CHUNYIP WONG/E+ via Getty Images

"Its not the critic who counts; not the man who points out how the strong man stumbles, or where the doer of deeds could have done them better.....the credit belongs to the man who is actually in the arena....." Theodore Roosevelt

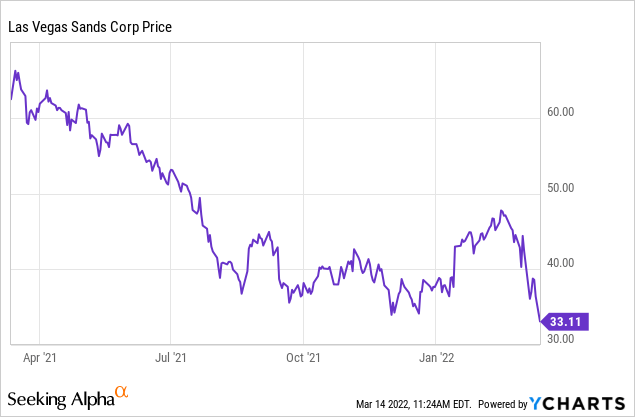

Let's stipulate first that I'm among those who have sung the praises of Las Vegas Sands (NYSE:LVS) as it climbed all the way up to its high last March of $63.71. At that time and beyond, I was guiding the stock to a PT in the $80 to $90 range. Since then, the stock has tanked, along with the entire Asia facing gaming sector down to $34.42 at this writing.

Latest news out of China further muddies the recovery waters for LVS. Though isolated mostly in the north but also hitting Shenzhen, the outbreak of new COVID cases will add to headline bearish outlooks ahead. What is different than 2020, however, is that 85% of China's 1.4b population has been vaccinated - according to Beijing. That means that recent rumbles that the zero-tolerance policy on Covid was under consideration for easing - great news for the Macau sector - is likely to remain in place. That is the single biggest factor in the sell-off.

My bullish outlook, plus those of other analysts, was compounded of many signals that assumed we were at least on the cusp of the endgame of the pandemic. That was before the Omicron variant gripped the globe. But despite that, I remained bullish entirely based on fundamentals: LVS's superb asset base in the globe's biggest gaming markets, its clean balance sheet, the sale of Vegas assets adding a mountain of $6.2b in cash to the coffers and the prospect that LVS would be announcing the development of a major integrated resort in a third Asian country. LVS also has been on the record deep-diving into the digital gaming space, i.e., sports and casino online gaming.

Just this week, CEO Goldstein told investors that the company was moving closer to a decision on a third Asian country to develop an IR. Against a growing tide of investor discomfort with the post-Adelson management team, I remained steadfast in my conviction that sooner or later their ground rooting gaming strategy would pay off big time.

Google

For certain it has been tough remaining bullish on the stock through the sharp decline. But I still take the long view that LVS is massively undervalued and that it's a hard case to make if you look at the current prospects for the stock. So is it time to throw up the white flag? There's a case to be made for that. But I have looked at the stock again, through a different prism and come out swinging again: At its current price, it's a buy.

I won't hide behind Omicron here to fully explain my failed fandom on the stock - thus far. For all analysts, it always comes down to a batting average. I only cite this to own the miss - but also to put it in context for my continuing belief that the stock has fallen enough to keep my buy guidance intact. There's another way to look at the stock beyond standard metrics we all live by.

That's because no matter what any analyst says, those right and those proved wrong like myself, such measures of performance have limited value for investors. It's because no algorithm I know can ever bake in the prospects for a sudden act of nature that sends a tsunami of damage across an entire sector.

Those who remain bearish on LVS are leaning on metrics and headlines - understood of course. But to me, that's at odds with the real world prospects of the stock, namely at its current price, in real terms.

Google

In a way, it's a Carl Icahn moment. His stock in trade since day one has been guided by the same "fallen angel" strategy applied to bonds he applies to stocks. He's used that to spot undervalued stocks and that's what formed the basis for his victories that brought him to an estimated net worth of $17b at writing. Central to his thesis is that a given stock is mostly undervalued because its top management is overpaid, overvalued, and stuffed end to end in the conference room with inept, old boy networks. That's not the case with LVS.

As a former industry colleague of CEO Goldstein, I can confidently assert here that while much is unpredictable here, blunders will not be made by him and his team. (Some investors believe selling the Vegas assets was a blunder. I think it was primarily a move to prepare for a third Asian IR, which could cost $4b at least.)

So we apply that approach to LVS right now. We see it, as a common stock with the characteristics of a bond dubbed a "fallen angel." Interestingly, LVS debt has recently been slightly downgraded a tick by Moody's due to the delayed recovery of the endgame of the pandemic.

The "fallen angel" analogy: A bond strategy applied to LVS

In brief, the fallen angel designation is traditionally assigned to bonds issued and traded as investment grade, that for one reason or another related to its issuers business is downgraded by the rating services. Such bonds usually take swan dives in the bond market. Astute traders on the prowl for such bonds find ones they believe to have recovery built into their business models, swoop in, load up and wait.

In a study of this factor, MoneyTalk has found that over time fallen angel bonds correctly picked show an accumulated return over time of 9.1% vs. 5.3% at issuance and ~6% for globally traded issues. When I was part of senior management at the former Trump Taj Mahal in Atlantic City, we were forced into a prepackaged bankruptcy situation in 1991.

The culprits here were the disastrous performance of the prior senior management group - among other factors. Our bonds tanked way down to 40, or 50ish. Icahn came in, bought tons and waited. Once we were able to put our new operating team in place, it ignited a healthy spike in our share of market and EBITDA. The bonds soared. Icahn walked away with tens of millions in the process. No, our original bonds were not investment-grade per se, but they had been snapped up when issued based on the property debuting in a healthy market with the biggest capacity, and the Trump name which then had significant currency on Wall Street.

In looking at LVS again, I see an analogy. Clearly, it's not perfect. But I think it's a different perspective in judging whether the stock qualifies in its own way as a fallen angel. Just prior to the COVID disaster, LVS's 2019 results were solid:

Net revenues: $13.7b

Net income: $2.6b

Assets: $23.1b

Long-term debt: $12.4b

Cash and cash equivalents as of 12/19: $4.2b

Returned to shareholders: $3.1b

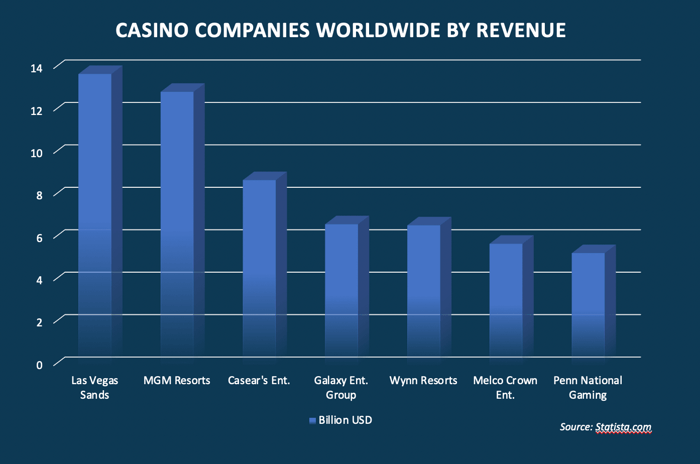

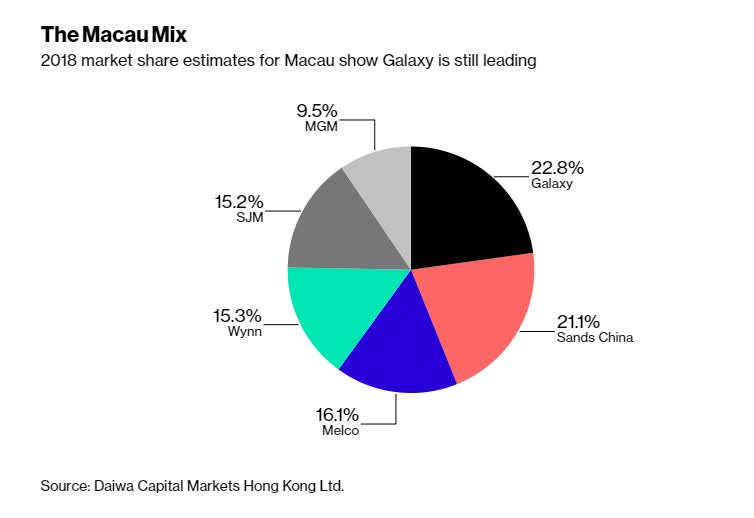

Share of Macau market: ~22% and growing

Total Macau market: $37.7b

Singapore: A duopoly between LVS and Resorts World Sentosa, now extended to 2030

Stock at end of December 2019: $63

For purposes of this discussion let's say that pre-COVID LVS was about as close as a casino company could realistically be to an investment quality valuation in its sector. It was, by many measures, an angel at $63 a share with an upside based on a transformation of its Cotai Central properties in progress and its ongoing expansion in Singapore. Its then Vegas business was performing well to boot.

Since then, with the pandemic taking its toll, the stock has fallen ~50% presenting investors with the same choices as bond traders do when deciding to either buy or pass on fallen angel debt. Clearly, when bonds are downgraded, there's a sell-off. Many institutions handling pension funds, for example, are subject to guard rails against holding bonds that fall below a given rating. Add to that the frenzy that always accompanies headlines about Fed actions anticipated, etc., and a bond may take a significant nose-dive.

Or there are those who simply won't touch fallen angels no matter what the discount off issuance does for yield. If we apply this theory, new flawed to an extent, but viable, to LVS common, we see the same choice.

Here are the questions to be asked before acting:

What are the prospects that the company's business model is sound going forward? Does it have a viable customer base? What's its share of market? What's our belief that the factors that caused a downgrade of a company's top-quality debt will continue to haunt it? Is the downgrade based on rational expectations that the events that caused it will continue to injure its credit standing?

Let's apply the answers to LVS:

The company's business model, the integrated casino resort offering gaming, rooms, entertainment, shopping and ongoing attractions deployed in the globe's single largest gaming markets will revive post-COVID to at least pre-COVID levels by 2023/4 or before. That we believe is beyond challenge. Attempting to forecast the path of COVID in the next 18 months is a fool's errand. But to believe that, given the state of inoculation in China and other Asian nations that feed Macau and Singapore, we will experience anything close to 2020 seems wrong as well. Global response will be quick, vaccination levels are high. That's all we can say. And that's part of the bet you make on the stock if you decide that it is, indeed, at $31 a fallen angel. No matter when we see viable trending of the end of COVID and high levels of protection against future outbreaks anything like 2020, that is a realistic expectation for making a bet on LVS now.

Lingering in the wings as it were is the very real question investors may well ask: Is $34 rock bottom here? Does bad news on COVID or other negative headlines, indicate the stock can trade lower? Is it still a wait-and-see stock? Could there be another 50% correction lying in the weeds here? So let's take a pass and sit on the sidelines, goes the mantra of many investors with whom I exchange opinions on LVS.

Our bottom line:

We continue to believe that, in many senses, LVS, among peers in the sector, is a fallen angel and as such holds the potential for great rewards downstream for those with the risk profile of bond traders. We also believe that while one can never accurately forecast bottoms, we think LVS offers a reasonably good bet that it is at or very near a bottom here.

One-year analyst target at writing: $52.

Our PT based on a "fallen angel" bet is $66, down from our highest prior PTs of $70 to $80 prior to the Omicron outbreak.

For in-depth and deep dive research on the casino and gaming sector, subscribe to The House Edge. New: Free excerpts from our book in progress "The Smartest ever Guide to Gaming Stocks" - free to existing members and new subscribers.