JHVEPhoto/iStock Editorial via Getty Images

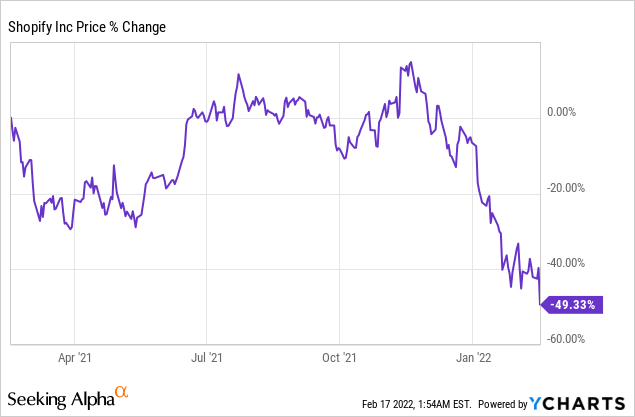

Shares of Shopify (NYSE:SHOP) went through an almost 20% drop in pricing after the e-Commerce company's growth outlook for FY 2022 disappointed yesterday. I believe the market overreacts to the firm's fairly unspecific guidance. Since shares have lost more than half of their value since November last year, Shopify's growth in the e-Commerce market is now undervalued!

Shopify: Still growing rapidly

The e-Commerce company submitted an impressive earnings card for the fourth-quarter that continued to show massive year over year gains in revenues and gross merchandise value. However, the outlook for FY 2022, which assumes slowing growth in the e-Commerce market, spooked investors yesterday. Shares of Shopify went through a near-20% drop in pricing at some point… before recovering towards the end of the trading session.

Before I am going to discuss Shopify's growth outlook for FY 2022, let's have a quick look at the company's achievements in Q4'21 and FY 2021, because they deserve detailing.

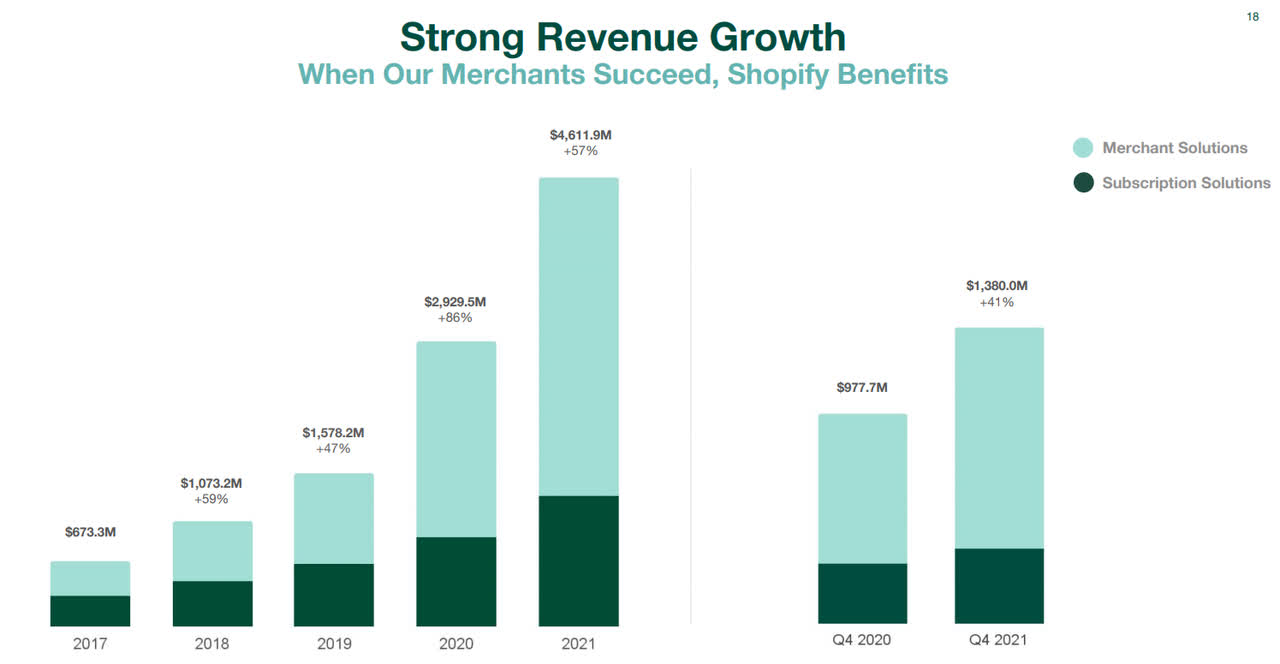

Shopify ended FY 2021 with $4.61B in revenues, showing 57% growth year over year. However, revenue growth for the full-year decelerated year over year -- Shopify grew its top line at a 86% rate during the pandemic year. Fourth-quarter revenues surged 41% year over year to $1.38B due to strong uptake of Shopify's online merchant solutions.

Servicing merchants with online store and payment functionalities remained Shopify's core business in Q4'21. Products and services targeting the merchant market generated $1.03B in revenues for Shopify in the fourth-quarter which calculates to a 75% revenue share. Merchant-related revenues soared 47% year over year and generated the majority of Shopify's top line growth. Subscription revenues, which are basically an aggregation of all of Shopify's monthly online store subscription plans, saw 26% revenue growth year over year. Subscription revenues totaled $351.2M and represented a 25% revenue share in Q4'21.

Shopify

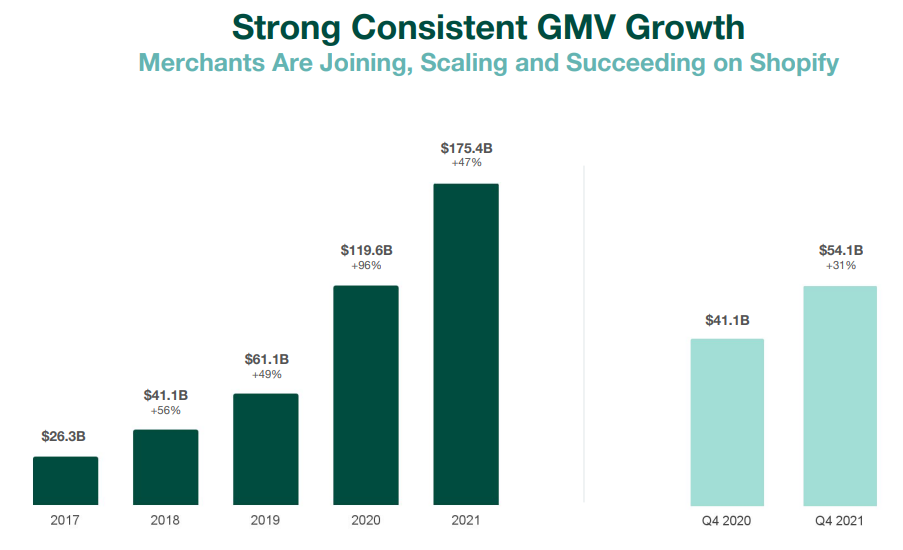

Surging subscription and merchant revenues were the result of after-effects stemming from the COVID-19 pandemic which shifted a considerable amount of traffic and gross merchandise value/GMV to online sellers that use Shopify products and services. As the pandemic waned in FY 2021, growth in gross merchandise value -- the amount of dollars Shopify processes through its ecosystem -- also decelerated. Gross merchandise value still surged 31% year over year to $54.1B in Q4'21 and 47% year over year to $175.4B in FY 2021. The annual rate of GMV growth, however, declined from 96% in FY 2020. While it is true that Shopify's gross merchandise value growth is decelerating, the e-Commerce firm still added a massive $55.8B in new gross merchandise value to its platform in FY 2021.

Shopify

Improving customer monetization

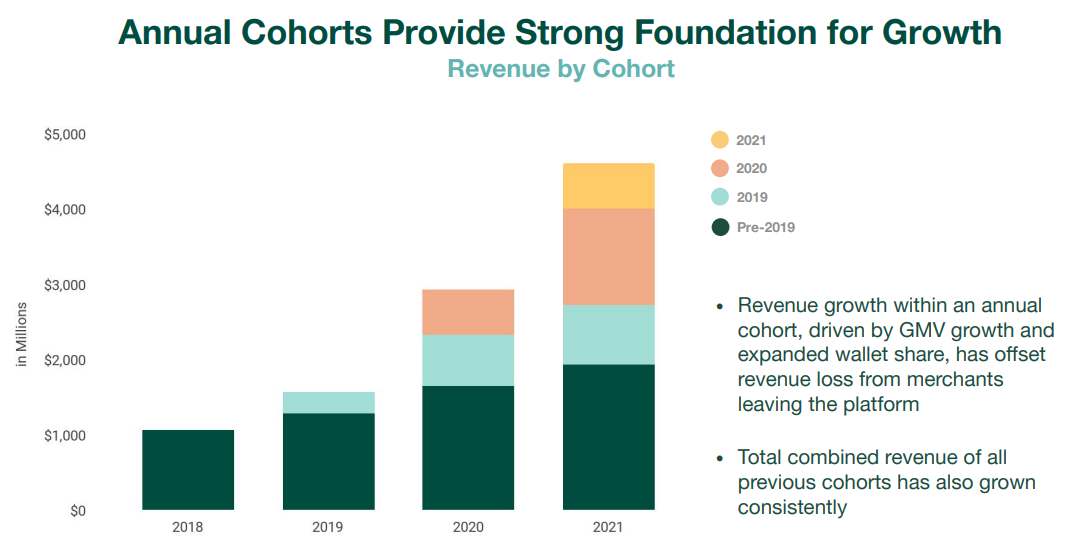

Every e-Commerce platform has churn, meaning customers are either leaving Shopify for other online store solutions or give up the adventure of online selling altogether. Shopify compensates for churn by improving monetization of customers that do stay on the Shopify platform. Shopify's 2020 cohort -- which are new sellers that signed on to the platform for the first time in 2020 -- successively increased their spending in 2021.

Shopify

Outlook for Shopify, discounted valuation

Shopify expects "secular tailwinds" in the e-Commerce market in FY 2022 due to a "more measured macro environment relative to 2021." The e-Commerce company also said in its release that it expects "year-over-year revenue growth to be lower in the first quarter of 2022 and highest in the fourth quarter of 2022", without providing more specific details. What this means is essentially that Shopify expects to see a further deceleration of revenue growth in FY 2022 which would mark the second straight year of slowing revenue growth since the FY 2020 record year.

Revenue expectations for FY 2022 are set at $6.12B, implying 33% year over growth. The e-Commerce company is also expected to scale revenues up to $17.6B over the next five years, implying an average annual top line growth rate of 31%.

Because of the steep drop in pricing shares of Shopify went through since November, the firm's commercial growth prospects in the online store merchant market are now undervalued. Shopify will continue to roll out new products and services that draw new online sellers into its ecosystem which sets the firm up for long term growth in the e-Commerce market.

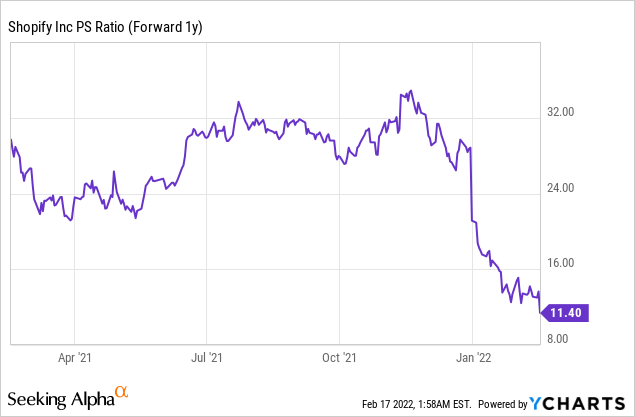

Because of the large drawdown in Shopify's share price, the sales multiplier factor has seen a major down-ward adjustment also.

Risks with Shopify

A growth slowdown in the e-Commerce market is a risk for Shopify and yesterday's market response to the firm's outlook really shows how concerned investors are with guidance.

A slowdown in revenue and gross merchandise value growth has the potential to add pressure on Shopify's already lowered sales multiplier factor going forward. I believe, however, that a normalization of growth rates in the e-Commerce sector after the pandemic is not a reason to panic. Shopify will continue to grow rapidly, especially in the market for online merchant solutions which generates the majority of the e-Commerce company's revenues.

Final thoughts

Including yesterday's drawdown, shares of Shopify have lost 58% of their value compared to last year's high. The guidance for FY 2022 spooked investors and the stock may not trade based on fundamentals short term. In the long term, however, I believe Shopify has the scale and products to service the merchant section of the e-Commerce market well. Shopify's shares are now undervalued and the risk profile is heavily skewed to the upside.