Paul Morigi/Getty Images Entertainment

TJX Companies (NYSE:NYSE:TJX) claims the title of leading off-price apparel and home fashions retailer in the U.S. and worldwide. The company sells name brand and designer merchandise at low prices, and it is the largest retailer that does so. TJX is a sizeable company, and it was listed at number 80 on the Fortune 500 list for 2020.

While TJX’s strength comes a lot from its impressive brick-and-mortar presence, it was among those industries that were affected harshly during the worst of the pandemic for the same reason. Like so many true leaders, however, TJX made the appropriate adjustments and put the company’s long-term financial health in high priority. TJX is poised to maintain and strengthen its leadership position, even with some remaining challenges. I see TJX as fairly valued today, and I am targeting a 12-month price of $98.40.

Source for image, data, and information: TJX

The Company

It’s not too uncommon to hear that one company has recruited some great talent from another. Sometimes that turns out to be a great move for the acquiring company, and perhaps a huge loss for the other company. What is less common is for the leadership of that talent to be so successful that eventually their new company acquires the original company that they worked for.

That appears to be the case at TJX. In 1976, Zayre Corporation had a vision for a new off-price retail store chain, and was able to lure away Bernard Cammarata, the then General Merchandising Manager of Marshalls. Cammarata opened the first T.J. Maxx store and later spun off other operations. The TJX Companies were born from the former Zayre Corporation spinoffs and TJX grew its business by opening stores, acquiring others, and becoming a large international retailer. By 1995 TJX acquired Marshalls, the company that Cammarata had been sourced away from, and when T.J. Maxx combined with Marshalls it nearly doubled TJX’s U.S. store presence. Talk about a key strategic recruitment effort!

At most recent reports, TJX operates over 4600 stores in nine countries including the U.S., Canada, Europe, and Australia, and four e-commerce sites all together employing over 320,000 associates. The company recognizes four main segments that are identified as Marmaxx, Homegoods, TJX Canada, and TJX International. Each store and region provides various types of merchandise such as apparel, footwear, home goods, furniture, and outdoor gear.

Source: TJX

Strategy

As mentioned, TJX business strategy includes offering brand name and designer merchandise at low prices. TJX products are generally sold at 20% to 60% off of what full-price retailers charge. TJX’s discounts are not special pricing, they are “every-day” prices. TJX uses what it calls a “treasure hunt” shopping experience. Interesting new products are brought in frequently and are not held long. The idea is to create a sense of excitement for customers to find new products, and an urgency where the customer apparently feels the need to purchase an item while they can. This is designed to create a desire to return to the store frequently so as not to miss out on the latest offerings. Computer-driven inventory management is used to support that by turning over products quickly, using an intelligent markdown strategy.

TJX has a flexible business model, where floor space is fluid. Various departments can be expanded or contracted easily to meet current product focuses. TJX uses a robust buying strategy where they review products from numerous sources, from over 100 countries worldwide, and from 21,000 vendors. This allows TJX to find the products they believe customers will want, and to procure those items at the pricing needed to offer higher quality goods at a discount.

Competition and Growth Potential

TJX is in a highly competitive industry, with numerous differentiating factors such as price, brands, style, quality, selection, and store location. Competitors also come in many forms such as traditional retailers, warehouses, outlet stores, and online retailers. A few well-known retailers that are more closely similar to TJX in price and products are Ross (NAS:ROST), Burlington (NYSE:BURL), Big Lots (NYSE:BIG), Kirkland’s (NAS:KIRK), and Bed Bath & Beyond (NAS:BBBY). TJX competes with international companies in the markets where they coexist as well.

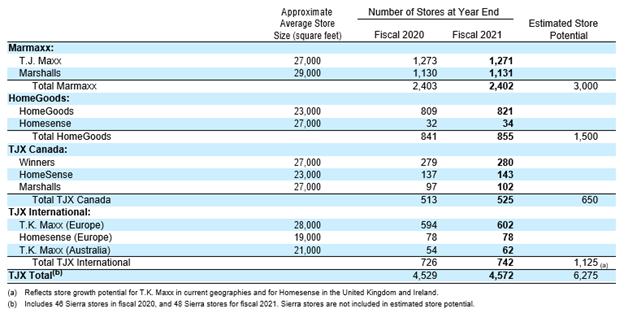

Although TJX is the largest off-price retailer the company still sees ample room for growth. While some retailers were desperately trying to hold on to stores during the pandemic, or, were even closing a good number of stores, TJX continued to increase its footprint. The image below, with notation that combo (superstore) locations are counted separately, shows significant store growth from FY20 to FY21 with 43 new locations.

Source: TJX

The trend continues, as TJX recently reported a total of 4,665 stores, which means another 93 stores have been added already with FY22 only a little over half the way in. Furthermore, the image also provides store potential estimates for current geographies. This indicates potentially another 25% in store growth alone, and not including any additional geographic areas. I add as an assumption, it may not include any possible future acquisition activity as well.

In e-commerce, some of the TJX sites have been in operation longer than others, but it’s worth noting that the Homegoods e-commerce site has just recently been launched. This can be another substantial contributor to revenue that has not shown in revenue on any prior reports. Also, the existing e-commerce sites may grow on their own as well.

Source: TJX

Valuation

TJX has seen much better conditions and revenue gains since the hardest days of the pandemic. Q2 of FY22 saw an increase of 23% in sales of the pre-pandemic sales of FY20. EPS for FY22 was actually much stronger than it first appears. EPS was $.64 for Q2 FY22 versus $.62 for Q2 of FY20. However when you factor in a debt extinguishment charge of $.15, and factor in approximately $.06 for sales lost at some pandemic-related temporary store closures in international locations then EPS “could” have been $.85.

Currently, there is worldwide concern about availability of inventory and freight costs. TJX states that as of Q2 FY22 the increase in revenue and margin increases more than offset additional freight costs. TJX sees overall product availability to be “excellent” and the company is positioned to provide merchandise throughout the fall season.

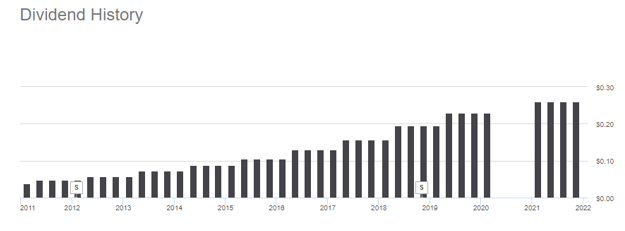

The company sees improving financials, as they were able to reduce outstanding debt by $2.75 billion in FY22, reducing annualized interest expenses by more than $90 million. TJX reinstated its stock repurchase plan early in FY22 and they have since increased the projected repurchase amount to between $1.25 billion to $1.5 billion in stock. Likewise, the annual dividend that was suspended during the pandemic has been reinstated at $.26. The dividend has grown from pre-pandemic levels and it appears to be set to continue a path of continued growth.

Source: Seeking Alpha

At a current TTM P/E of approximately 30, TJX may seem to be about fairly priced, but that is based on $2.04 TTM EPS. Actual EPS for the first half of FY22 is $1.09. With the adjustments mentioned above FY22 first half EPS could have been $1.30. ($2.60 annualized) FY20 (pre-pandemic) diluted EPS was $2.67. Total guesswork, but I’ll assume a 23% increase and project a forward EPS of $3.28. (2.67*1.23). That reflects the actual 23% increase in sales as of last quarter and roughly the performance improvement it could have achieved. (.62 Q2 FY20 to .85 = 27% increase, which is somewhat close to .23, erring on the conservative side).

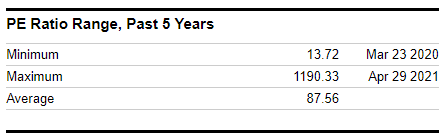

At a current P/E of 30 and a presumed forward P/E of 3.28 you might see a share price of $98.40. I will call the current share price fairly valued at today’s price, considering all the uncertainty in the overall industry at this time. But I also believe a 12-month target price is very reasonable at $98.40. Certainly, factors could deny this price, but I believe it is conservative. The figure does not consider much more for the growth that new stores may bring, or for growth from e-commerce. It also does not consider the potential increase for typical seasonality gains. Further, the 5-year average P/E for TJX is actually 87.56, indicating that TJX is typically rewarded very well for performance, at a much higher P/E than what I used.

Source: YCharts

Risks

TJX includes a full rundown of risks in their FY2021 annual statement. I recommend a full read there, but I recognize the shipping issues the world is facing at this time and the possibility of extended periods of inflation. Among all other factors, these risks could eventually hinder TJX, and any of its competitors, from achieving results as they, or as we may hope to see.

Also, the pandemic continues to affect the industry in general, and there is no way of knowing if that will end soon, or instead may worsen and negatively affect EPS potentials.

Final Thoughts

Various industries were affected differently during the pandemic. Companies that provided essentials such as food, or cleaning supplies may not have been affected as harshly by the pandemic, and maybe never had to miss a dividend. Companies like TJX saw an immediate effect, however, as customers were unable to enter their stores for some time.

No investor wants to see a dividend cut, but TJX took that measure, among others right as it was needed. To their credit, it only lasted three quarters until they were able to reinstate it, along with the share repurchase program, and they also were able to do some debt clean-up.

The market took its wrath on any sign of weakness, and the current P/E for TJX is less than half the 5-year average. But I believe the turnaround is in full motion. Shareholder equity is better than ever and TJX is confident that its cash flow is strong, and that growth initiatives can be readily funded. The company has stated a long-term vision of reaching $60 billion in sales. At a little over $32 billion in sales for FY21, TJX has lots of room to grow, per their own guidance. If past results are an indication, shareholders may have many more years to add value to their portfolio fueled by growth from TJX. That is, in assuming that the market realizes this is the same great company it always was, and that TJX has some time to show that.