whitebalance.oatt/E+ via Getty Images

As economies around the world recover from the pandemic, Uber Technologies Inc. (NYSE:UBER) has observed solid rebound patterns in revenues and bookings. Unfortunately, Uber is a highly unprofitable company with a track record of terrible losses.

The longevity of losses, as well as the extent of Uber's cumulative deficit, weighs more heavily at this point than, say, booking recovery patterns. Furthermore, Uber faces significant investment risks due to the company's operational industry. This can only lead to one conclusion: Uber is a value trap.

Diversified Business Model With An Incredible Amount Of Losses

Uber began in the ride-sharing market, but the company's economic model has changed considerably in the last several years. Uber's business portfolio is divided into three sections: Mobility, Delivery, and Freight.

Uber has benefited from strong recovery trends in its Mobility division. Uber's Mobility sector consists mostly of income from Uber app-booked rides from point A to point B. Uber's second category, Delivery, covers the delivery of necessary supplies to consumers' doorsteps, such as food. After the first Covid-19 instances hit the global economy in 1Q-20, the Mobility industry, in particular, has seen a solid recovery in gross bookings. The Delivery Segment benefited from the epidemic since more food delivery orders were placed during this time period.

Weekly Delivery And Mobility Gross Bookings (Uber Technologies)

Uber's gross bookings represent the total dollar value collected from customers across all segments, including taxes, tolls, and fees. A strong increase in gross bookings began in 2Q-20, at the commencement of the pandemic, and total gross bookings jumped 159% to $26.5 billion in 1Q-22. Gross bookings increased by 35% YoY in 1Q-22. The Delivery business currently accounts for 53% of total gross bookings, with the Mobility business accounting for 41%. The remainder is freight services.

Gross Bookings (Uber Technologies)

Only Adjusted Profits

While recovery trends appear to be positive on the surface, Uber's main issue is that the company can only attain profitability on an adjusted basis. Many new businesses face this issue for obvious reasons: they are not yet established.

However, Uber has been operational for more than a decade and profits are still elusive. Uber began operations in 2009 and became public in 2019. You'd think a corporation like this would be able to turn a profit by now, especially now that the Covid-19 pandemic has ended, and operational conditions have returned to normal.

Unfortunately, Uber is not one of them. The company's latest profits demonstrated once again that it is incapable of generating true profitability. Uber's adjusted EBITDA in the first quarter was $168 million. Due to 'other expenses', actual net income was negative $5.9 billion.

Financials Overview (Uber Technologies)

Other costs include investment profits and losses from Uber's investment division, which seeks stakes in firms relevant to Uber's operational business. Uber reported a $5.6 billion investment loss attributable to equity investments in its ‘other costs’ in the first quarter. Uber has made investments in firms such as DiDi Global (DIDI), China's leading ride-hailing startup; Zomato, which bought Uber's food delivery business in India in 2020; and ride-hailing giant Grab (GRAB), which provides transportation and delivery services in Southeast Asia.

Uber’s Investment And Operating Risks Are Positively Correlated

Uber's equity book has the potential for enormous returns, but also high losses, as we recently learned. Aside from the prospect of massive losses, there is another issue with Uber's investments.

Uber's investments are primarily focused on the same industry in which it operates. That is, if the running firm suffers a downturn, such as a recession, the value of Uber's stock investments will almost certainly have to be reduced as well. If Uber's core businesses, Mobility and Delivery, experience macro challenges, this link of stock risk and operations risk might become a major issue.

Investments (Uber Technologies)

The $5.6 billion losses indicated previously were caused by significant drops in DiDi and Grab values in the first quarter. If prices continue to decline, Uber will be obliged to reduce the value of its equity position.

Investments And Fair Value Measurement (Uber Technologies)

The concentrated nature of Uber's investment book, along with operational underperformance, resulted in a $5.9 billion loss in 1Q-22, bringing the company's aggregate deficit to $29.6 billion. In Uber's existence, shareholders have supported about $30 billion in losses, which is, to put it kindly, dismal and not exactly a fantastic sales presentation to entice investors to buy the shares.

Interests And Equity (Uber Technologies)

The Price Is Too High

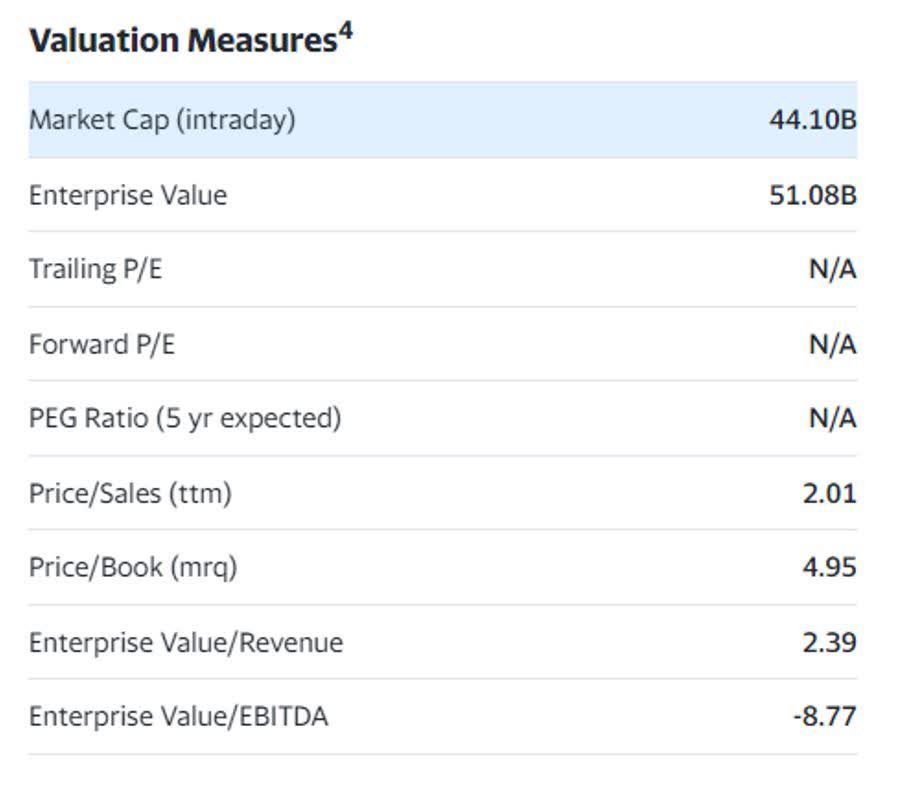

Based on this year's revenue, Uber's P/S ratio is 2.0x, while its P/B ratio is 4.9x. Both multiples indicate enormous overvaluation because the company is not profitable and will most likely not be profitable for a long time. Lyft (LYFT) has a P/S ratio of 1.8x and a P/B ratio of 5.5x, and it is likewise a firm that I would not consider buying.

Valuation Measures (Yahoo Finance)

Why Uber Could See A Higher Stock Price

Uber has been in operation for over a decade and still remains highly unprofitable. This could or could not change in the future. If it does, investors may be ecstatic at the idea of owning a piece of one of the world's most inventive corporations. A rebound in equity valuations could boost Uber's earnings. Having said that, I believe Uber will stay unprofitable for at least another couple of years.

My Conclusion

Uber is a value trap, given its history of enormous losses. Investors will have to recuperate $30 billion in losses over the duration of the company's lifetime before they see a dime on their investment.

Furthermore, equity and operating risks are strongly associated because one would expect DiDi Global and Grab to experience comparable issues if Uber's Mobility and Delivery division suffered revenue hurdles due to a recession.