J. Michael Jones/iStock Editorial via Getty Images

Image: Corning optical communications facility

Investment Review: Corning Incorporated

I previously analyzed Corning Incorporated (NYSE:GLW) in my Nov. 04, 2020 article "Corning: Illusory EPS And 'Leaky Equity Bucket' - Avoid." At that time, Corning had reported non-GAAP earnings totaling $5,203 million and paid out dividends of $2,379 million over the 3.75 years to Sep. 30, 2020. Over the same period, the balance sheet showed Corning had gone from a net cash position of $1,384 million to a net debt position of $5,564 million. A large part of this increase in net debt was due to share repurchases in an attempt to boost non-GAAP EPS despite absence of meaningful non-GAAP earnings growth. But $3,757 million of the increase in debt could be fairly attributed to costs and expenses excluded from the non-GAAP earnings calculations. These costs and expenses included large amounts attributed to restructuring. The good news is there have been minimal adjustments in arriving at non-GAAP results for nine months ended Sep. 30, 2021. The bad news, from a balance sheet perspective, is the impact of transactions associated with the redemption of preferred shares in April 2021. The preferred shares had an equity value of $2,300 million and were redeemed on April 8, 2021 (see Q3 2021 10-Q p. 15) by issue of 115 million ordinary shares with a market value of $5,126 million, based on closing share price of $44.57 on the day. Corning entered into an arrangement to buy back 35 million of the newly issued shares from the preferred shareholders for $1,526 million ($43.60 per share). Of the $1,526 million, $507 million was immediately payable with further installments of $504 million due April 8, 2022, and $515 million due April 8, 2023. These payments can be expected to further increase Corning's net debt in due course. Having painted this pessimistic picture of the past, it's possible Corning has its restructuring issues behind it and 2021 earnings are showing likelihood of achieving pre-pandemic levels. As other authors have pointed out (see here, and here), some of Corning's products could have a good runway of growth in the years ahead. Barring the unexpected, based on my usual detailed structured financial analysis further below, Corning has the possibility of providing high single to double digit returns, buying at current share price and holding through end of 2023. First, some brief details of Corning's business operations.

Corning: Business

From the company's Q3 2021 10-Q filing,

Corning operates in five reportable segments: Display Technologies, Optical Communications, Environmental Technologies, Specialty Materials and Life Sciences, and manufactures products at 122 plants in 15 countries.

- Display Technologies - manufactures glass substrates for flat panel liquid crystal displays and other high-performance display panels.

- Optical Communications - manufactures carrier network and enterprise network components for the telecommunications industry.

- Specialty Materials - manufactures products that provide more than 150 material formulations for glass, glass ceramics and fluoride crystals to meet demand for unique customer needs.

- Environmental Technologies - manufactures ceramic substrates and filters for automotive and diesel applications.

- Life Sciences - manufactures glass and plastic labware, equipment, media, serum and reagents enabling workflow solutions for drug discovery and bioproduction.

Looking for share market mispricing of stocks

What I'm primarily looking for here are instances of share market mispricing of stocks due to distortions to many of the usual statistics used for screening stocks for buy/hold/sell decisions. The usual metrics do not work when the "E" in P/E is distorted by the impact of COVID-19. And if the P/E ratio is suspect, so too then is the PEG ratio similarly affected. I believe the answer is to start with data at the end of 2019, early 2020, pre COVID-19 and compare to projections out to end of 2023, when hopefully the impacts of COVID-19 will have largely dissipated. Summarized in Tables 1, 2, and 3 below are the results of compiling and analyzing the data on this basis.

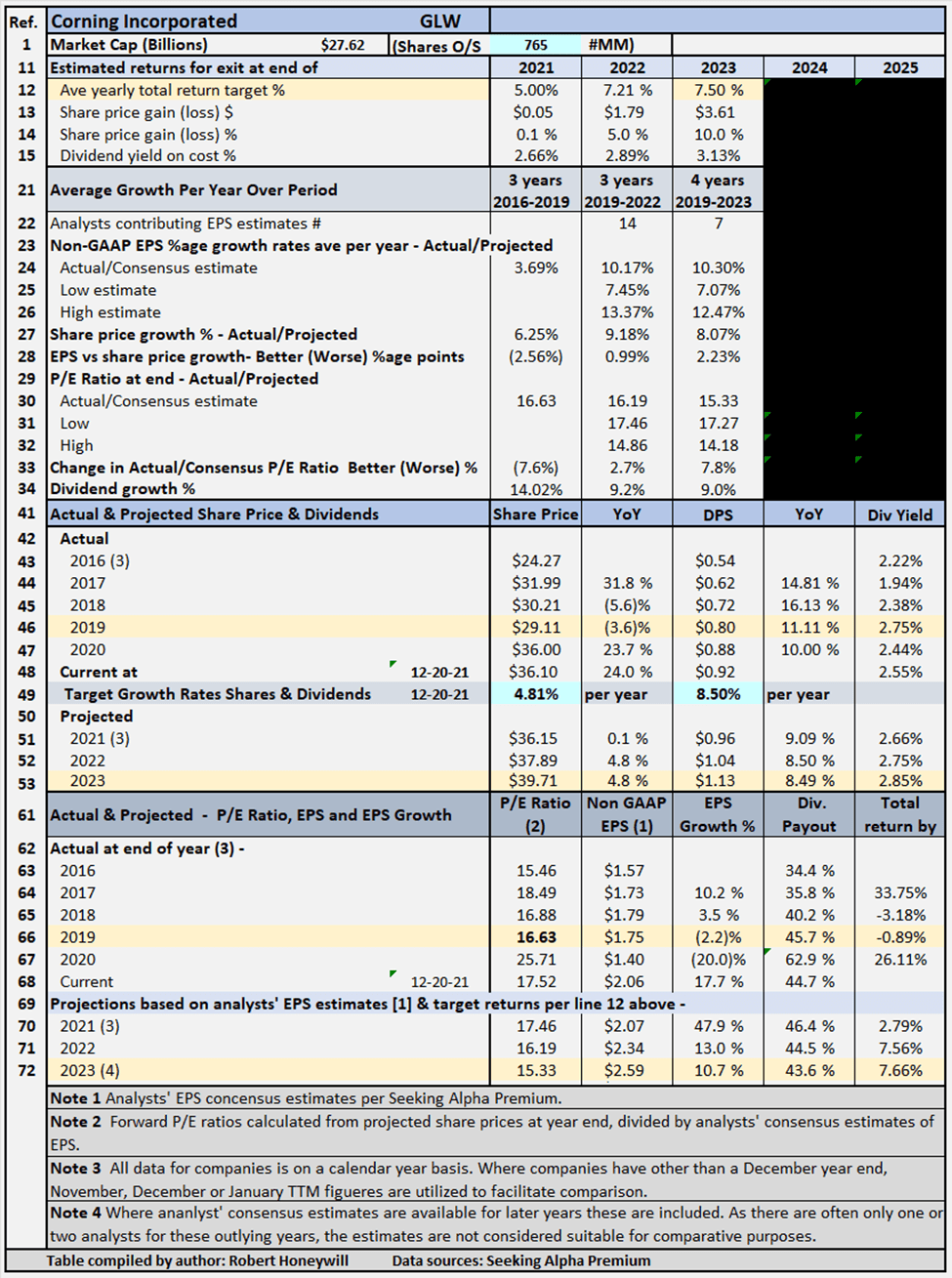

Table 1 Detailed Financial History And Projections

Table 1 documents historical data from 2016 to 2019, including share prices, P/E ratios, EPS and DPS, and EPS and DPS growth rates. The table also includes estimates out to 2023 for share prices, P/E ratios, EPS and DPS and EPS and DPS growth rates (note estimates are shown for analysts EPS estimates out to 2025 where available but these are considered not as reliable). Table 1 allows modeling for target total rates of return. In the case shown above, the target set for total rate of return is 7.5% per year through end of 2023 (see line 12), based on buying at Dec. 20 closing share price level. The table shows, to achieve the 7.5% return, the required average yearly share price growth rate from Dec. 20, 2021, through Dec. 31, 2023, is 4.81% (line 49). This growth rate is lower than the target 7.5% return due to estimated dividends receivable. Corning has a current dividend yield of 2.55% (line 48). Table 2 below summarizes relevant data flowing from the assumption of a target 7.5% total return.

Targeting A 7.5% Return

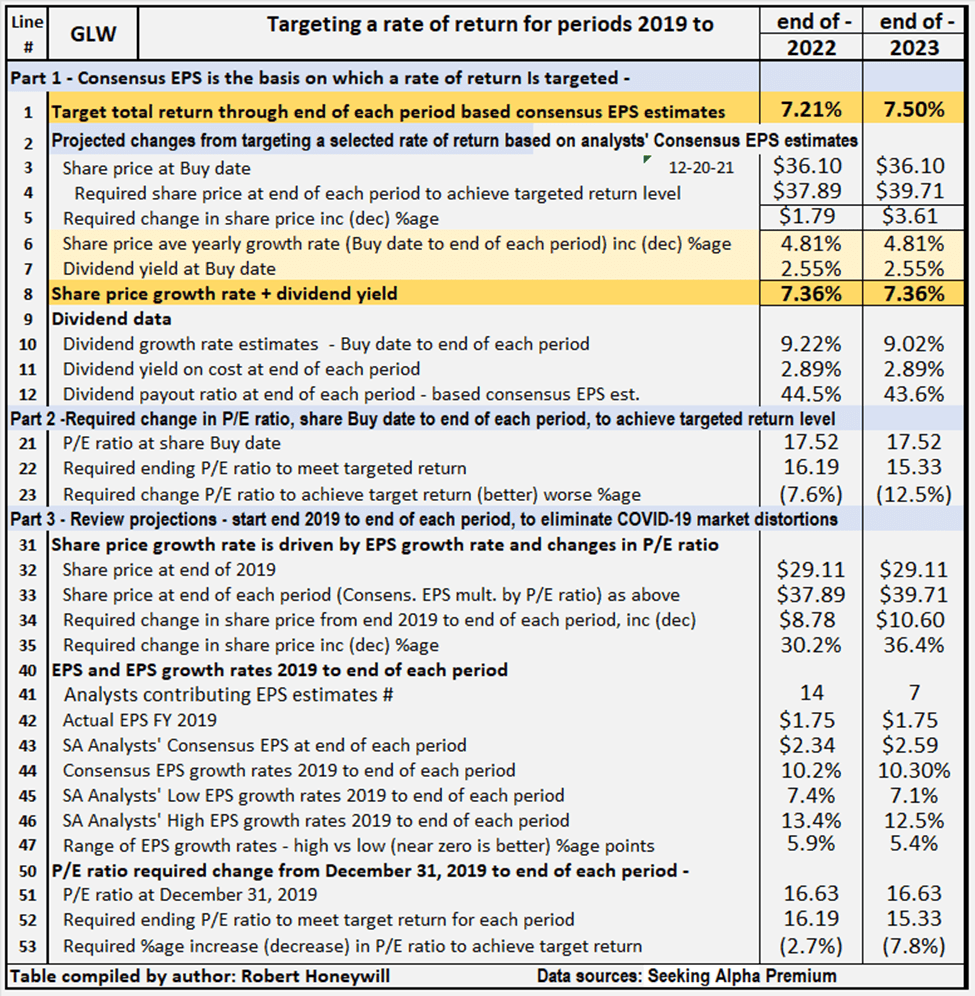

Table 2 - Targeting a 7.5% return Table 2 provides comparative data for Corning, assuming share price grows at rates sufficient to provide total rate of return of 7.5%, from buying at closing share price on Dec. 20, 2021, and holding through end of 2023. All EPS estimates are based on analysts' consensus estimates per SA Premium.

Table 2 provides comparative data for Corning, assuming share price grows at rates sufficient to provide total rate of return of 7.5%, from buying at closing share price on Dec. 20, 2021, and holding through end of 2023. All EPS estimates are based on analysts' consensus estimates per SA Premium.

Comments on Table 2 are as follows:

Part 1 - Consensus EPS (Case 1.1) (lines 1 to 12)

Part 1 shows the amounts the share price would need to increase to achieve a 7.5% rate of return through end of 2023. The share price would need to increase by $3.61 from the present $36.10 to $39.71 at the end of 2023, for the 7.5% rate of return to be achieved.

Part 2 - Required change in P/E ratio to achieve Target 7.5% return (lines 21 to 23)

Part 2 shows the amount the P/E ratio would need to increase or decrease by, from buy date to end of 2023, to achieve the share price level at the end of 2023 necessary to achieve the targeted 7.5% return. For Corning, the P/E ratio at buy date can decrease by 12.5% through end of 2023, and the 7.5% return will still be achieved. Being able to achieve a targeted return despite a reduction in the P/E ratio would normally be regarded as a positive. However, due to the distortions of earnings and sentiment, due to the COVID-19 pandemic, it's difficult to judge whether the change in P/E ratio is a positive, or the result of a distorted starting point. To overcome this difficulty, in Part 3, I review the necessary change in P/E ratio from a different, pre COVID-19 starting point.

Part 3 - Projected change in P/E ratios from 2019 to 2023 (lines 31 to 46)

In part 3, I start with the share price at Dec. 31, 2019, before the impact of the COVID-19 pandemic on earnings and market sentiment. The end point is projected share price at end of 2023, when it's assumed the market and earnings are no longer materially impacted by the COVID-19 pandemic. For Corning, the share price would need to increase by $10.60 from $29.11 at Dec. 31, 2019, to $39.71 at end of 2023, and, as detailed in Part 1, at $39.71, the targeted 7.5% rate of return would be achieved. For Corning, there are a number of givens in our assumptions. Using these givens, the change in the share price for Corning, from Dec. 31, 2019, to end of 2023, can be expressed as mathematical formulae as follows:

A - Change in share price, due effect of EPS growth rate, equals share price at beginning multiplied by (1 plus average yearly EPS growth rate) to the power of number of years invested

= $29.11*(1+10.3%)^4 = $43.08 (that would be the result if the share price grew in line with EPS growth, and the P/E multiple remained constant)

B - Change in share price due change in P/E ratio equals share price adjusted for EPS growth rate multiplied by (1 plus/minus percentage change in P/E ratio)

= $43.08*(1-7.8%) = $39.71 (price required at end of 2023 to provide 7.5% total return, buying at current share price)

The increase of $13.97 ($43.08 minus $29.11) due to the average yearly EPS growth rate is cumulative, and share price will continue to increase the longer the shares are held, and the growth rate continues. The decrease of $3.37 due change in P/E ratio ($43.08 minus $39.71) has a one-off effect. A continuing high or low P/E ratio has no impact on future share price growth, only a change in P/E ratio affects share price, not the level of P/E ratio.

Next, rather than targeting a specific rate of return, I look at historical P/E ratios to see the potential impact on returns of a reversion to these levels of P/E ratio. First of all, I should explain a little about the Dividend Growth Income+ Club approach to financial analysis of stocks.

Understanding The Dividend Growth Income+ Club Approach

Dividend Growth Income+ Club logo Copyright: Robert Honeywill 2020

Dividend Growth Income+ Club logo Copyright: Robert Honeywill 2020

Total Return, Dividends, Share Price

The only way an investor can achieve a positive return on an investment in shares is through receipt of dividends and/or an increase in the share price above the buy price. It follows what really matters in share value assessment is the expected price at which a buyer will be able to exit shares, and expected cash flow from dividends.

Changes In Share Price

Changes in share price are driven by increases or decreases in EPS and changes in P/E ratio. Changes in P/E ratio are driven by investor sentiment toward the stock. Investor sentiment can be influenced by many factors, not necessarily stock specific.

"Equity Bucket"

Earnings are tipped into the "Equity Bucket" for the benefit of shareholders. It's prudent to check whether distributions out of and other reductions in the "Equity Bucket" balance are benefiting shareholders.

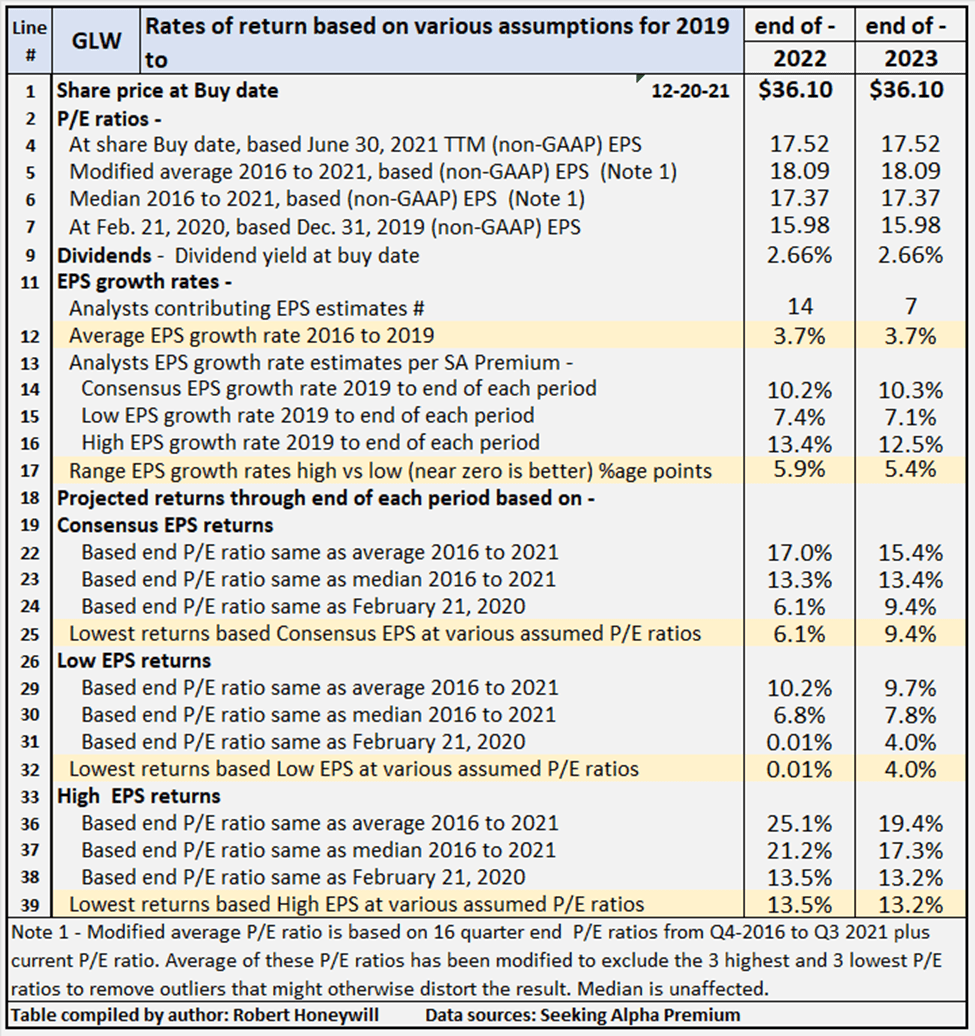

Corning's Projected Returns Based On Selected Historical P/E Ratios Through End Of 2023

Table 3 below provides additional scenarios projecting potential returns based on selected historical P/E ratios and analysts' consensus, low and high EPS estimates per Seeking Alpha Premium through end of 2023.

Table 3 Summary of relevant projections Corning

Table 3 provides comparative data for buying at closing share price on Dec. 20, 2021, and holding through the end of 2023. There are a total of nine valuation scenarios, comprised of three EPS estimates (consensus, low and high) across three different P/E ratio estimates. Comments on contents of Table 3 follow.

Consensus, low and high EPS estimates

All EPS estimates are based on analysts' consensus, low and high estimates per SA Premium. This is designed to provide a range of valuation estimates ranging from low to most likely, to high based on analysts' assessments. I could generate my own estimates, but these would likely fall within the same range and would not add to the value of the exercise. This is particularly so in respect of well-established businesses such as Corning. I believe the "low" estimates should be considered important. It's prudent to manage risk by knowing the potential worst-case scenarios from whatever cause.

Alternative P/E ratios utilized in scenarios

- The actual P/E ratios at share buy date based on actual non-GAAP EPS for Sep. 30, 2021, TTM.

- A modified average P/E ratio based on 21 quarter end P/E ratios from Q4-2016 to Q3 2021 plus current P/E ratio in Q4-2021. Average of these P/E ratios has been modified to exclude the three highest and three lowest P/E ratios to remove outliers that might otherwise distort the result.

- A median P/E ratio calculated using the same data set used for calculating the modified average P/E ratio. Of course, the median is the same whether or not the 3 highest and lowest P/E ratios are excluded.

- The actual P/E ratios at Feb. 21, 2020, share prices based on FY 2019 non-GAAP EPS. The logic here is the market peaked around Feb. 21, 2020, before any significant impact from COVID-19 became apparent, and after FY 2019 results had been released. This makes the P/E ratios at Feb. 21, 2020, reflective of most recent data before distortion of P/E ratios by the impact of the coronavirus pandemic.

Reliability of EPS estimates (line 17)

Line 17 shows the range between high and low EPS estimates. The wider the range, the greater disagreement there is between the most optimistic and the most pessimistic analysts, which tends to suggest greater uncertainty in the estimates. There are four analysts covering Corning through end of 2023. In my experience, a range of 5.4 percentage points difference in EPS growth estimates among analysts is not an unusually large difference.

Projected Returns (lines 18 to 39)

Lines 25, 32 and 39 show, at a range of historical P/E ratio levels, Corning is conservatively indicated to return between 4.0% and 13.2% average per year through end of 2023. The 4.0% return is based on analysts' low EPS estimates and the 13.2% on their high EPS estimates, with a 9.4% return based on consensus estimates. Those are the lowest of the returns under the consensus, low and high EPS scenarios. At the high end of the projected returns for Corning, the indicative returns range from 9.7% to 19.4%, with consensus 15.4%. The difference between best and worse cases is an indication of a degree of uncertainty in analysts' estimates and the stability of historical P/E ratios. The current P/E ratio is 17.52 which is within the range of 15.98 to 18.09 for the historical P/E ratios (lines 5 to 7).

Review Of Historical Performance For Corning

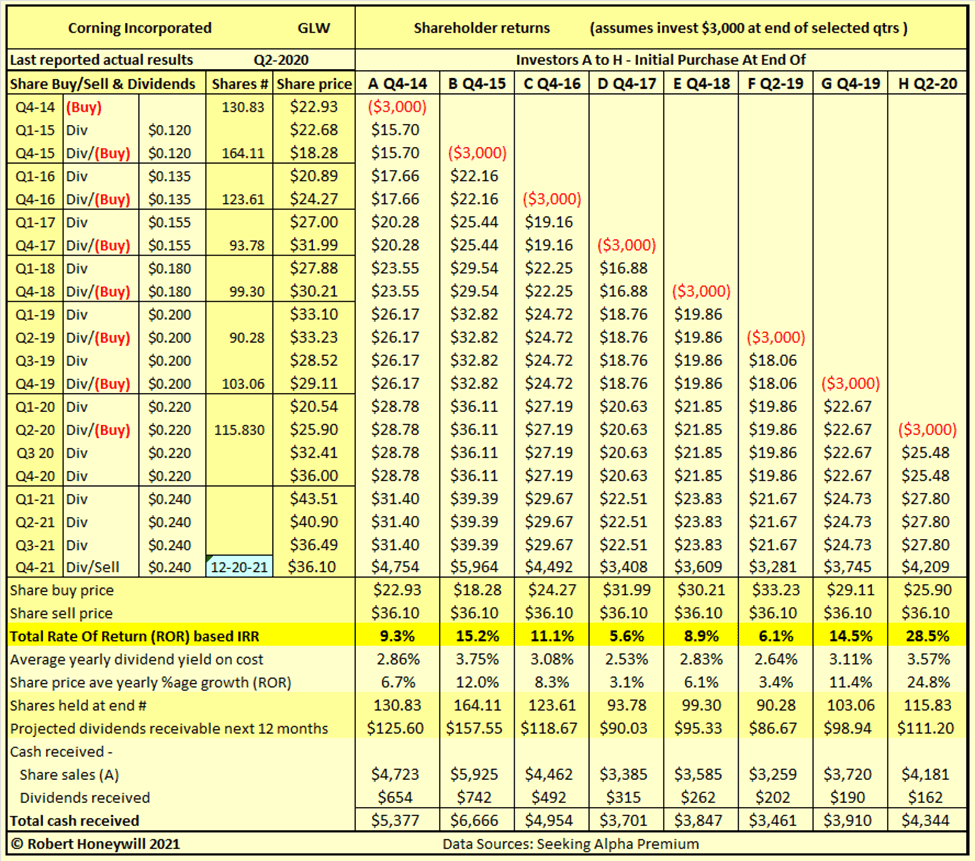

Corning: Historical Shareholder Returns

In Table 4 below, I provide details of actual rates of return for Corning's shareholders investing in the company over the last six years.

Table 4

Table 4 shows returns have been mostly good for investors buying shares in Corning over the last six years. For four of the cases above, returns have been in the double digits, ranging from 11.1% to 28.5%. For the remaining four investors, returns have been in the mid to high single digits, ranging from 5.6% to 9.3%. The rates of return in Table 4 are not just hypothetical results. They are very real results for anyone who purchased shares on the various dates and held through to fourth quarter 2021. In the above examples, the assumed share sale price is the same for all investors, illustrating the impact on returns of the price at which an investor buys shares.

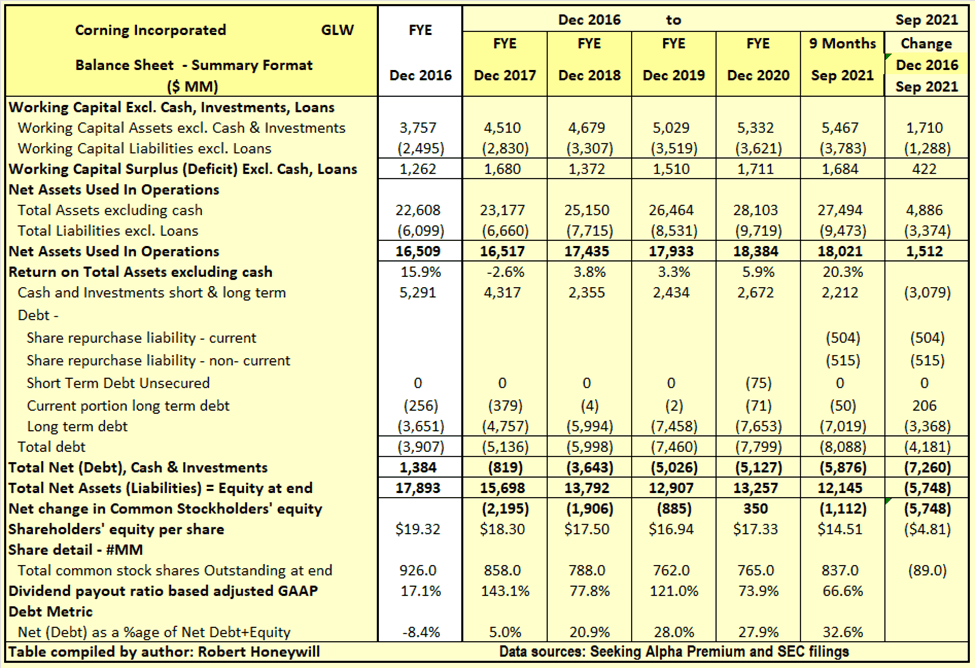

Checking Corning's "Equity Bucket"

Table 5.1 Corning Balance Sheet - Summary Format

Table 5.1 shows a decrease in shareholders' equity of $5,748 million over the 4.75 years, January 1, 2017, through Sep. 30, 2021. This $5,748 million reduction of equity, together with $1,512 million applied to increasing net assets used in operations, was funded by an increase of $7,260 million in net debt. This decrease of $5,748 million in shareholders' equity is despite reporting "core earnings" of $7,220 million over the period and only paying out $3,153 million in dividends, a net increase of $4,067 million. Further analysis is provided below.

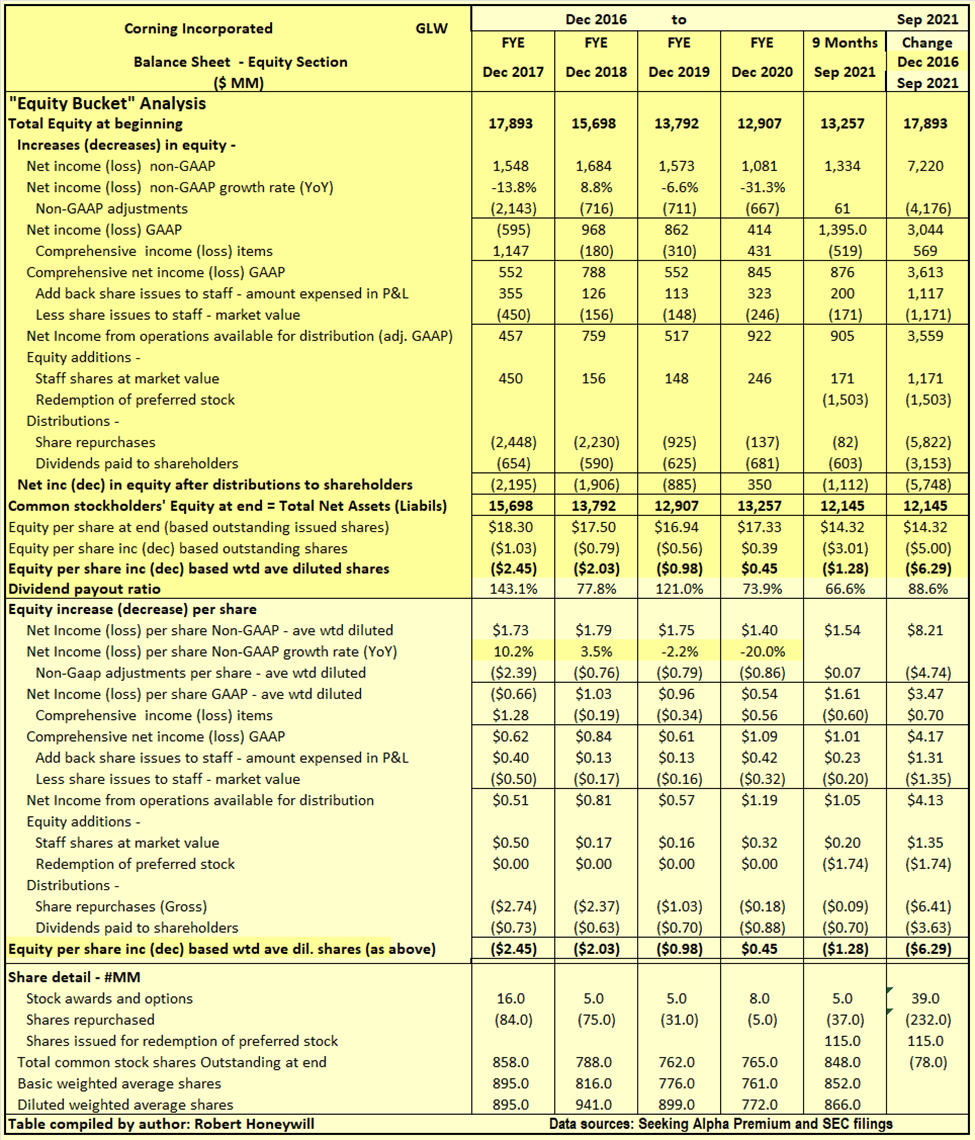

Table 5.2 Corning Balance Sheet - Equity Section

I often find companies report earnings that should flow into and increase shareholders' equity. But often the increase in shareholders' equity does not materialize. Also there can be distributions out of equity that do not benefit shareholders. Hence the term "leaky equity bucket." This has happened with Corning, resulting in a much-reduced benefit to shareholders compared to the considerable earnings reported over the last 4.75 years.

Explanatory comments on Table 5.2 for the period Jan. 1, 2017, to Sep. 30, 2021:

- Reported net income (non-GAAP) over the period totals to $7,220 million, equivalent to diluted net income per share of $8.21.

- The non-GAAP net income excludes $4,176 million of net expense items, regarded as unusual or of a non-recurring nature, in order to better show the underlying "core" profitability of Corning. These items decreased GAAP EPS over the 4.75-year period by $4.74 per share compared to the reported non-GAAP result.

- Other comprehensive income includes such things as foreign exchange translation adjustments in respect to buildings, plant, and other facilities located overseas and changes in valuation of assets in the pension fund - these are not passed through net income as they fluctuate without affecting operations and can easily reverse in a following period. Nevertheless, they do impact on the value of shareholders' equity at any point in time. For Corning, these items were positive $569 million and increased EPS by $0.70 over the period.

- There were share issues to employees, and these were a significant expense item. The amounts recorded in the income statement and in shareholders' equity, for equity awards to staff, totaled $1,117 million ($1.31 EPS effect) over the 4.75-year period. The market value of these shares is estimated to be similar to the amount recorded against income.

- By the time we take the above-mentioned items into account, we find, over the 4.75-year period, the reported non-GAAP EPS of $8.21 ($7,220 million) has decreased to $4.13 ($3,559 million) adjusted net income from operations, added to funds available for distribution to shareholders. Dividends for the period totaled $3,153 million, ~89% payout of the $3,559 million adjusted net income from operations available for distribution, leaving a balance of $406 million addition to equity.

- Issues of staff shares, assessed at estimated market value, increased equity by an estimated $1,171 million over the 3.5-year period. Share repurchases totaled $7,325 million. After taking account of shares issued to staff, net share repurchases were $6,154 million. This $6,154 million was offset by the $406 million net addition to equity from operations, resulting in the $5,748 million reduction in equity per Table 5.1 above.

Summary And Conclusions

At Sept. 30, 2021, the company had debt of $8,088 million (including $1,019 million owing for share repurchases) and cash of $2,212 million resulting in debt net of cash of $5,876 million. There has been an increase in net debt over the 4.75 years of $7,260 million. This $7,260 million additional borrowing can be attributed primarily to $7,325 million in share repurchases. It's difficult to see how the share repurchases have been a benefit to shareholders. The net share repurchases have reduced share count, but this has not been sufficient to cause EPS to grow as can be seen in the statistics in Table 1 above. Earnings have declined through end of 2020, EPS has been flattish and debt has increased markedly over the last 4.75 years. Fortunately, there are signs of real EPS growth in 2021 and beyond which could lead to high single to double digit returns, buying at current share price and holding through end of 2023.

Dividend Growth Income+ Club - Register today for your Free Trial.

Click Triple Treat Offer (1) Your Free 2 Week Trial; (2) 20% Discount New Members; (3) Bespoke reviews for tickers of interest to subscribers.