JStuij/iStock via Getty Images

As I wrote about in my last piece, Chemours (NYSE:CC) is what remains after DuPont spun off its performance chemicals into a separate company, done in 2015. There are some fundamental risks to this business with regards to its legacy from this time. It does take some fundamental upside beyond the usual to consider this business a "BUY", as I see it.

For the time being, I'm careful here, and I will show you why.

Chemours - Looking at recent results

Chemours company recently dropped as much as 15%. The reason for this was simple. Expectations and forecasts had been riding high, much like the share price because Chemours was expected to deliver a good beat and some good guidance.

Instead, they delivered more in line with my expectations. Below are forecasts, and with guidance that reflects the ongoing supply chain and pandemic issues. While it may be viewed that a 15%+ drop in a single day is a lot for a miss of less than €40M in revenues on a quarterly basis, it reflects the current market trends and the way Chemours is viewed by the market.

That isn't to say that results or operations were all bad. Results were indeed back to pre-COVID-19 levels, certainly above that 2020 with a 28% YoY net sales increase. In fact, every single metric was up either slightly or significantly, and margin improvements came at 300 bps on an EBITDA basis for the full year.

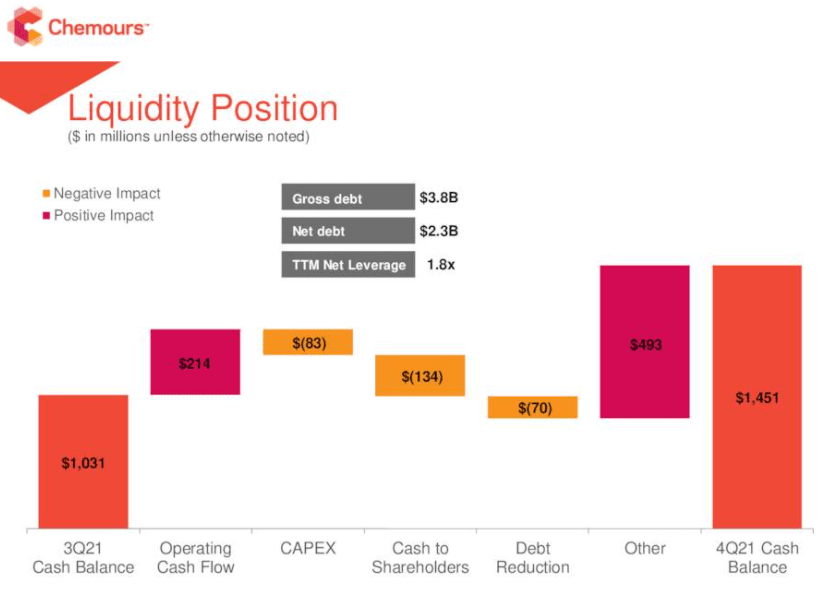

Full-year trends are what is interesting here. 4Q21 isn't that interesting to me due to weak comps. What we're looking for is a fundamental reversal in the company's pandemic trends. What we're looking for is fundamental strength. There is some delivery of this.

Chemours 4Q21 Results (Chemours IR)

On a segment-by-segment basis, Chemours is showing good results as well. More importantly, the expected segment results for 2022 are mostly positive. Titanium Technologies is seeing sustained demands - but weighed down by ore constraints, raw material inflation, logistics challenges as well as customer supply chain issues. In short, the company's core segment isn't an easy place to be in at this time, nor is it expected to improve massively in the near term.

The expectations for other segments are good. CC expects continued adoption of its solutions in Specialized Solutions/Thermal, but it is once again very reliant on overall Automotive recovery. These sorts of recoveries are not exactly helped by the current standstill in Automotive HQ near the Canadian border at this time. This is a trend we see in Performance Materials/Chemical Solutions as well. Solid demand growth is anticipated in 2022, but the logistics issues from input costs, energy costs, logistics costs are massive here - and the company expects them to persist.

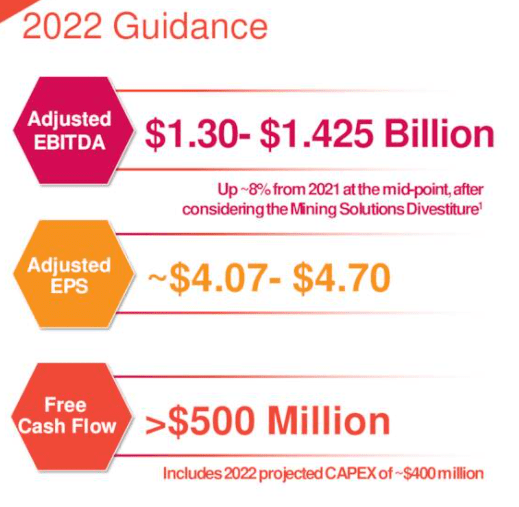

The guidance calls for an 8% YoY increase in 2022, and an EPS between $4.07-$4.7. This is a wide range and includes a lot of the uncertainty we're currently seeing, although it is important to point out that even with this 8% adj. EBITDA increase guidance, there is the assumption that the macro will improve. While I view some improvement as likely, current visibility here is low. It also explains the market's reaction to what the company did here.

Chemours 2022 Guidance (Chemours Ir)

There are a few things not to like here. I went through the potential controversies and litigations in my last article. I suggest you read up on them there. I'm not one to say that this makes a company uninvestable - it does not. But it certainly impacts the overall valuation of the business.

Look - what I'm saying is that we're seeing companies drop massively due to these inflation concerns, supply chain issues, and other things. It doesn't seem to matter much even if they beat their consensus. Goodyear (GT) recently beat massively but is still on a 24% pre-market slide as I am writing this article. The implication of inflation and these issues are very, very relevant to your portfolio's overall health. if you're willing to take on the risk that Chemours comes with - that's of course an option, but I would personally be somewhat hesitant to do so at this time by investing in the common.

On a high level, I view it as unlikely that Chemours will be able to push through the ongoing inflation increases with the same ease as they did during 2021. While the company is taking action that's supposed to keep increasing EBITDA to that 8% guidance, it's my view that this is not a conservative stance. If we consider the litigation issues and risks and couple this with input uncertainty and supply chain issues both on a company and customer-side, we get the risk profile of other, excellent chemical companies such as BASF (OTCQX:BASFY) and LyondellBasell (LYB), but with the addition of massive litigation.

Do we get a higher yield or upside for this? No - the yield is in fact significantly lower than both of these companies and comes in at 3.33%

Let's look at valuation.

Chemours Valuation

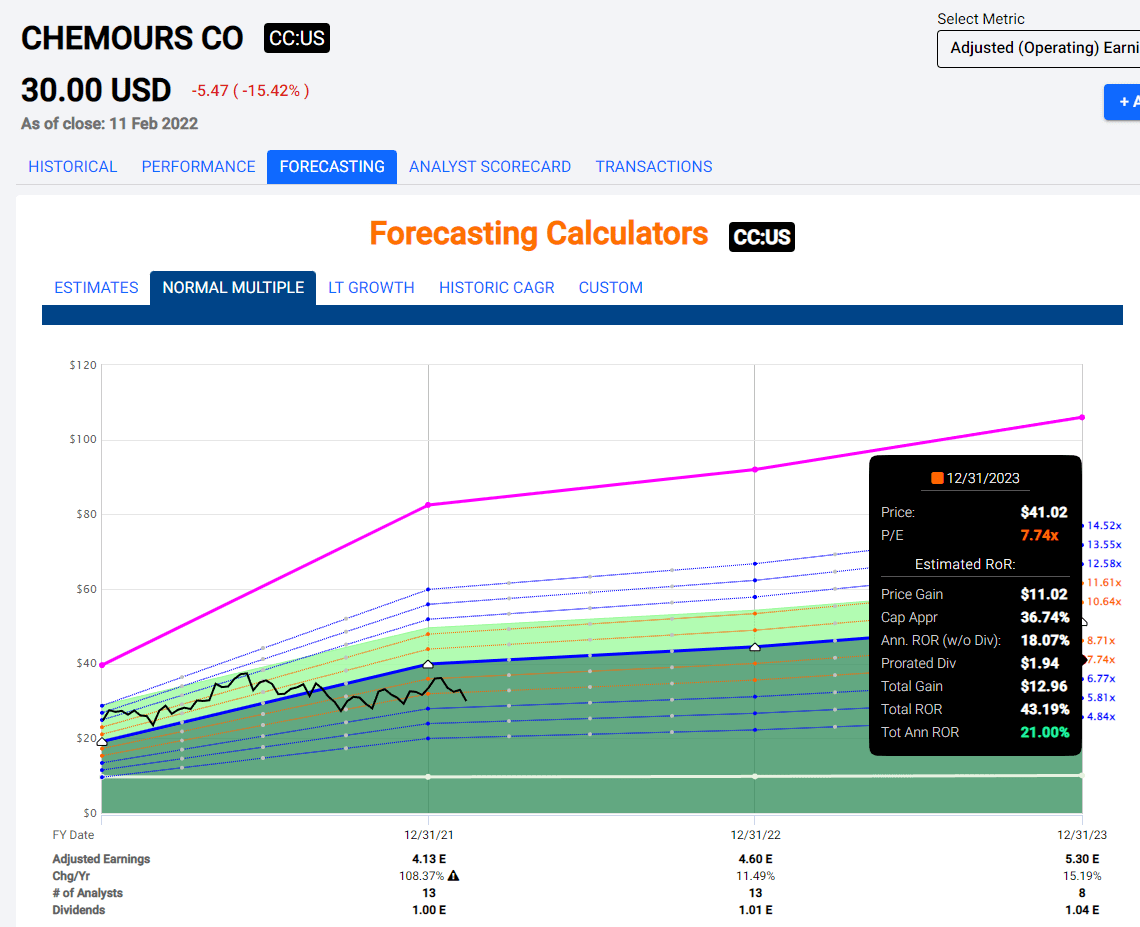

Chemours did come in at a pretty good 2021. Assuming 2022 holds, and 2023 comes in even better thanks to the aforementioned efficiencies, and the litigation doesn't provide any significant downside, the upside for Chemours at this point is significant. At least in theory.

Chemours Upside (F.A.S.T graphs)

The problem with these forecasts is that Analysts making them have a 0% forecast accuracy, both on a 1-year and 2-year basis. (Source: FactSet) It's pretty amazing, being able to have worse accuracy, even on a 10% margin of error, to the toss of a coin. The company has either beat forecasts by triple digits, prior to the pandemic or failed to meet expectations by about 50-80%.

Because of this, these forecasts can, candidly, be taken as not all that indicative. They could fluctuate wildly - and the litigation of course gives them further fluctuation potential. There is also extremely little dividend growth forecasted, with single-digit GDP/inflation growth being forecasted by S&P Global (Source: S&P Global). Based on current trends and fundamentals, I see no reason to vary my own forecasts from these trends - nor do I see a catalyst for "better" performance.

The risk definitely, to my mind, outweighs the upsides here. This isn't as risky an investment as some growth stocks. But to my mind, the question becomes why you would want to take such an outsized risk when there are far safer and higher-yielding alternatives out there, with similar upside.

This isn't to say Chemours isn't a bad company. But there is, to my mind, little downside to "waiting" for the company to solve its litigation, wait out some of the inflation and cost pressures here. On a high level, the uncertainty about the company is well-reflected in the reaction to 4Q21. Similar to growth stocks, whenever even almost a "beat" causes a double-digit share price drop, you can be certain that there is a lot of underlying uncertainty to the stock and the investment assumptions.

To that end, I present to you that Chemours is still not investable at this price - even if the price is now better.

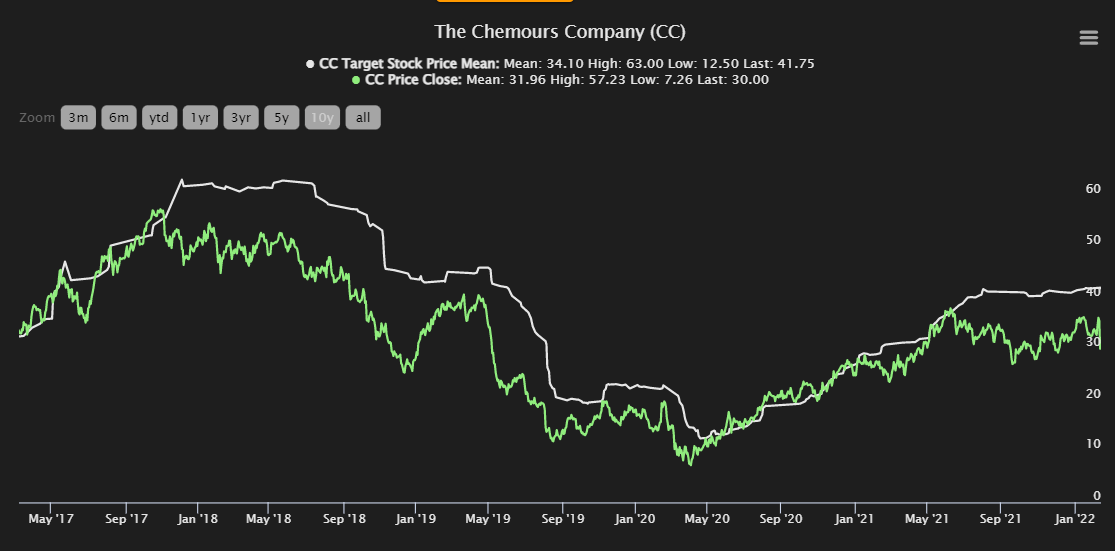

I will however play devil's advocate and say that S&P Global sees a massive upside here. The problem is, these come with not atypical assumptions of premium that rarely materialize.

Chemours S&P global targets (S&P Global/TIKR.com)

You may think that at such an undervaluation, almost all analysts are going to be "BUY" here. That's not the case - 50% of them aren't. There is a wide gap between the "HOLD"s and the "BUY"s here. That isn't, by the way, because some of these analysts hold a sub-$30/share price target. All 12 analysts have a price target that is at least 15% above the current share price. Despite this, 50% of them are at a "HOLD". This tells you quite a bit about the way even analysts with an upside view Chemours.

Me, I come down on the side of the "HOLD", and consider Chemours buyable at around $25/share - a more honest target.

You see, when I give a company a "BUY" target, I do mean that I would BUY the company at that valuation. I don't say "BUY", but then say "buuuuut, I still wouldn't buy here". That to me is not a "BUY" target.

Thesis

My thesis on Chemours is simple.

- At $30/share, I remain a staunch "HOLD" with this company. I would "BUY" Chemours at dirt-cheap valuations with yields that push close to 4%, to reflect some of the risks of litigation as well as the massive volatility of the stock.

- My PT is $25/share.

- Options are a way to invest here. The $26 strike July -22 PUT options come at a premium of $1.7. The yield for that, as I'm writing this, is 16.26% annualized, with an implied cost basis of $24.30 and a YoC of 4.12%. This is a decent option, with only a capital exposure of $2,400. I may write this option within the next 72 hours.

- But the common, that one remains a hard "HOLD" for me.

Remember, I'm all about :

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

This process has allowed me to triple my net worth in less than 7 years - and that is all I intend to continue doing (even if I don't expect the same rates of return for the next few years).

If you're interested in significantly higher returns, then I'm probably not for you. If you're interested in 10% yields, I'm not for you either.

If you however want to grow your money conservatively, safely, and harvest well-covered dividends while doing so, and your timeframe is 5-30 years, then I might be for you.

Chemours is a "HOLD" here.

Thank you for reading.

The company discussed in this article is only one potential investment in the sector. Members of iREIT on Alpha get access to investment ideas with upsides that I view as significantly higher/better than this one. Consider subscribing and learning more here.