Kwangmoozaa/iStock via Getty Images

Introduction

It's been more than six months since I last discussed Ardagh Metal Packaging (NYSE:AMBP). Back in March, one of the Gores SPACs announced its intention to acquire the beverage can business from the Ardagh Group as its qualifying transaction. This piqued my interest as it's general knowledge the demand for aluminum cans continues to increase and competitor Ball (BLL) has mentioned it expects the demand growth to continue all the way into 2025. Not only was Ardagh already a respectable producer of those cans behind Ball and Crown Holdings, it was also heavily investing in growth as it wants to maintain or perhaps even grow its market share.

The third quarter was once again strong, and the company continues to invest in growth

Ardagh Metal Packaging reported a net loss in the third quarter. That's perhaps shocking to see for people who aren't familiar with the company. But in this article, I will explain why the company is still doing well on an underlying basis, and why it remains my top pick in the beverage can industry.

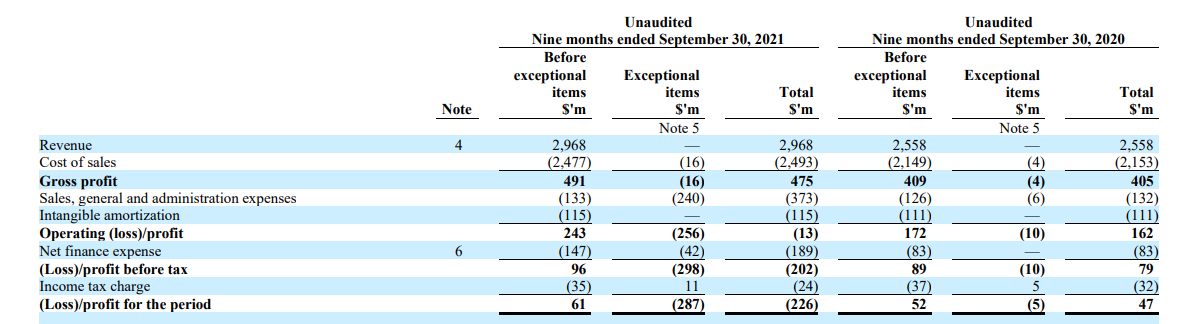

The company reported a total revenue of $1.04B in the third quarter, which allowed it to generate approximately $150M in gross profit. This gross profit included about $8M of exceptional charges, and the entire third quarter was actually dominated by exceptional charges. As you can see on the image below, AMBP reported an operating loss to the tune of $146M. That may sound very surprising considering the beverage can industry has a lot of wind in its sails.

Source: financial results

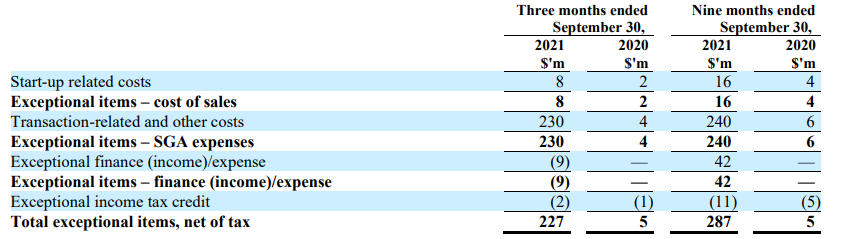

However, you can see in the image above there's an exceptional item to the tune of $230M in the SG&A expense category. That really undermined the company's financial performance and was the sole reason why the operating profit from last year was converted into an operating loss. Excluding the exceptional items in both years, the operating income would have been about $71M in Q3 2020 and a very respectable $92M in the third quarter of this year, which would be an increase of about 30%. And as you can see below, the vast majority of the exceptional items is related to the going public transaction of Ardagh. So it truly is an exceptional item which should not re-occur in the next few quarters and years.

Source: financial results

The net finance expenses also increased in 2021 as the company issued debt to pay the acquisition fee to the Ardagh Group and to raise the cash needed for its aggressive expansion plans. The reported net income was a net loss of $178M in the third quarter, but excluding all the exceptional items, Ardagh would have posted a net income of about $49M.

That's a decent, but definitely not great, result. We do need to cut the company some slack though, and I was mainly interested to see how much of the reported profits were actually converted into free cash flow.

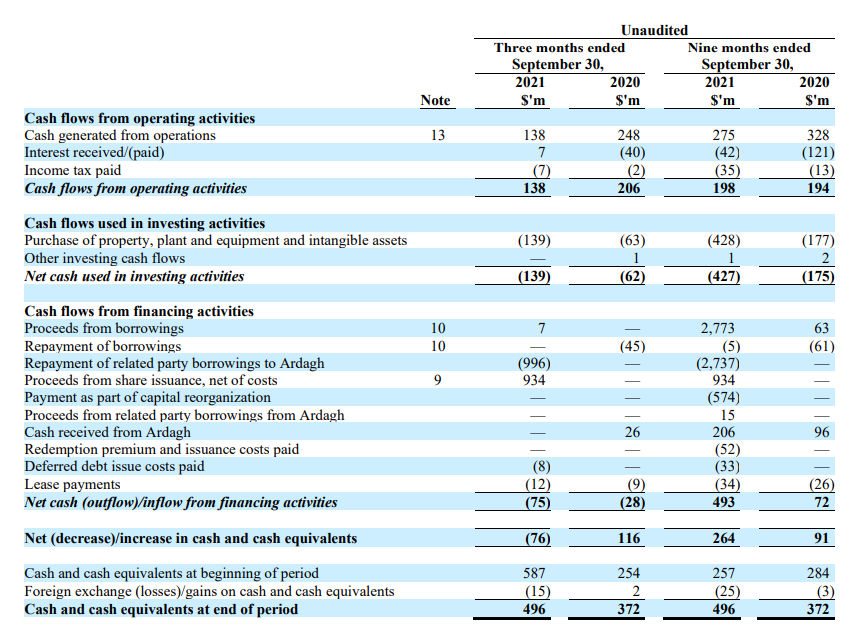

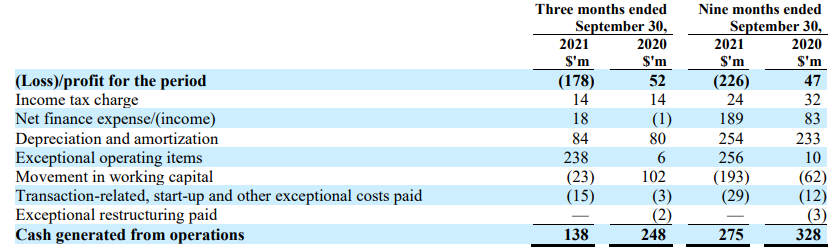

Source: financial results

The cash flow statement above shows the 'cash generated from operations' as starting point. However, this already includes all the changes in the working capital position, and as you can see in the image below, the $138M in cash generated from operations includes about $23M in changes in the working capital position as well as $15M in transaction related expenses. This means that on a normalized basis, the $138M in cash generated from operations would be approximately $176M.

Source: financial results

So I think it's fair to use the $176M, and subsequently deduct the $16M in taxes that would have been due on the result before exceptional items, while we should also deduct the $12M in lease payments. This means the underlying operating cash flow in the third quarter of the year was approximately $148M.

While this was barely sufficient to cover the $139M in capex, keep in mind Ardagh is heavily investing in its future and several new manufacturing plants are currently under construction. As you could see in one of the previous images, the total depreciation and amortization expenses in the third quarter were just about $84M, so it is clear the AMBP capex is much higher than the depreciation expenses. The investment in production capacity is not a surprise, as this was a key element in my March article as I enjoyed Ardagh's aggressive growth plans, which would predominantly be funded by the internally generated free cash flow.

Investment thesis

I currently have a long position in Ardagh Metal Packaging, and am continuing to write put options at various strike prices and expiry dates as I would like to obtain an overweight position in this name. The demand for aluminum beverage cans continues to increase and as you could read in my previous article, Ardagh is a top-3 player in the world and will for sure benefit from the higher demand.

I will continue to build my position in the foreseeable future while I will also write additional put options.

Consider joining European Small-Cap Ideas to gain exclusive access to actionable research on appealing Europe-focused investment opportunities, and to the real-time chat function to discuss ideas with similar-minded investors!

NEW at ESCI: A dedicated EUROPEAN REIT PORTFOLIO!