fcscafeine/iStock via Getty Images

I began writing this article on Thursday morning, with absolutely no idea how the markets were going to end up by the closing bell.

I'm the first person to admit I don't have a crystal ball. But I'll use my December 2 blog post to help explain why that doesn't matter:

"For a while there yesterday, the major indices looked like they would take back a good chunk of Tuesday's losses. Maybe they'd even advance beyond that dip altogether, making it a mere blip in a continuing bull market!

"But that just wasn't meant to be."

Judging by the comments that post received, different people have different opinions about what the real contributing factor in stocks' ultimate slide was. But it basically boils down to two factors:

- CNN reported the CDC's news that the U.S. had its first known case of Covid 19's Omicron variant.

- Federal Reserve Chief Jerome Powell told the Senate Banking Committee that he might ramp up existent tapering plans. "We're now looking at an economy that's very strong and inflationary pressures that are high." As such, it might be "appropriate to wrap up our purchases a few months earlier" than previously announced.

I write those morning blogs to inform investors about what's going on with the real estate investment trusts. And since REITs are part of the larger market, I spend most of my time explaining what's going on elsewhere as well.

Which leads me back to "What Really Happened Yesterday."

The Fickle, Fickle Mr. Market

In case it wasn't clear, "What Really Happened Yesterday" was Thursday morning's blog post title, which included this bit:

"Just like that, people were panicking over shutdown possibilities.

"Yet before you panic too, stop and really think about it.

"Like how Mr. Market knew full well on Monday - when stocks climbed nicely after Friday's significant selloff - and again on Wednesday morning that Omicron would hit the U.S. soon enough.

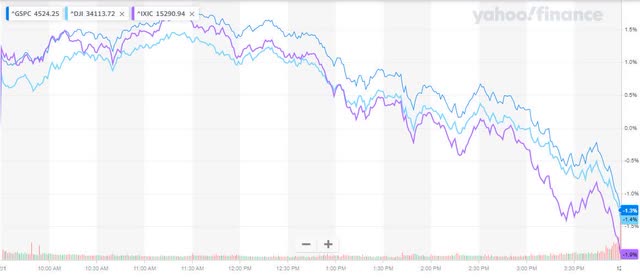

"He's not stupid. Just reactionary. Hence the December 1 chart below of the S&P 500 (dark blue), Dow (bright blue), and Nasdaq (purple)."

(Source: Yahoo Finance)

That contributed to a seven-day chart (November 23 through December 1) that looked like this:

(Source: Yahoo Finance)

Clearly then, Mr. Market jumped right from bullish to bearish to bullish to bearish to bullish to bearish - in a very short amount of time.

For some people, that was too much, which I understand. Any negative market activity can far too easily have a chilling effect on one's investing enthusiasm. And throwing in choppy upward movement can actually make those concerns more pronounced.

But when you're a fundamentals-focused individual, you're much more easily capable of moving past such fears.

You're not interested in market timing (because you know it's impossible to implement as a strategy anyway). You're not fixated on what everyone else is doing.

You know which stocks are sound. You know which have a place in your portfolio based on proper diversification, asset allocation, and your personal situation. And you know your entry price points: when to buy which shares based on fair or discounted valuation.

You really don't need anything else along the way.

3 Insanely Cheap REITs

That's not to say I don't sometimes wish I could market time. If I'd just gotten to writing this article sooner, I could have recommended even better prices…

But that's not how it works. Not for me. Not for you. And none of us can act on every awesome opportunity that comes our way.

We're limited creatures like that.

On the plus side, there are always prospects worth pursuing. As my associate Dividend Sensei likes to say, the stock market is a market of stocks. So no matter how over-elevated the indexes become, there will always be quality companies trading at reasonable or better valuations.

In the case of REITs like the ones below, we get a bonus. Their valuations are very likely to grow in size and matching price from here, AND we get the benefit of dividends as they do.

Dividends that should keep coming no matter if Mr. Market is quickly climbing like it ended up doing on Thursday… or plunging like it did on Friday, November 26.

To me, that's something worth investing in. And I think if you set both fear and greed aside for the fundamentals, you'll probably find it's true for you too.

(Source)

So today, I'm providing you with three Strong Buy REITs that are shockingly cheap - and with expanding moats. In the words of Guy Spier, author of The Education of a Value Investor:

"There are plenty of reckless investors with scant regard for the risk of loss. But they tend not to survive very long in the investing game. The long-term survivors possess a more sophisticated grasp of risk, including the ability to see when the situation is less risky than the stock price might suggest."

With that in mind, let's evaluate the risk already… and the rewards.

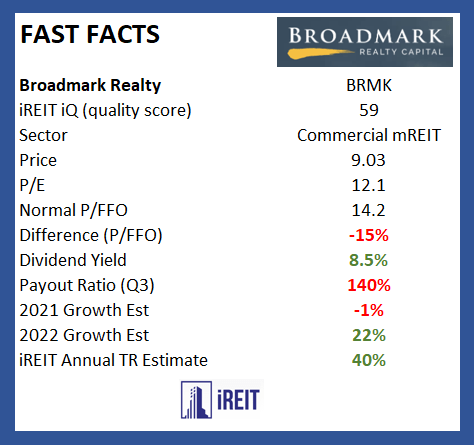

Broadmark Realty Shouldn't Be In The Bargain Bin

Our first insanely cheap REIT is Broadmark Realty (BRMK). This commercial mortgage REIT invests in senior secured construction loans designed for vertical construction of projects such as:

- Multi-family housing

- Single-family housing

- Commercial, office, and industrial buildings.

Weighted toward residential housing, BRMK is one of the fastest-growing lenders in the U.S. The company has an active loan portfolio that includes 217 loans across 17 states, plus D.C. And it targets states with favorable demographic trends and lending laws.

Over a 10-year period, it's maintained minimal principal losses with approximately 0.2% on $3.4 billion loans originated. During and subsequent to Q3-2, BRMK foreclosed on two loans and received total pay offs on seven in default.

The total commitment was $50.5 million.

Within the current default population, 55% of its loans have construction complete or nearly complete. And 64% are collateralized by residential properties, giving confidence in its resolution capabilities.

The weighted average loan-to-value is approximately 89% for loans in default as a result of cost-overruns and collectible receivables.

In a recent article, Wolf Report points out:

"Defaults are part of their operations. The sorts of loans the company [give] are not risk-free, as should be indicated by the returns and yield you may get. Part of what you have to decide is if you trust the company and management's ability to handle exactly these sorts of events."

As such, defaults are expected. It's just a matter of how they handle them. "And, as of yet, [it's] proven very capable of doing just that."

I've interviewed BRMK CEO Jeff Pyatt on iREIT on Alpha at least six times now. In the latest one, he related the case of a Portland borrower last quarter with about $40 million on the line.

It's worth sharing here too…

Broadmark Saves Its Own Day

There were three pieces of collateral, including a partially finished office building and an apartment building. Broadmark couldn't foreclose on the former for a while under Oregon's extended moratorium.

Plus, it was "right in the center of where all of Portland's riots" were. So "finding tenants was just about impossible." Yet:

"We were paid off in full, had no loss of principle, and… I'm going to call it a victory. And certainly it proved out our business model. We were proud of the outcome, and it was a tough one."

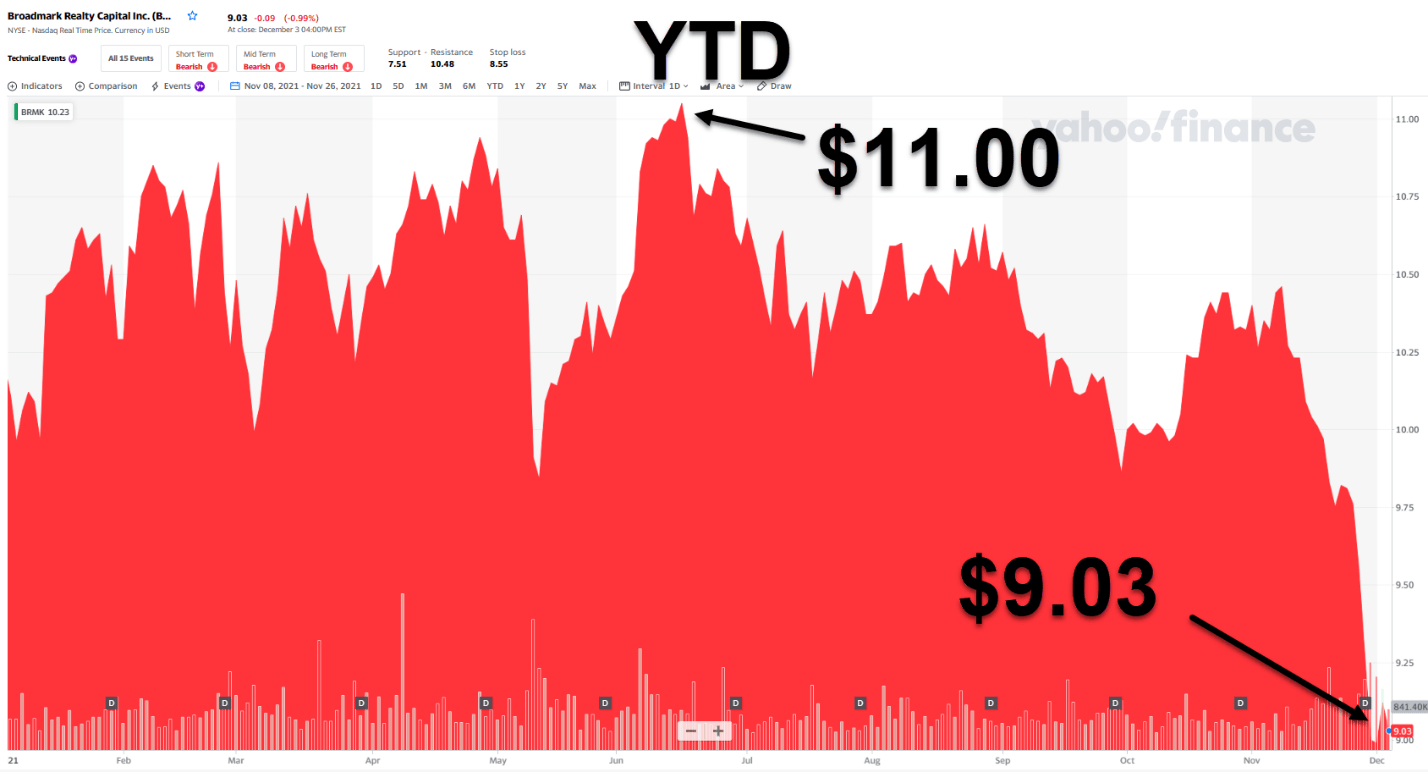

(Source: Yahoo Finance)

As viewed above, BRMK is now trading at $9.03 with a 12.1x price-to-earnings multiple. Over the last two years, its P/E has averaged 14/2x.

The dividend yield, meanwhile, is now 9.3%. So the primary reason for the mispricing is a potential dividend cut.

Pyatt recently said that, as the year winds down, he's "seeing sustained and robust demand in the nation's housing market." That and a "healthy pipeline" of new housing product.

Better yet, BRMK is "well-capitalized" to "help [borrowers] see their business plans through to completion."

The Commercial Observer said that the company:

"… provided $25.7 million in debt to a private investor to refinance existing debt and fund remaining construction work on Alura Vail, a 10-unit townhome project in Vail, Colorado.

"The roughly 35,000-square-foot townhome development will be situated on more than an acre of land at 1488 Matterhorn Circle in Vail, one of the country's most visited mountain destinations…"

(Source)

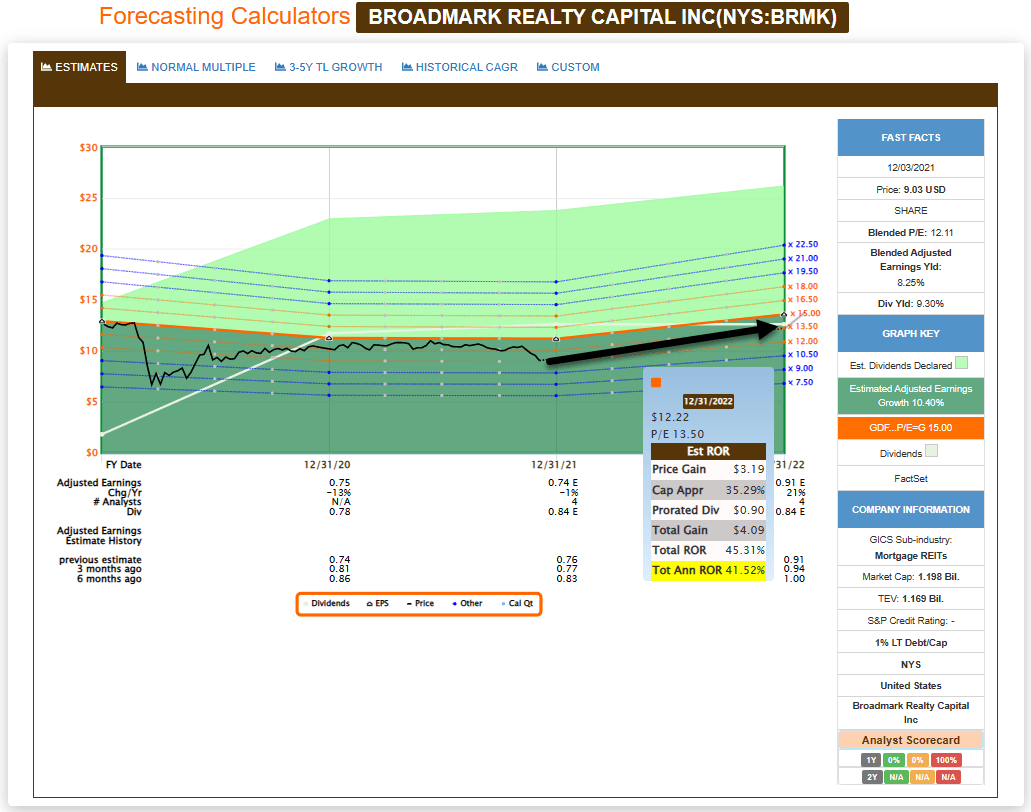

We consider BRMK a Strong Buy based on its strong pipeline. And analysts expect earnings to grow by over 20% in 2022.

If that projection holds up, the dividend should too.

We'll be watching BRMK closely and staying in close contact with management. Our 12-month total return forecast is 40%.

(Source: FAST Graphs)

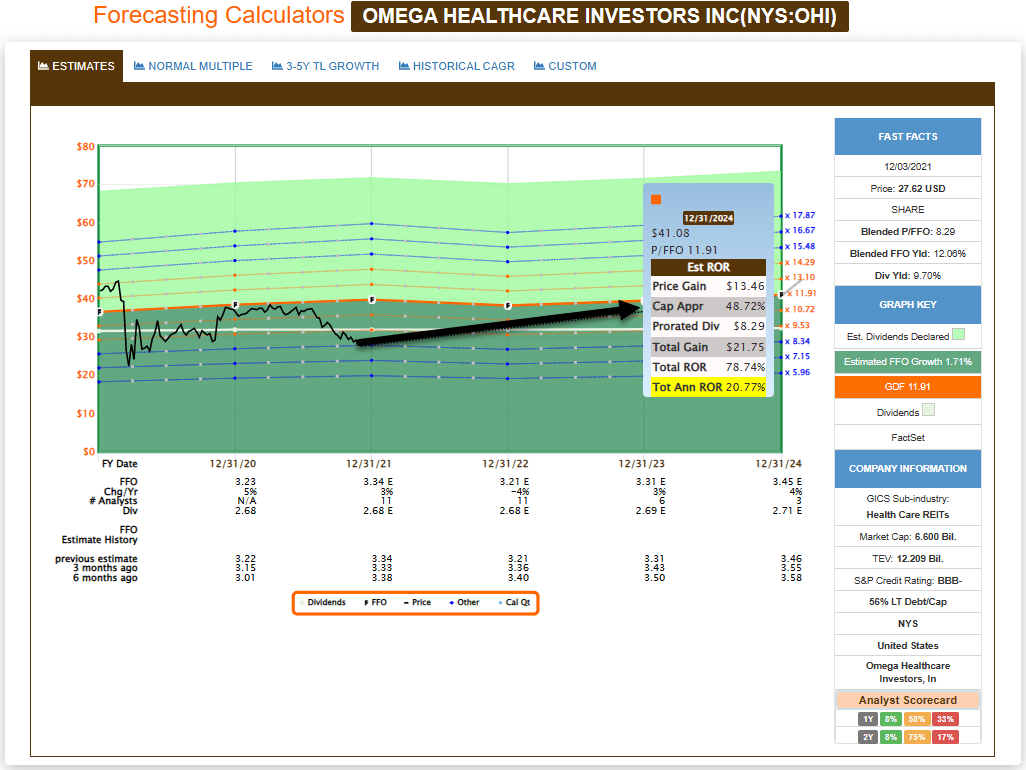

Omega Is Hardly Our Last REIT Pick On The List

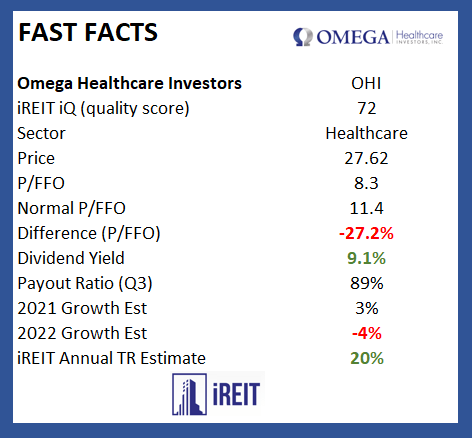

Our next insanely cheap REIT is Omega Healthcare Investors (OHI). It owns 944 properties with 96,000+ beds across the U.S. and U.K., diversified further by 63 operators.

OHI is the largest skilled nursing REIT, and we believe scale has its advantages. Its long lease contracts and limited supply provide solid earnings dependability.

Its certified facilities and beds have remained steady for many years, with no net new supply.

Of course, Covid-19 has put a strain on many skilled nursing operators. Yet government financial support continues to be both sufficient and timely.

Skilled nursing facilities still fulfill an essential need within the healthcare continuum. And secular tailwinds with improving demographics remain in place.

In a recent interview, CEO Taylor Pickett pointed out:

"… this is a labor-intensive business, and [the shutdowns] hit us on two ends. One is the cost side, but… just as importantly, without appropriate staffing, a number of facilities in the industry have put themselves on self-imposed admission bans.

"So even though they might have the opportunity to take more residents, they can't because they can't staff at the levels they need to staff. So it's mixed. Things are rebounding. The operators have stabilized care delivery, but occupancy and labor are going to be big battles and government support's going to be important."

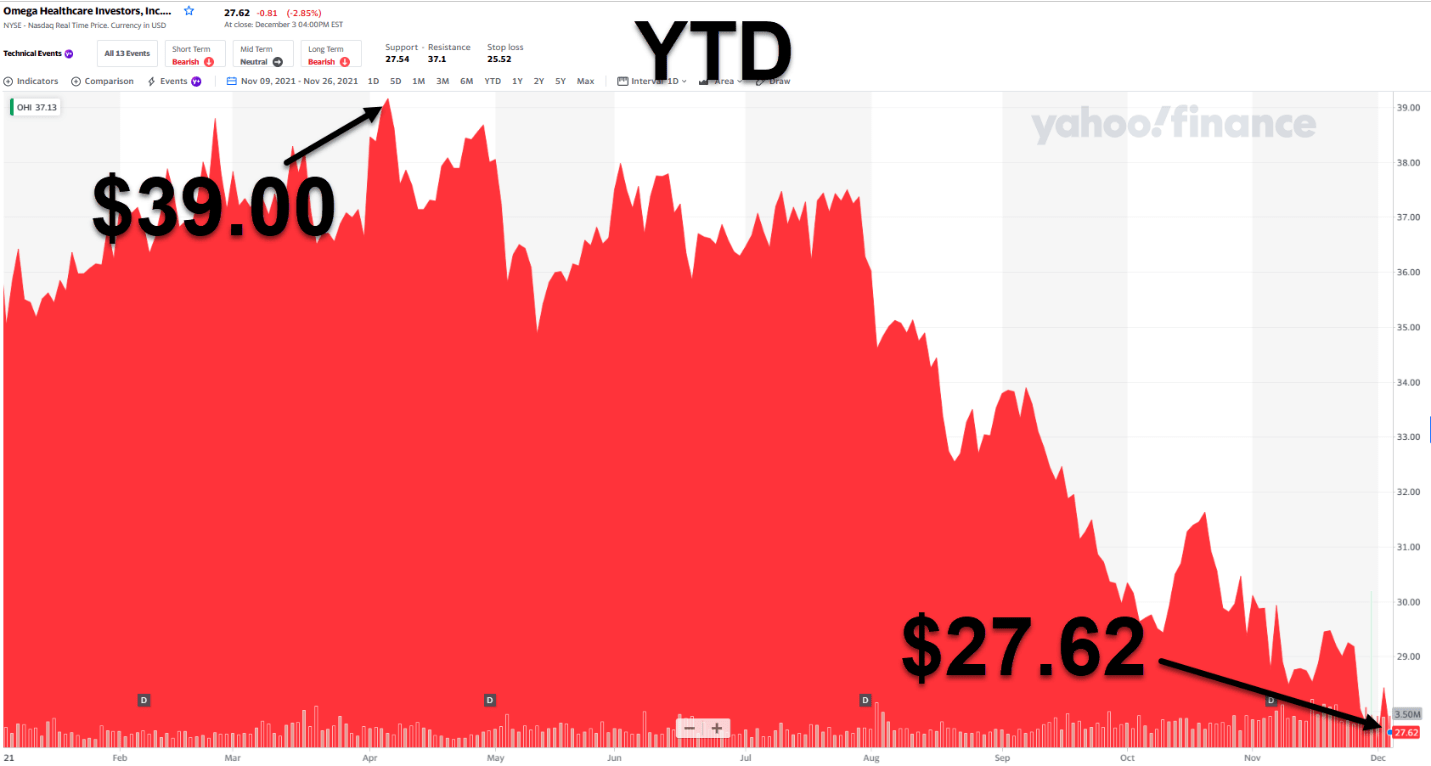

(Source: Yahoo Finance)

As you can see above, OHI is currently dirt cheap, with shares trading at $27.62. Its dividend yield is 9.70%, showing further fear of a dividend cut.

That's understandable given how its payout ratio - based on adjusted funds from operations (AFFO) models by REIT Base - was 88.5% as of Q3-21. Even so…

That's Not The End To Omega Healthcare's Story

Keep in mind other REITs like Medical Properties Trust (MPW) - with its 91% payout ratio - and Physicians Realty (DOC) at 95%. Both have higher AFFO-based payout ratios. OHI also has several operators that are in the "work-out" mode.

Pickett told me he's comfortable with his company's $0.67 per share. "The only reason" he'd ever look at reducing it would be if there were "years-long issues within the portfolio that are permanent or semi-permanent."

"And as we sit here today, we don't think that's where the business is. Obviously, facts could change that position. But… I think there's consensus among the board members that if we see Covid playing out the way we think it will - where occupancy returns to pre-Covid levels over some reasonable period of time - that moving the dividend around wouldn't make sense."

Thus, we're maintaining a Strong Buy, recognizing that there will be more volatility over the coming quarters. We believe in the business model… and the so-called "silver tsunami" in which aging Baby Boomers are expected to drive a multi-decade increase in demand.

We're talking about a 44% projected increase in adults aged 65+ in the next 20 years. Knowing that, our 12-month total return forecast is 20%.

(Source: FAST Graphs)

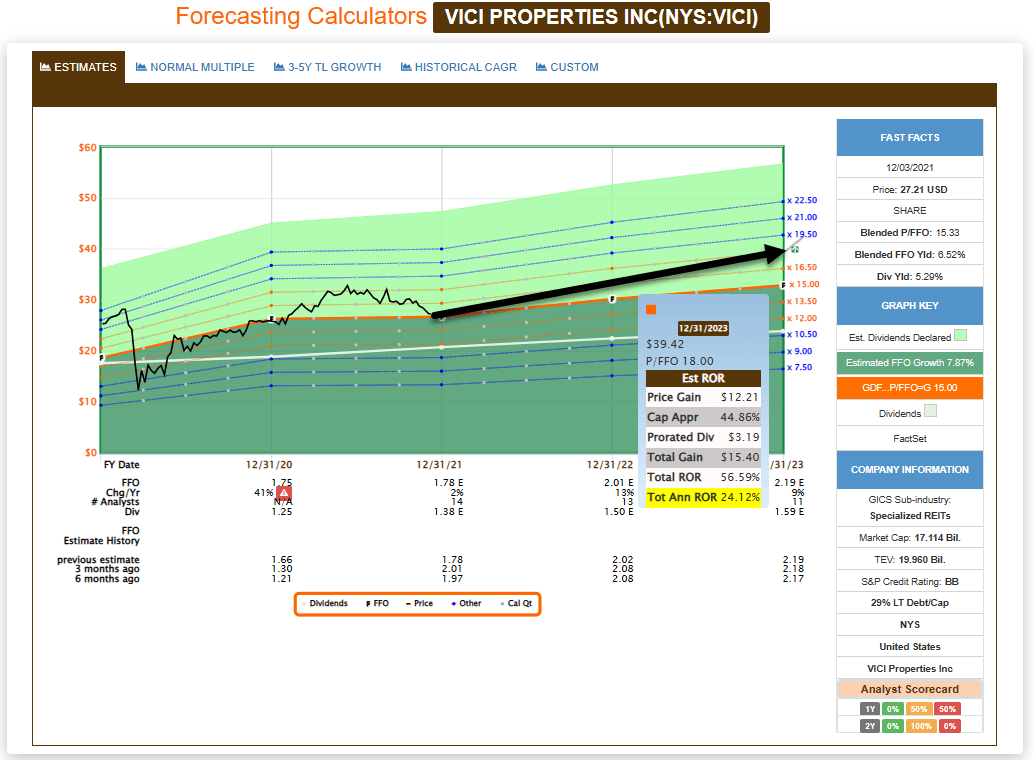

VICI Isn't Done Conquering Yet

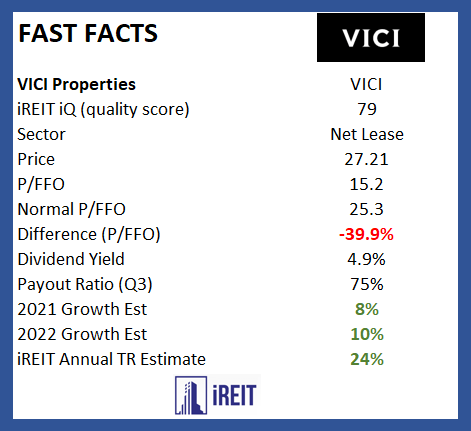

Our final "insanely cheap" REIT is VICI Properties (VICI). A net-lease "gaming" REIT, it announced earlier this year that it's acquiring MGM Growth Properties (MGP) for approximately $17.2 billion.

That includes stock, cash distributed to MGM, and $5.7 billion of debt.

MGM has a leading presence in Las Vegas and global brand recognition that includes a diversified mix of U.S. regional, Las Vegas, and Macau properties across multiple customer segments. And its financial profile will certainly be enhanced with the VICI deal… where its liquidity will grow from $5.6 billion to more than $9 billion.

This megamerger should close in the first half of 2022 and be immediately accretive to AFFO per share upon closing - with minimal need to increase VICI's standalone general and administrative (G&A) expenses.

VICI's CEO, Ed Pitoniak, told me:

"Over the course of 2021, we've raised $5.5 billion of equity. Which, as you know… equals a market cap of a lot of REITs.

"But all of that equity is sufficient to fund the closing of both the Venetian and MGP again. And that's an important point to stress, as you point out, that we have raised all the equity for MGP. We will, upon closing, need to raise a certain amount of debt to finalize the funding of the transaction, but all the equity is raised."

Pitoniak also pointed out that VICI is "in very close contact with S&P, Fitch, and Moody's" to "educate them on what we're about to do." He even suggested that a credit upgrade may be "in the cards" - pun intended - as it puts VICI "in a position where it meets the qualifying criteria that S&P spoke of."

iREIT's Final Thoughts On VICI's Current - Growing - Potential

VICI cannot "predict with any accuracy when exactly S&P would be inclined to move VICI to investment grade," he admitted. But "upon closing [on MGP] and upon evidence that VICI has achieve" leverage below 6x, it "could move quickly."

(Source: Yahoo Finance)

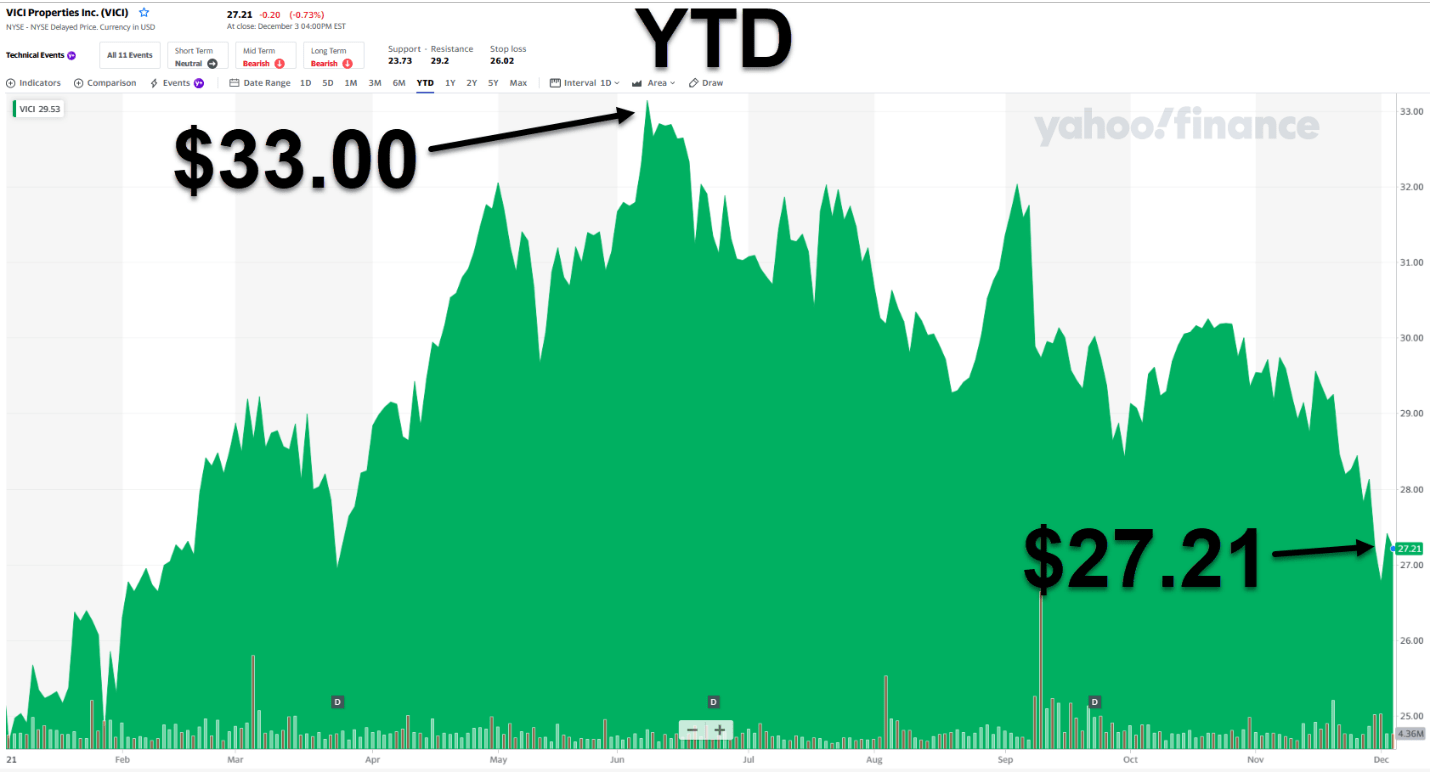

We find it fascinating that VICI has sold off by over 16% since June despite it signaling many catalysts that should spark a 2022 liftoff. For some reason, the shorts (at about 12%) aren't as excited as we are.

But of course, that means we can take advantage of the mispricing and gobble up even more shares.

Analysts are forecasting AFFO per share to grow by 10% in 2021 and 8% in 2022. And, honestly, I'm not too concerned with inflation fears given how VICI has CPI-adjusted lease contracts and a modest payout ratio of about 74%.

Shares are now trading at $27.21 with a p/AFFO of 15.3x and a dividend yield of 5.3%. Remember:

- Interest rates go up, REITs go down

- Interest rates go down, REITs go down.

So ignore Mr. Market and stay laser-focused on fundamentals. Our 12-month total return forecast is 24%.

(Source: FAST Graphs)

In Conclusion…

In his classic book, The Intelligent Investor, Ben Graham wonders how to sum up sound investing into a single phrase. In response to the self-directed challenge, he writes three words all in caps:

"MARGIN OF SAFETY."

Afterall, it's the margin of safety that's the essence of value investing. It's the metric by which hazardous speculations are segregated from bona fide investment opportunities.

But I'll let Guy Spier sum up this article for us all around.

"If your goal in life is to get rich, value investing is pretty hard to beat."

Happy Holidays! And I hope you enjoy these FAST FACTS provided by iREIT on Alpha:

Please NOTE that there is an error in the Broadmark chart above in that the payout ratio in Q3-21 is 110%, not 140%.

Author's Note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: written and distributed only to assist in research while providing a forum for second-level thinking.

The iREIT BUY ZONE

Join iREIT on Alpha today to get the most in-depth research that includes REITs, mREIT, Preferreds, BDCs, MLPs, ETFs, Banks, and we recently added Prop Tech SPACs to the lineup.

We recently added an all-new Ratings Tracker called iREIT Buy Zone to help members screen for value. Nothing to lose with our FREE 2-week trial.

And this offer includes a 2-Week FREE TRIAL plus my FREE book.