CHEGG is a Buy online learning Uwe Krejci/DigitalVision via Getty Images

Chegg (NYSE:CHGG) is a growth stock. Its average 5-year revenue CAGR is 22.96, and forward revenue CAGR is 34.35%. Investors should consider taking advantage of CHGG's-24.03% YTD price performance. Chegg is now a more affordable investment in the fast-growing $250 billion e-learning industry. CHGG's forward P/E is now only 38.59x.

The online education business is predicted to be worth $1 trillion by 2027. Chegg has 6 million U.S. subscribers. It also has 1 million international subscribers.

(Source: Global Market Insights sample PDF)

The current headwind is obvious. I expect CHGG's price to decline further because of the legal dispute with Pearson (PSO). These two are former partners. There's a good probability they would be able to settle their differences out of court.

Anyhow, the total cash position of Chegg is $2.06 billion and its net operating cash flow is $258.75 million. Chegg can afford to hire the best lawyers to fend off Pearson.

Why Invest

The Piotroski F score of CHGG is 5. It has healthy finances. This financial attribute could only get better after Chegg's 1-to-1 online tutorial service, Thinkful, attracts more paying customers. Thinkful allows its customers to pay in multiple ways. It could become the next Lynda.com. LinkedIn bought Lynda.com for $1.5 billion six years ago.

Udemy.com has more than $1 billion valuation during its 2020 fund-raising. If you can evaluate Chegg beyond its conflict with Pearson, CHGG is a good growth stock. Online education has a long-term tailwind from COVID-19. The Delta variant is highly contagious. Learn-from-home is the safer choice versus face-to-face classes/tutorials.

Chegg offers a diversified suite of support materials and services for learners and educators. Aside from selling and renting text books, Chegg is a Software-as-a-Service company which charges monthly subscription fees for its web/mobile apps.

(Source: Learn.com)

Most busy parents won't mind paying monthly subscription fees so that their kids can use Chegg's homework helper and math solver apps. Thesis and essay writings of K-12 and college students could be improved using Chegg's paid plagiarism/grammar checker and expert proofreading services.

This company could become consistently profitable. A check on its hiring requirements revealed Chegg is actively recruiting tutors in India. Chinese online education companies like 51Talk are avid employers of Filipino online tutors. 51Talk's offer to experienced tutors is just PHP100 ($2.00) per hour.

Chegg can hire Filipino math and science tutors at $2.50/hour and charge American parents $8 - $16 per hour. This could partly reverse the continuing net loss handicap of Chegg. Thinkful.com copying the flat $29.99/month to access all tutorials/lessons of LinkedIn Learning (new name of Lynda.com) might attract professionals who want to learn new skills.

The screenshot below says Thinkful.com caters to some of the customers that LinkedIn Learning and Udemy.com services.

(Source: Thinkful.com)

Growth Story Is Real

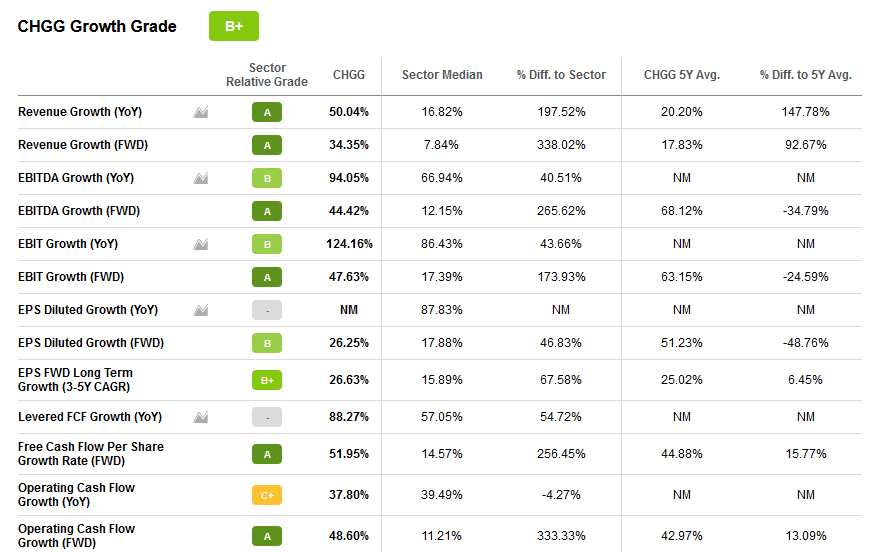

I rate CHGG as a buy because of its high double-digit revenue growth rate. The 21% CAGR of the e-learning business is congruent with Chegg's 5-year average revenue CAGR of 22.96%. Growth potential is the no. 1 priority of most investors. The chart below is a big endorsement for Chegg.

(Source: Seeking Alpha Premium)

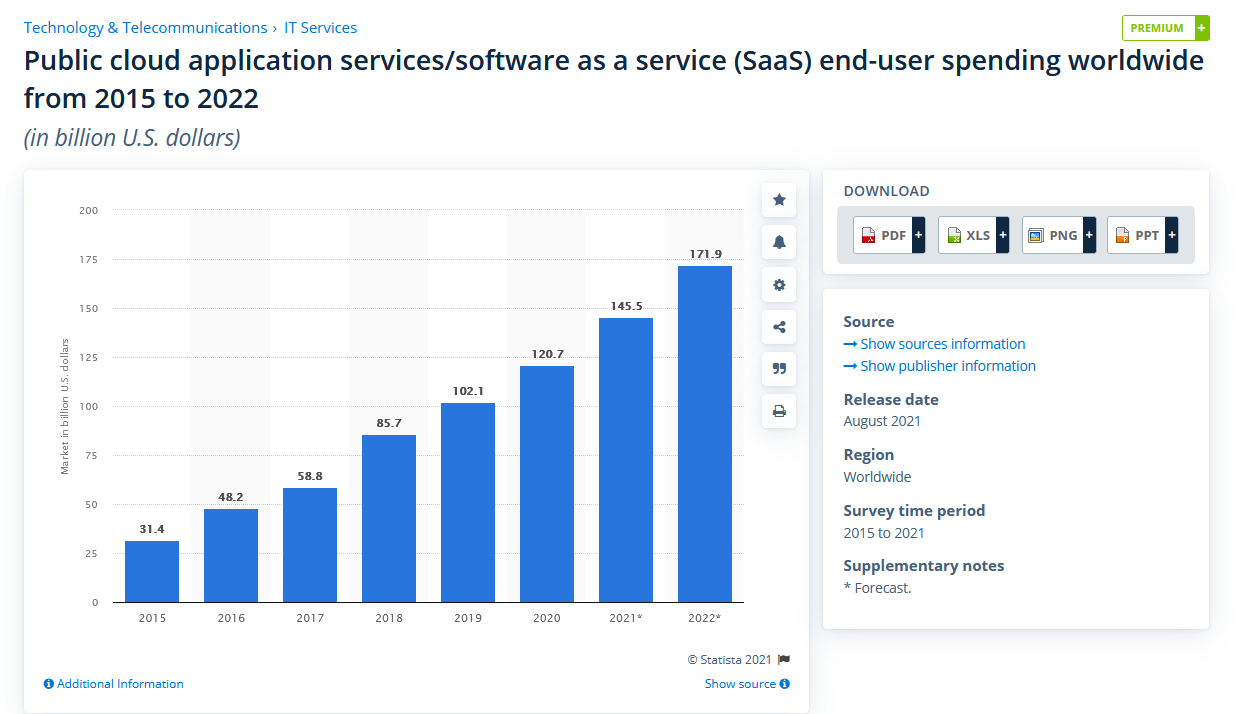

Any company that has forward revenue growth estimate of 34.35% is worth a spot in your long-term portfolios. The subscriptions-based online tutoring/education business is a category under SaaS. Think outside the box. Chegg is worthy growth stock. It is a fast-growing firm engaged in the $145.5 billion SaaS industry. The SaaS market touts a 21.20% CAGR.

(Source: Statista Premium)

Conclusion

Chegg is an American online/distance-learning growth stock you should consider buying. It is not exposed to Chinese government's crackdown on China-based online education companies.

Chegg has $2.06 billion in total cash. It can spend some of this to aggressively promote Thinkful.com. Going forward, Thinkful could replicate the 40 million-strong user count of Udemy.com. Two-thirds of that are from outside the U.S.

A laser-focus on subscription-only online learning could help CHGG improve on its Q2 EPS of $0.43.