kynny/iStock via Getty Images

I will not let anyone walk through my mind with their dirty feet.” - Mahatma Gandhi

Today, we take a look at tech concern Ultra Clean Holdings (NASDAQ:UCTT). The stock seems reasonable or potentially undervalued on an earnings and revenue growth basis. The analyst community is also sanguine about the company's prospects. However, this is a historically volatile part of the market and insiders are frequent and consistent sellers of the shares. Which way does the equity go from here? A full analysis below.

Company Overview:

UCTT - Company History (January Company Presentation)

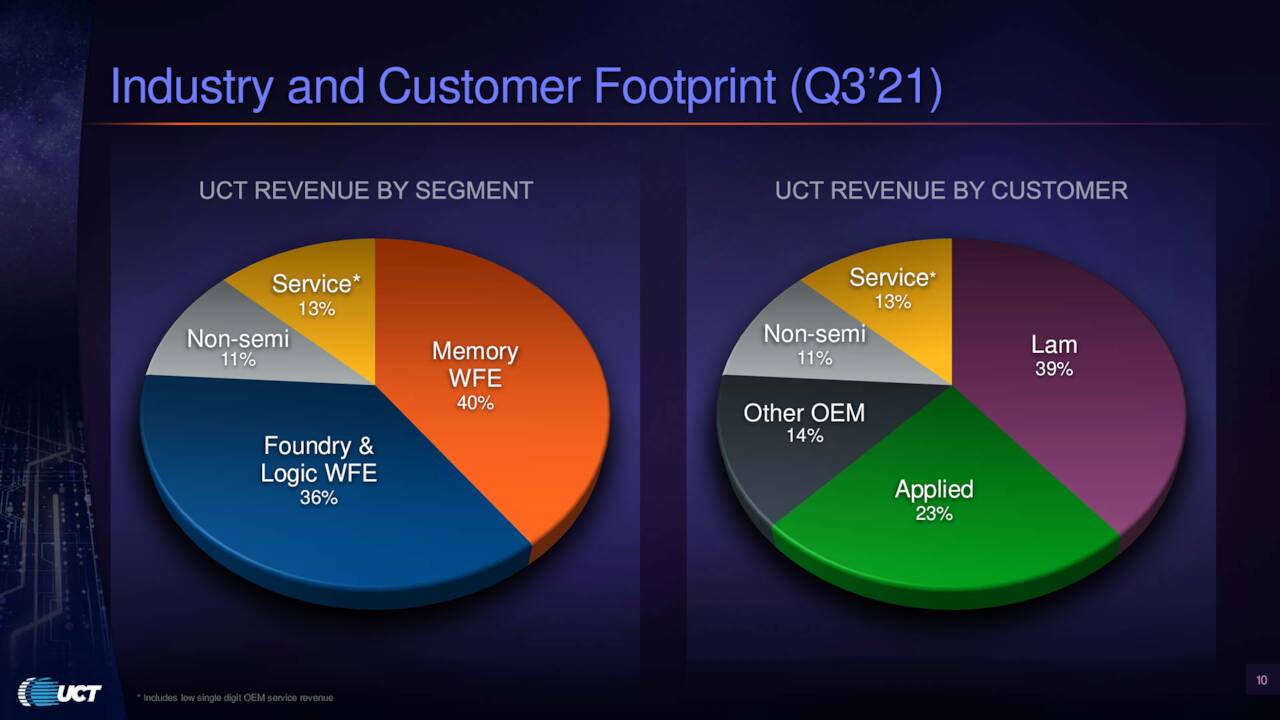

This tech concern is located just outside of San Francisco. The stock currently sells for just under $49.00 a share and sports an approximate market capitalization of $2.2 billion. Ultra Clean Holdings is a developer and supplier of critical subsystems, components and parts, and ultra-high purity cleaning and analytical services, primarily for the semiconductor industry. Two customers do account for over 60% of total sales currently (below). Approximately 85% of the company's revenues come from product sales and the rest come from services.

UCTT - Revenue Breakdown (January Company Presentation)

Recent Events:

At the end of 2020, the company purchased Ham-Let on the Tel Aviv stock exchange, for nearly $350 million. Ham-Let was a leader in the development, manufacturing and distribution of Ultra-High Purity and industrial flow control systems and helped build out the offerings Ultra Clean could provide its end customers.

UCTT - Growth History (January Company Presentation)

It was the latest in a series of acquisitions the company has executed in its history and one of the drivers of Ultra Clean's approximate 50% revenue growth so far in FY2021.

UCTT - History Of Acquisitions (January Company Presentation)

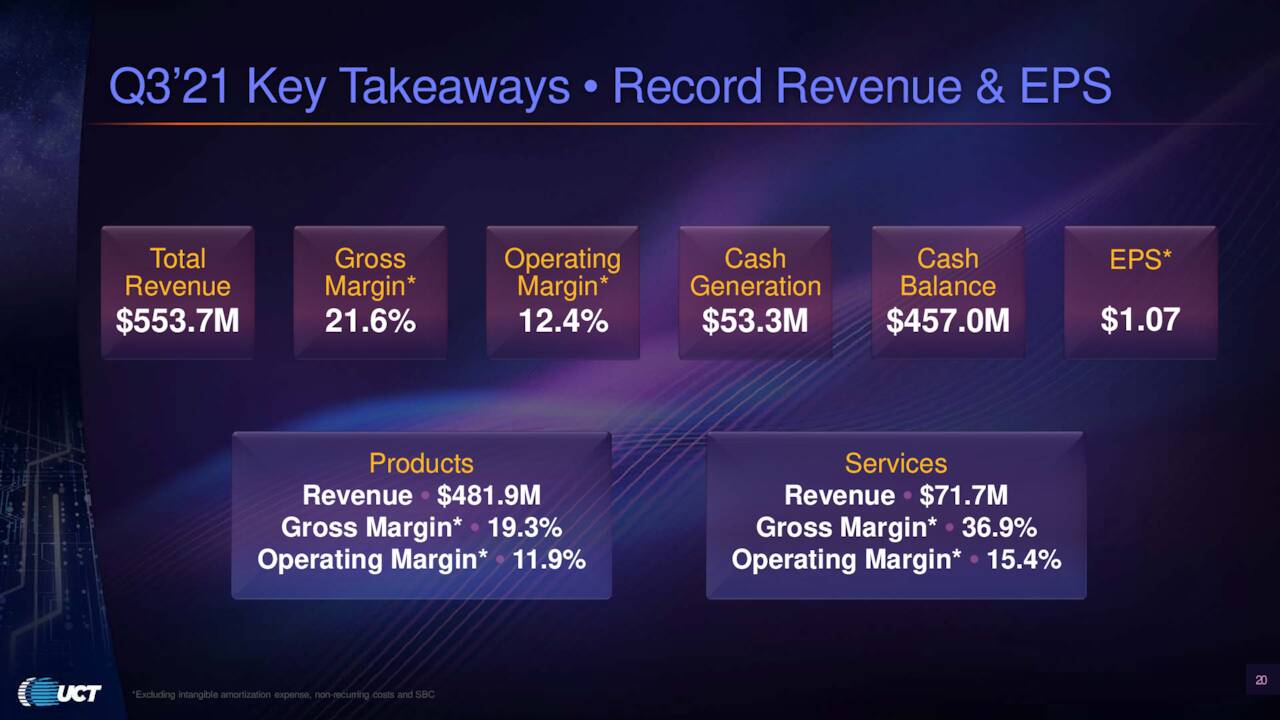

On October 27th, the company reported non-GAAP EPS of $1.07 a share as revenue rose over 52% from the same period a year ago to just north of $555 million. Both numbers were slightly above the consensus. Management guided it expected fourth quarter non-GAAP earnings of between $1.12 to $1.29 a share on $590 million to $630 million in revenue.

UCTT - 4th Quarter Guidance (January Company Presentation)

Analyst Commentary & Balance Sheet:

Surprisingly given its market size, there has been little in the way of analyst chatter around the company in recent months. In September and October, four analyst firms including Needham and Stifel Nicolaus reissued Buy ratings on the stock, but there are no analyst ratings I can find since then. Price targets proffered within those ratings ranged from $66 to $77 a share.

Insiders are frequent and consistent sellers of the stock, with nary a purchase. Insiders sold just under $300,000 worth of shares in January and more than $1 million in November. Most insiders have retained the vast majority of their shares, but in at least two cases, it appears insiders have sold a decent chunk of their holdings. Only one out of every 40 shares is held short currently, however.

UCTT - 3rd Quarter Takeaways (January Company Presentation)

The company executed a $175 million secondary offering in late April of 2021 and ended the third quarter with just over $450 million of cash and marketable securities on its balance sheet after generating more than $53 million of cash in the third quarter. The company has just over $500 million of long-term debt according to this report.

Verdict:

The current analyst consensus has the company earning approximately $4.70 a share on $4.4 billion in revenues in FY2022. This represents almost 15% growth on both metrics off FY2021 levels. This leaves the stock selling at just over 10 times forward earnings and 50% of overall sales.

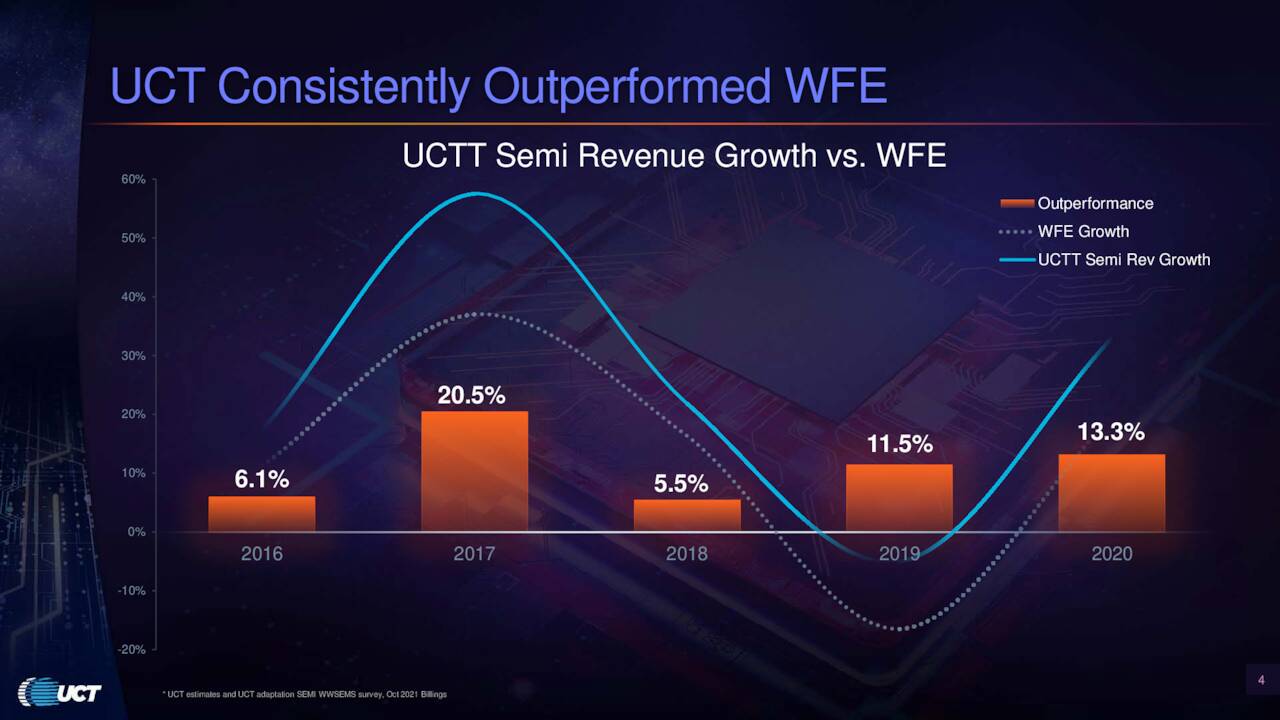

UCTT Versus WFE (January Company Presentation)

These are certainly reasonable valuations given this a cyclical part of the market, and thus mostly always sees a significant discount to the valuation of the S&P 500, except coming off recessions. The company has also nicely outperformed the overall Wafer Fabrication Equipment {WFE} space through all cycles of the past half-decade (above). The stock is approximately 45% below the current median analyst price target on the shares as well.

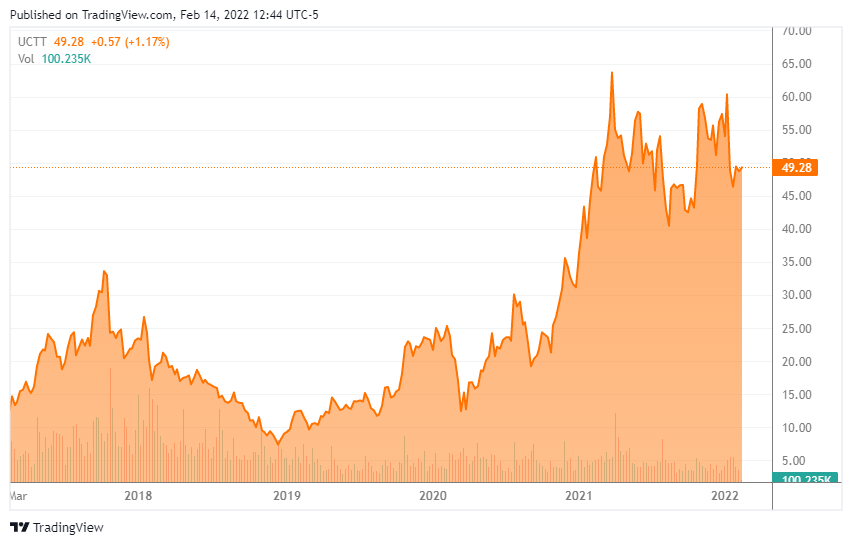

UCTT - Five Year Stock Chart (Seeking Alpha)

That said, this is a highly cyclical industry as the stock chart above alludes to and global growth is slowing. In addition, the company has relied on acquisitions for a good part of its growth over the years (which can be a risky strategy). Like so many manufacturers, the company is seeing supply chain and logistical issues. Shipping/freight charges have gone from approximately 1.6% of sales in 2019 to around 2.5% currently as one example of these challenges. Add in the insider selling and I am probably going to remain on the sidelines on this one until another set of data points gets posted within fourth quarter results in approximately two weeks.

Civilization is the distance that man has placed between himself and his own excreta.”― Brian Aldiss, The Dark Light Years

Bret Jensen is the Founder of and authors articles for the Biotech Forum, Busted IPO Forum, and Insiders Forum

Author's note: I present an update my best small and mid-cap stock ideas that insiders are buying only to subscribers of my exclusive marketplace, The Insiders Forum. Our model portfolio has more than doubled the return of its benchmark, the Russell 2000, since its launch. To join our community and gain access to our market beating returns, just click on our logo below.