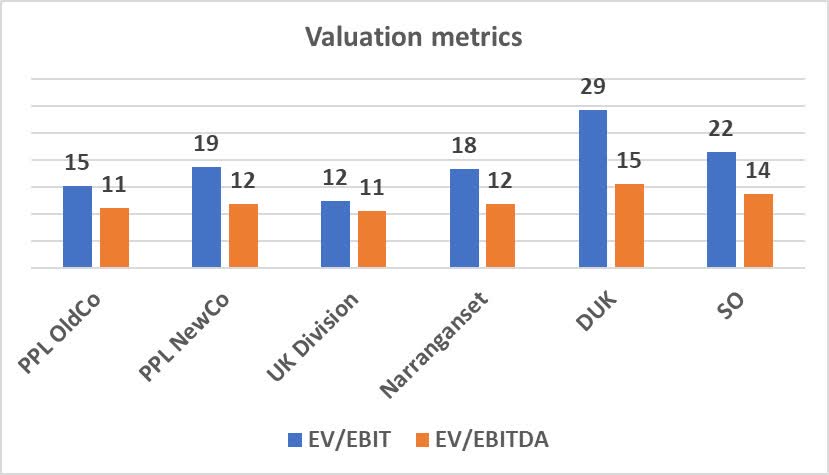

In terms of EV/EBIT multiples, it appears as if PPL paid a premium for Narragansett Electric Co., while selling its UK division for a lower multiple. In comparison to other publicly traded utilities such as Southern Company (SO) and Duke Energy (DUK), both sides of the deal, as well as the projected future valuation of PPL NewCo appear reasonable:

Figure 2: Valuation metrics (computed from the most recent 10-K and 10-Q filings of the respective companies and from the presentation outlining the transaction, compiled by the author)

Making sense of PPL NewCo’s leverage

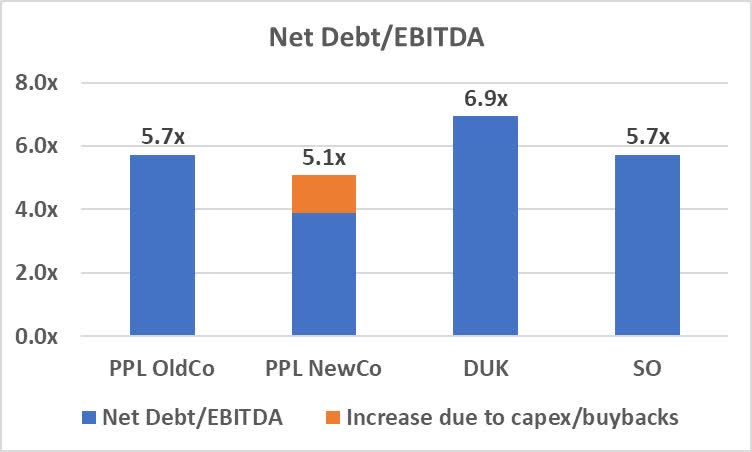

The transaction certainly improved PPL’s balance sheet. As mentioned before, PPL NewCo should be able to generate annual EBITDA of roughly USD 2.8 billion. With projected net debt of USD 11 billion, the leverage of PPL NewCo falls to roughly 3.9x EBITDA. This compares favorably to PPL OldCo and other regulated utilities such as DUK or SO. Note, though, that this estimation does not account for investments in renewables and share repurchase. The excess USD 3.8 billion in cash remains on hand (as per pro-forma March 31st, 2022, balance sheet, Table 2). If the company invests roughly USD 1.7 billion in renewables and retires USD 1.7 billion worth of shares, leaving USD 429 million in cash on hand, the company’s leverage ratio would stand at 5.1, which is arguably worse but still acceptable.

Figure 3: Leverage ratios of PPL OldCo, NewCo and peers (data from the most recent 10-K (EBITDA values) and 10-Q filings (balance sheet data) of the respective company with the SEC, compiled by the author)

Figure 3: Leverage ratios of PPL OldCo, NewCo and peers (data from the most recent 10-K (EBITDA values) and 10-Q filings (balance sheet data) of the respective company with the SEC, compiled by the author)

Estimation of PPL NewCo’s dividend

As mentioned before, PPL’s UK division accounted for approximately 51 % of operating earnings. As outlined earlier, I expect PPL NewCo’s operating earnings to come in at roughly USD 1.8 billion. This assumes that the acquired business unit does not increase corporate expenses and that 50 % of OldCo’s corporate expenses are associated with the Kentucky and Pennsylvania business units. The other 50% are assumed to be saved due to decreased corporate overhead, now that PPL is no longer exposed to the UK.

Due to the significant deleveraging, a review of the interest payments is warranted. PPL OldCo paid USD 1,001 million in interest in 2020. Management provided a breakdown of the interest expenditures with respect to the business units (page 130 of the 2020 10-K). Assuming that interest payments associated with corporate are split 50/50 among the US and the UK division, the UK division accounted for 46 % of the interest expenses, and hence, the remainder (i.e. USD 537 million) is associated with PPL’s US divisions. With currently outstanding debt of USD 13.3 billion, this translates to an interest rate of 4.04 %. Upon completion of the acquisition of the Narragansett assets, debt is increased by roughly USD 1.5 billion. Slapping the same interest rate on the additional debt, PPL NewCo is looking at roughly USD 600 million in annualized interest obligations going forward.

With a corporate tax rate of 21%, EBIT of USD 1.8 billion and USD 600 million in interest, I expect PPL NewCo to generate net earnings of USD 944 million going forward. This corresponds to EPS of USD 1.23. Taking share repurchases of USD 1.7 billion and a share price of USD 29 into account, the free float should shrink to 711 million shares, lifting EPS to USD 1.33.

On slide 14 of the March 18, 2021, presentation, management stated that the dividend is projected at around 60-65% of EPS post-closing of the transactions. Currently, PPL pays an annual dividend of USD 1.66 per share. If my estimations are somewhat accurate and management aims towards the high side (i.e. 65 %), this would translate to a dividend of USD 0.86 per share. With a current share price of USD 29, the dividend yield would be 3% - clearly not what income-oriented investors would expect from a regulated utility. Note that these assumptions do not factor-in the proposed increase in corporate tax rate to 28%.

As per Ray Merola’s model, an annual dividend of USD 1.33 appears defensible. Here are the main reasons for the divergence from my estimation:

- My earnings figures are based on six-year averages, whereas Ray Merola appears to have used the 2020 figures.

- Ray Merola’s calculation of interest rate is based on the long-term debt as per 2020 10-K whereas my calculation is based on the short- and long-term debt as per second quarter 10-Q.

- My calculation estimates that the UK division accounts for 46 % of the interest expenditures, whereas Ray Merola estimates 50 %. In total, his NewCo interest expense is expected to be USD 500 million, whereas I arrive at roughly USD 600 million (USD 537 million from the RemainCo and 60 million from Narragansett’s assumed debt).

I do not want to imply that my estimation should be favored over Ray Merola’s. My estimation appears somewhat more conservative and thus could serve as a lower boundary for investors. In case I missed a significant EPS contributor, I would greatly appreciate a notice in the comments below.

Conclusion and Outlook

My estimation comes to the conclusion that a future dividend of USD 0.86 per share is likely. Thus, I refrained from re-opening a position in PPL since I deem a dividend yield of only 3.0% not enough for a regulated utility. Nevertheless, in case the share price drops to a level reflecting a yield of 3.5% to 4.0%, I would be interested in acquiring shares of the company. Quite frankly, I doubt that PPL’s share price drops to such a level since this would indicate a massive valuation gap in terms of EV/EBITDA in comparison to larger peers.

As a bottom line, I would like to draw your attention to the fact, that former CFO and CRO of Southern Company has been elected a director of PPL as per October 1st, 2020. Probably, the repositioning of PPL is a strategic step en route to a buyout by a larger utility?

Thank you very much for taking the time to read through the article. I appreciate your input in the comments below or via private message, and I hope that my reasoning sparks an interesting discussion about PPL.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.