Christoph Burgstedt/iStock via Getty Images

Introduction

I believe the headline serves as the fundamental question determining whether the recent plunge in Meta platforms (FB) stock constitutes a buying or selling opportunity. The Q4-2021 earnings and forward FY2022 guidance released on February 2nd 2022 turned out to result in the biggest loss of market cap in a single day for an individual company - ever.

In a very brief summary, investors were left with a very strong FY2021, a Q4-2021 that was good, but also underperformed slightly according to expectations while the forward FY2022 guidance left investors gasping for air. As the stock market always considers the future more so than the past, a fantastic FY2021 couldn't keep the stock from plunging.

While I'll visit all of those points, the more fundamental question to ask oneself is whether faith in Mark Zuckerberg and his management team remains, which will also serve as the core of my discussion. Numbers matter, they always do, but right now Meta Platforms is at crossroads where they are about to plough the majority of their war chest into a totally new business venture. At the same time as the legacy business is finally feeling the strain of competition and data privacy, perhaps the most challenging period for Meta Platforms and its shareholders is ahead of the business, ultimately revealing itself over the coming years. In such a situation, what matters is quality of leadership combined with a solid and trustworthy vision, and it's about the fundamental and long-term orientated decisions.

Q4-2021 Financials Wasn't The Problem

Meta Platforms is a money minting machine. If we compare the company to Apple (AAPL), Microsoft (MSFT) and Alphabet (GOOGL) (GOOG) across the last decade in terms of average operating margin, percentage-based revenue and EPS growth, Meta Platforms beat all of them.

EPS revisions (www.seekingalpha.com/symbol/FB/earnings/revisions)

However, where the company doesn't beat its peers, are the forward expectations, and also one of the major reasons why the company sold off so massively as expectations have suffered. When considering forward EPS growth expectations, Meta Platforms finds itself bottom of the pack together with Apple.

Meta Platforms Full Year 2021 Financial Highlights (www.investor.fb.com)

Glancing over the Q4-2021 numbers and the company delivered strong top-line growth at the expense of a significant increase in total costs resulting in a reduction in net income of 8% compared to Q4-2020 as the company gears up towards its metaverse focus. The quarterly EPS of $3.67 proved to be miss of $0.15 according to consensus expectations.

Comparing FY2021 with FY2020 and the positives are very difficult to hide. A 37% top-line growth while keeping costs at a growth of 34%. Eventually resulting in a net income growth of 35% and EPS growth of 36%. Very impressive for a company sprinting past the $100 billion revenue mark. The company also churned out $18.1 billion in cash from operating activities, up from $14 billion when compared quarter-on-quarter - very impressive.

A new addition to reporting is management ensuring a split in terms of divisional performance allowing to understand the break down performance between "Family of Apps (Facebook, Instagram, Messenger, WhatsApp and other services)" and "Reality Labs (augmented and virtual reality related consumer hardware, software and content)". As can be seen above, the total costs and expenses during Q4-2021 ballooned by 38%.

Meta Platforms Division Split Full Year 2021 Financial Highlights (www.investor.fb.com)

Reality labs secured a revenue of $2.2 billion, primarily associated to sales of Meta Platforms leading VR headset, the Quest 2, where management highlighted a strong holiday season. On the other hand, the division ended up with a total loss of $10.1 billion, underlining the investment priority of this division and what we can expect looking forward as Meta Platforms will be betting on the metaverse venture.

Where the Q4-2021 wasn't quite as impressive, was when considering the daily active users (DAU) and monthly active users (MAU). Facebook has 1.9 billion daily active users, and 2.9 billion monthly active users and gravity is starting to assert itself as the global population is finite, making is difficult for Meta Platforms to continue growing these numbers. As such, we also saw a small quarter-on-quarter decline for Facebook daily active users coming in at 1.929 billion compared to 1.930 during Q3-2021, something shareholders aren't used to experience. However, no other company can boast having anywhere near a similar number of users and Meta Platforms has still driven extremely strong advertising growth per user. Despite the fact the userbase will be difficult to expand from hereon, it doesn't take away the fact that advertisers will be looking towards Meta Platforms family of apps.

Facebook Daily Active Users (www.investor.fb.com)

Seen from my chair, it's hard to argue anything alarming about the development in DAUs, it's just not what we have been used to, but with a finite global population, there had to come a day when the numbers would stop climbing. That doesn't mean Facebook as a platform is about to vanish.

The Headwinds About To Impact Meta Platforms - Revenue Slowing Down & Costs Increasing

Rarely have I been so curious to dive into the earnings call as this time, not least because of the extremely strong market reaction. Zuckerberg didn't make it far into his opening remarks before he laid out the investment priorities of his company followed by a more detailed elaboration.

"…Today, I'm going to discuss our seven major investment priorities for 2022: and they're Reels, community messaging, commerce, ads, privacy, AI, and of course the metaverse… (On the metaverse priority)… We're focused on the foundational hardware and software required to build an immersive, embodied internet that enables better digital social experiences than anything that exists today... We're working towards a release of a high-end virtual reality headset later this year and we continue to make progress developing Project Nazare, which is our first fully augmented reality glasses. As for software, Horizon is core to our metaverse vision. This is our social VR world-building experience… And we've seen a number of talented creators build worlds like a recording studio where producers collaborate or a relaxing space to meditate. And this year, we plan to launch a version of Horizon on mobile too, that will bring early metaverse experiences to more surfaces beyond VR."

Management listed a number of headwinds impacting the forward expectations, thus calling for the market to reprice the stock. Some of the headwinds identified during the earnings call include

- Q1-2022 revenue growth expected at 3-11% YoY growth translating to revenue between $27-29 billion, below analyst consensus estimates of $30.3 billion

- Tough YoY comps due to the strong growth shown during FY2021 and also, that the Apple IOS changes weren't in effect during Q1 and Q2 of 2021.

- Apple's IOS changes negatively impacting the outlook due to the tune of $10 billion for FY2022 guidance, due to its tracking transparency feature which has negatively impacted digital advertising as it limits add accuracy

- Competitive pressures with TikTok being a named example with Meta Platforms making their reels an investment priority as TikTok has struck a nerve here, management citing that reels exhibit great engagement and willingness from users to spend significant amounts of time. Meta Platforms like TikTok, Pinterest (PINS), Snapchat (SNAP), etc., all fight for the same eyeball hours and it's with this understanding, that management cite the growing competitive pressures

"And we believe the impact of iOS overall as a headwind on our business in 2022 is on the order of $10 billion, so it's a pretty significant headwind for our business."

Naturally, the IOS impact is no small thing, and Sheryl Sandberg, COO, also elaborated on the matter as analysts naturally questioned it in more detail. Here she laid out, that in essence it concerns advertisers worrying their return on investment from advertising is reduced, where Sheryl stated that Meta Platforms has already made progress in terms of remedying the situation in order to adjust to the new conditions - but also that it would be a year-long journey. The holiday season of 2021 apparently also revealed a problem connected to delay in data transmissions making ads less effective as adjustment is difficult on the very short-term as would be the optimum during the busy days of a holiday season.

The discussed impact above was related to the IOS 14.5 update, and it would only be natural to ask whether we could expect more drastic changes when faced with newer updates, and here the management team stated they expected further impact related to future IOS releases, but nowhere near the consequences related to IOS 14.5

When diving into the 2022 outlook, management has forecasted total expenses in the $90-95 billion range, a significant expansion from the $71 billion for FY2021. David Wehner elaborated, that the main driver of that increase would be related to the seven investment priorities, with emphasis on headcount growth as the largest driver of costs while reality labs is expected to continue driving a substantial loss, which was labelled as a "meaningful operating loss", all part of the FY2022 expense outlook.

In total, revenue growth is slowing down, and costs are increasing, not exactly what investors like to hear.

A Man With A Vision

When dealing with a company about to embark on a new strategic business initiative having already communicated the willingness to splash additional billions into investments effectively trying to build the market and experience, it's about the leadership making smart capital allocation and navigating towards the value-adding decisions. Again, coming back to the article headline.

Much can be said about Mark Zuckerberg, but I don't believe it's possible to deny that he has shown great instinct through his reign of Meta Platforms, allowing to line the pockets of shareholders for almost a decade. However, this is perhaps also the first time he will be fighting on more fronts at the same time.

Zuckerberg recognized the potential of his business and decided not to be swayed by the many suitors trying to acquire Facebook while it was still a mosquito on the savannah, many years before it turned into the apex predator it is today. Most famously, he turned down a $1 billion offer made by Yahoo, the rumors saying he even went against his own board at the time. Supposedly, titans like Microsoft and Google, now Alphabet even tried to make Zuckerberg sell at one point. On that day in July 2006, Zuckerberg was only twenty-two years old and running a Facebook with a single digit million users and $20 million in revenue when confronted with a $1 billion offer for his company. Facing up against the likes of Peter Thiel, a board member at the time and a legendary venture capitalist with billions to his name having co-founded PayPal (PYPL), Zuckerberg argued there was no reason to sell as the company was drastically undervalued given the vision, he had for its road ahead. Twenty-two years old, it takes some nerve to turn down $1 billion where most would have ended up in his own pockets.

A little less than six years later, and Zuckerberg again exercised his immaculate understanding of how social media would develop, by picking up Instagram for $1 billion, possibly being one of the greatest deals of this century. The deal was agreed to in April 2012, less than a month before the company went public at a $104 billion IPO. The details of how the deal came to life has become public knowledge as a US House antitrust committee made public the e-mail exchanges between Zuckerberg and his former CFO, David Ebersman. Facebook, and in particular Zuckerberg, wanted to acquire Instagram having recognized the competitive threat it represented along with a strong integration opportunity. At that point in time, Instagram was a company of only a handful of employees and very few, if any, could have foreseen that it would one day turn into an annual revenue business of $20 billion. Looking in the rear-view mirror and this deal would have been obvious for anybody, but back then Instagram was only a mobile app with just above 20 million users, and nobody had ever paid $1 billion for such a thing. Holding more than half of the voting rights, Zuckerberg hammered out the deal in a very short timeframe, even compromising on the typically very lengthy due diligence process having recognized that he wasn't the only potential buyer for Instagram, therefore wanting to limit the possibility for Instagram's management to get cold feet during the process.

A few years later, and Zuckerberg did it again when he acquired WhatsApp for $14 billion, a messaging app that has in excess of two billion users globally, today. During 2014 he also picked up Oculus VR for $2.3 billion, laying the very early foundation to the future metaverse bet.

Another example is the failed acquisition attempt of Snapchat, which Zuckerberg was ready to add to the fold as early as 2013 when he supposedly offered to acquire it for $3 billion in order to strengthen appeal with younger users. While we are all familiar with Snapchat today, back then it was only two years old and years away from its $60 billion market cap of today. As with Instagram, Snapchat didn't have meaningful revenue but exerted itself through strong engagement and growth though barely holding 20 million users back then. The founders turned down Zuckerberg, but the point being, that Zuckerberg and his team recognized the potential in Snapchat before it became the player it is today.

Depending on how one frames it, Zuckerberg has either had the mental capacity to foresee how the market would develop, or he was lucky to pick up golden nuggets way before Meta Platforms received the regulatory attention it is under today, making such prospective deals close to impossible if we were talking about today.

Having slowly grown to become the apex predator of the savannah, Zuckerberg has along the way recognized the need to rid himself of his competitors either acquiring them or "copying" a select number of abilities of competitors and integrating those functionalities into his own social media empire - effectively either killing or acquiring the competition. A more flattering name for this, would be that Zuckerberg has great business acumen, that he recognizes a potential long before all the great minds surrounding him. It's easy to act as a Monday coach and say that it was all so very obvious, but imagine the amount of potential platforms that he and his team could have opted to try and acquire, except, he managed to choose those which later on created substantial value.

Fast forward, and here we are again, at some sort of crossroad that we will all look back at in ten years and say "of course, everyone could have seen that coming", as if it was just another Instagram. At least, that is what people will be saying if he pulls it off, again. The shifting focus towards significant capital allocation directed at the metaverse is something he has most likely pondered for some time, but this is not a deal that can be closed over night or that comes with a single digit billion-dollar price tag.

No, rather Zuckerberg is more or less betting his company's future by making it one of his top investment priorities, already having dumped billions into the new priority while realistically only having his Oculus VR headset to show for it as of right now, while hoping he will pioneer the next leap in the internet age.

Meta Platforms Glassdoor Review (www.glassdoor.com/review)

Having been named Time's person of the year in 2010 and making the short-list when discussing the most influential and powerful people walking the planet, there is little doubt that Zuckerberg is in a position where he can make as informed a decision as possible while surrounded by a capable board of directors and management team. Naturally, any leading company counting its market cap in the hundreds of billions comes with a competent board and Meta Platforms is no exception.

One thing however which has plagued the company during its first 18 years of life (the legal age in my native country) is its run-ins with regulators and law makers, having found Zuckerberg in Senate hearings multiple times. Operating at the edge of morality related to privacy and data management, social media addiction and related social issues. To use the metaphor related to the company's age, if the company was a teenage guy, it most likely would have a few priors and be a known face with the local law enforcement as it went its own ways. Similarly, the decision to go full speed ahead with the metaverse vision, the company will once again risk experiencing run-ins with regulators and lawmakers while striving to complete the vision. This remains a balance that has to be tread carefully.

The leadership team at Meta Platforms has opted for significant risks but also stand to reap massive rewards if they have spotted the trend correctly and develop the "marketplace/experience" before its competitors. If proven correct, this bet could wildly influence how we live, work, video games, commerce and socializing between people on a broader scale.

Given Zuckerberg's track record, it's difficult not to argue, that he has proven capable in making strong value-adding long-term decisions on behalf of his company and shareholders.

The Meta Platforms We Are Left With

We are left with a company that feels competition heating while some of its current offerings belonging to the family of apps appear to have finally reached the upper limits for how far they can grow their userbase - remember that doesn't necessarily translate to, that they can't be monetized further. It can easily come off as gloomy but let's not forget that even though the IOS changes will provide significant headwind, that Meta Platforms will still drive positive cash flows counted in the billions. I believe we need more quarters to understand how the company will fare and what sort of free cash flow we can expect as the headwinds materialize themselves in combination with the strong investments being driven into building the metaverse.

However, Meta Platforms is sitting on top of $48 billion of cash and cash equivalents while continuously adding to that pile on a quarterly basis. The company utilized $44.8 billion for share repurchases during 2021, with $19.2 billion allocated during Q4-2021 alone with the cash position only having dwindled by roughly $15 billion YoY. Another $38.8 billion remain under the current repurchasing program, and if investors are worried about the headwinds related to the IOS change and investment prioritizations already listed, then this would be a natural place for management to reduce spending for Meta Platforms if needed.

It is easy to anticipate, that companies can grow uninterrupted forever, but let's take Apple as a quick example of the opposite. FY2015 revenue for Apple came in at $233 billion, while both FY16 and FY17 were below that before FY2018 resulted in $266 billion. Similarly, FY19 was again below the year prior before FY2020 resulted in $275 billion. Sure, Apple isn't Meta Platforms and vice versa, but it's easy to be grasped by fear, that Meta Platforms' best days are behind it and that growth is done. On the other hand, one could perceive the current situation as one where Meta Platforms has to adjust its foothold before it can go for the next leg up the revenue ladder.

Having said that, Meta Platforms is still expected to grow its revenue for the coming three years with current FY2022 expectations for revenue coming in at $132 billion compared to the $118 of FY2021. Further, we must not forget that Meta Platforms counts its userbase in the billions and therefore is a natural priority for advertisers. In no means can I see a scenario where the offerings and platforms of Meta Platforms become irrelevant.

Zuckerberg and his management team are ready and willing to commit a double-digit number of billions to build the metaverse experience, and as capital can only be allocated once, it also derives that this strategic priority takes precedent over other alternatives. In other words, out of the options available, management has decided this possibility carries the best risk-reward potential and is the most meaningful for Meta Platforms. While there isn't a clear path to profitability right now, the management team must be confident, that they can take this priority to a place where it secures a return on invested capital somewhere in the double digits for it to create meaningful value for the company and be somewhat in line with the existing returns on capital.

Given management historical ability to make the right decision, I believe they should receive benefit of doubt in the current situation.

Valuation

For once, the discussion on valuation is a little bit less meaningful than it would typically be. Why? Because Meta Platforms is in a new situation. Being pressured on its existing business, not exhibiting the growth the market is used to while having made a major strategic priority where it's very difficult to gauge where it will end and how the profitability will look like.

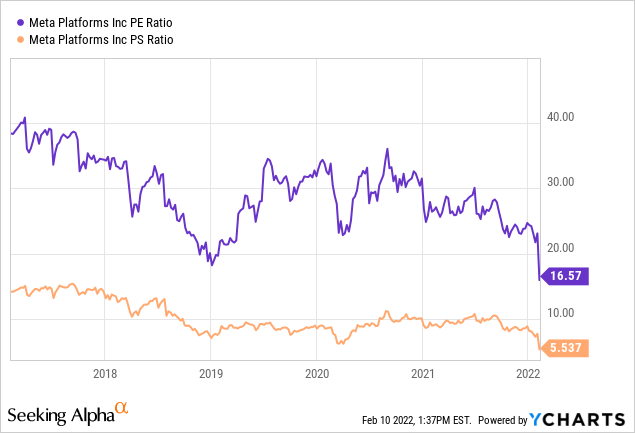

- With a forward EPS estimate of $12.50, the stock currently trades at around a forward price/earnings ratio of 18.5 as well as a forward price/sales ratio of just above 4 (assuming revenue growth between 10-15%).

These aren't levels we are used to, and it's easy to immediately conclude that Meta Platforms must be a screaming buy as forward P/E and P/S are well below what we have witnessed in recent years. However, the historical levels were based on a different outlook on both revenue and profitability, not to mention the competitive environment.

As shown in the forward EPS revisions early on in the article, the consensus FY2022 EPS estimate is $12.5 and $14 for FY2023 which would put the 2023 P/E at 16.5, and already ahead of the FY2021 EPS of $13.8. Meta Platforms has had a historical tendency to overshoot the EPS consensus estimates, and the forward-looking valuation levels are appetizing.

Pullbacks within the FAANG stocks have typically represented buying opportunities, but I'd be careful with drawing a straight line between history and future in this particular instance as the playing field has changed. The earnings for Meta Platforms should be more volatile than historically not least due to the capable field of platforms fighting for the same eyeball hours globally and the fact that management also underlined that not all platforms have been hit equally hard by the IOS changes.

From my standpoint, a false expectation would be, that Meta Platforms could soon be expected to close the gap to its historical valuation. In a situation where management is betting billions towards an initiative with great uncertainty, I'd expect the market wanting to see a clearer path towards the end state before the company will be rewarded with a higher valuation once again. All that to say, that the mid-term returns expected out of Meta Platforms may well be lower than the average seen through the last decade.

Being cheaper than its peers isn't a quality in itself.

However, no other company has access to the same pool of users and the company is putting serious muscle behind its metaverse venture. At this point in time, Meta Platforms comes at a fair discount relative to the uncertainty keeping the long-term earnings power of the company in mind.

Conclusion

Mark Zuckerberg has shown a strong track record when measured on his decision-making related to building social media and monetizing it through the last decade. At pivotal moments, he has chosen the right path more than once in terms of decisions that could appear as no brainers today, but which required a strong in-depth ability of setting the right course to avoid wasting billions of dollars on going the wrong direction.

As a pioneer already having been center in building social media to what it is, Zuckerberg and his team should be capable of turning the current massive operating loss of reality labs into a profitable business over the long-term. Meanwhile, the existing 'family of apps' will continue to be a highly profitable business securing strong free cash flows that can be funneled into the new business venture, though there are headwinds impacting the company as seen impacting the business to the tune of $10 billion for FY2022 while having permanently elevated the cost base as the Metaverse bet ramps up its staffing and investment trajectory.

More so than letting the immediately available numbers conclude whether the investment case is positive or not, I'd look towards the decision-making track record, which is almost immaculate given how far Meta Platforms have made it through its lifetime. As such, there is a good chance, that this will be yet another profitable business venture for the company, but before profit comes investments, and investors have to accept that it will take time to turn a double digit billion operating loss into a positive one with all the uncertainty that comes with it along the way.

Further, when looking at the current valuation, it does offer what appears to be an attractive entry if Meta Platforms can indeed deliver on the consensus expectations for especially FY2023 and beyond, which doesn't appear unreasonable given the EPS expectations are only slightly beyond what was achieved during FY2021 despite the consensus estimate of FY2023 revenue crossing $150 billion. While I favor focusing on the decision prowess of management in this situation, the numbers don't look shabby either.

With the current information available, Meta Platforms deserve a bullish rating for long-term investors.