martin-dm/E+ via Getty Images

Global Payments (NYSE:GPN) is a global payment technology company. It offers an established business with steady growth and substantial cash flows. GPN pays a small dividend. It builds payment solutions for issuers, consumers, and merchants. The company is a successful serial acquirer.

Global Payments enables efficient and simple payments processes, regardless of the channel used. It profits from electronic payments through cards, apps, and online. The company has a global footprint across more than 100 countries on every continent. It's one of the most complete behind the scene payment and software solution providers. The biggest enemies of Global Payments are cash and cheques.

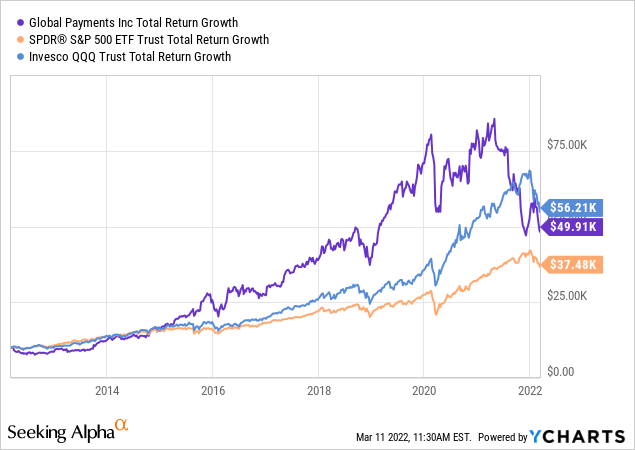

The stock market appreciates the company's expansion strategy, with strong long-term returns. It outperformed the Nasdaq (QQQ) and S&P 500 (SPY) for most of the last decade, except for 2020-2021. The recent underperformance surprises since the company delivered strong results, especially last year.

Potential Price Catalysts

- Robust revenue growth with expanding margins should lead to a fast-growing free cash flow. The company balances shareholder returns with acquisitions.

- Global Payments' exposure to fintech companies and crypto advances quickly.

- A revaluation is due as the company trades below its 5-year average valuation.

Growth

Recent growth looks good. Revenue grew 14.7% in 2021, and adjusted earnings per share jumped 27.5%. The company guided for 9% to 10% revenue growth and 16% to 19% adjusted earnings growth for 2022. It also forecasts an accelerating digital growth post-Covid.

Global Payments has a consistent growth history. It grew revenue per share from $13.98 in 2011 to $29.13 in 2021 at a 7.62% CAGR. It made several acquisitions, of which some were dilutive, so the total revenue grew much stronger at the expense of extra shares. The company keeps obtaining additional companies to strengthen its payment solutions ecosystem further. It signaled the pipeline for further acquisitions is full.

Global Payments

Global Payments built an attractive ecosystem for payments for all its customers. It handles complex cases like the commerce technology for the Mercedes-Benz Stadium in Atlanta.

The company benefits from payment trends online and offline. It has collaborations with distinctive software providers like Amazon's AWS (AMZN), Google (GOOG, GOOGL), and PayPal (PYPL).

Good Pace Of Acquisitions

Global Payments continues its acquiring spree. The company expands its network and reinvests its sizeable free cash flow profitably.

- September 8, 2021: MineralTree adds SaaS business-to-business software-led payments to GPN for $500M.

- July 9, 2021: It acquires merchant services from Bankia (OTCPK:BNKXF, OTCPK:BNKXY) together with CaixaBank (OTCPK:CAIXY, OTCPK:CIXPF).

- May 7, 2021: Acquired customers from Worldline PayOne in Austria in its joint-venture with Erste (OTCPK:EBKOF, OTCPK:EBKDY) and CaixaBank.

- May 4, 2021: Zego, a real estate software, and payment solutions provider, joins GPN.

These acquisitions expand Global Payments' product offering. It also opens up cross-sell opportunities to existing and new customers. GPN proved it could integrate these companies fast and turn them into profitable growth. There is always a clear value proposition with these acquisitions.

For example, Zego was only active in the US. The worldwide presence of GPN allows it to expand geographically. Zego already facilitated $30B in payments annually. Global Payments can also integrate these payments into its ecosystem for synergies.

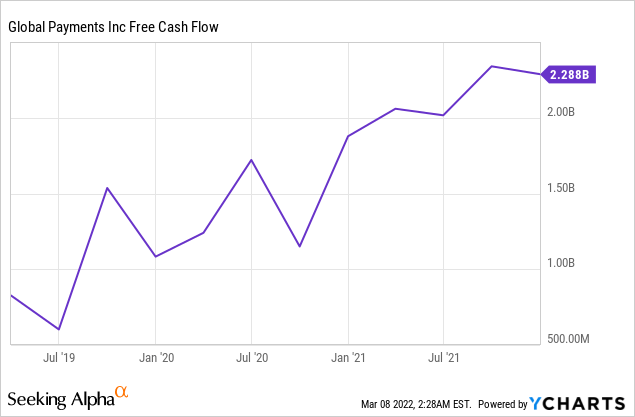

Free Cash Flow For Buybacks, Dividends, And Acquisitions

The continuous growth of Global Payments pays off in terms of cash. The company increased its free cash flow massively over the past few years.

Free cash flow usage balances shareholders' rewards with external growth. The company repurchased $740.8M worth of shares during the third quarter. It has an open buyback program for another $949.2M. It also pays a $0.25 quarterly dividend, a 0.68% dividend yield. The dividend picked up since it acquired TSYS and pledged to continue its dividend. It seems like the company will regularly increase its dividend.

Over the past year, it spent $2.5B on strategic transactions and $2B on shareholder returns. It's more than the trailing free cash flow and gets funded by additional debt. The increased results keep its leverage ratio stable.

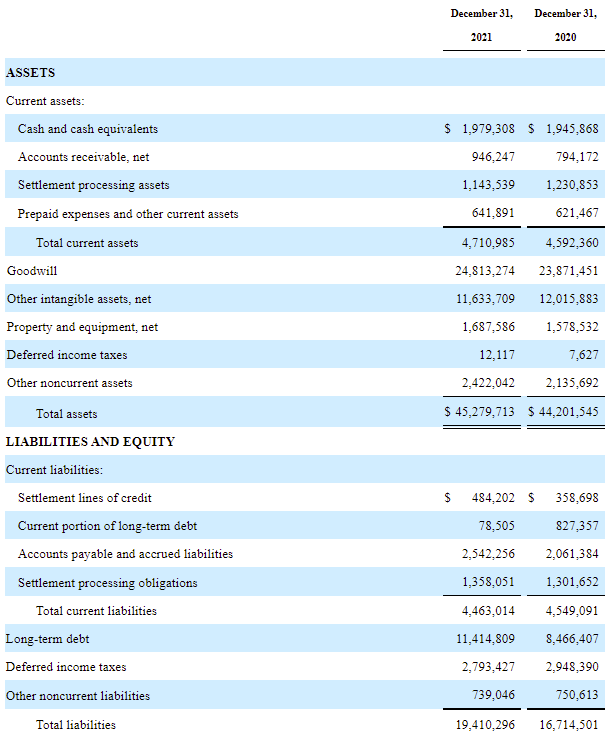

Balance Sheet

The balance sheet shows the acquisition activity of GPN. It has a lot of goodwill and intangible assets on its balance sheet.

Global Payments 10-K

The company writes off these intangibles quickly. That's why there is a big difference between its GAAP EPS and adjusted EPS. Overall, the balance sheet looks good with ~$2.35B in liquidity. As mentioned before, it funds acquisitions with debt. The leverage position of 2.6 is good and leaves room for cash acquisitions.

The considerable goodwill and intangibles position is one of the most significant risks to GPN. It has managed these very well so far.

Valuation

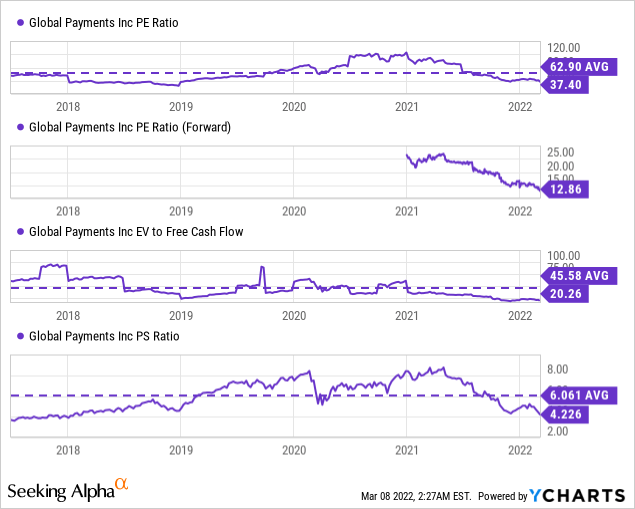

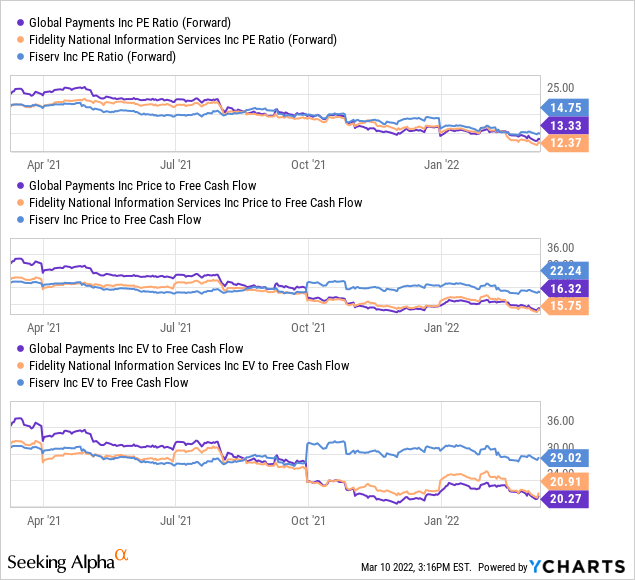

Global Payments looks expensive on GAAP net earnings. These are misleading as the amortization of intangibles has a prominent effect on these earnings. Based on analyst estimates, the forward P/E coincides with expected adjusted earnings.

GPN looks cheap against its past valuation. The company increased its profitability and produced sizeable free cash flows. The EV/FCF ratio shows the improved profitability perfectly. It only trades at 20.2 against an average of ~45 over the past five years.

There isn't a good reason for the current discount of GPN.

Possible explanations are upcoming payment processes and the competition of cryptocurrencies. Upcoming payment processes don't look threatening to GPN. The company is a backbone for many systems and should get its share of new apps. GPN's complete offering and global presence are tough competition.

Cryptocurrencies' future as payment systems is still unsure. GPN and PayPal's relationship includes the support of cryptocurrencies recently. So the competition from crypto is uncertain.

As I've stated before, the possible new competition isn't threatening GPN. The biggest enemy is cash payments.

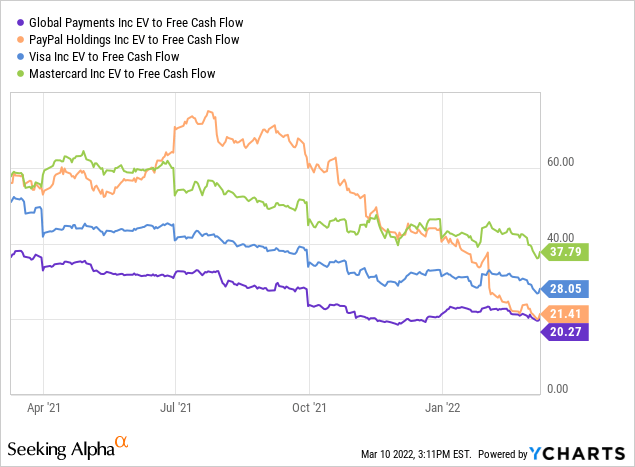

Comparison To Other Payment Providers

Visa (V), Mastercard (MA), and PayPal aren't in the same business as Global Payments. These are front-end providers of credit cards and payment apps. The competition of new payment systems and crypto applies to these as well.

I think the EV/FCF sketches a clear picture. They move in the same general direction as they are all payment providers. The discount increased in 2021 for GPN. Again, there is not a good explanation other than market mispricing.

PayPal dropped significantly in valuation due to its recent earnings with guidance below expectations.

The sell-off of similar payment providers unjustly hit GPN harder than others. It received a premium in the past and now trades at the bottom range of competitive services like Fidelity National Information Services (FIS) and Fiserv (FISV).

Conclusion

Global Payments is reasonably valued for its growth. The company showed strong free cash flow results, and the outlook is also promising. An expanding multiple would make sense, but even just the expected growth makes for a bright future.

It profits from structural trends towards card and digital payments. It expands quickly with an accretive acquisition strategy. The company has the right balance between shareholder returns and adding growth.

Join me at Green Growth Stocks for more high-growth investment ideas. I offer access to my model portfolio, growth ideas with price targets, and a live chat. I cover high-growth opportunities with thorough research that can change your life.

Discover my best ideas in the fast-growing green sector in the USA and the world. Don't miss out and subscribe today with a 14-day free trial!