Jay Yuno/E+ via Getty Images

Investment Thesis

Global Payments Inc. (NYSE:GPN) is mostly a third-party payment processing company that owns the payment network, acts as an acquirer, and "facilitates" the rest of the payment process between merchants, card issuers, and paying consumers. Since it does not issue credits in the payment process, it does not bear any credit risks of payment default, making it relatively less risky as an investment compared to credit-issuing banks.

GPN has a profile of increasing top and bottom lines that is achieved by issuing massive volumes of shares to acquire other companies. While the acquisitions make sense "strategically", it leads to shares' dilution which is less ideal for investors compared to using cash.

The company does not have a significant edge in terms of overall financial profitability when compared to its closest competitors. Investors should wait and see who eventually emerges as the winner of this consolidation in the larger payment industry.

The stock is currently undervalued but without a clear winner in sight after the industry-wide consolidation, I maintain a hold rating on GPN.

Company Overview

GPN operates in 3 main segments, Merchant Solutions, Issuer Solutions, and Business and Consumer Solutions. From the company's annual report, these are the services that it provides.

- Merchant Solutions segment - The company provides its core offerings of "authorization, settlement and funding services, customer support, chargeback resolution, terminal rental, sales and deployment, payment security services, consolidated billing and online reporting" to the merchants.

- Issuer Solutions - The company provides solutions to "enable financial institutions and retailers to manage their card portfolios, reduce technical complexity and overhead and offer a seamless experience for cardholders on a single platform". They also provide solutions to "support business-to-business payment processes for businesses and governments".

- Consumer Solutions - The company provides consumers with "general purpose reloadable prepaid debit and payroll cards, demand deposit accounts and other financial service solutions to the underbanked and other consumers and businesses in the United States". Additionally, the company also provides "2B payment services and SaaS offerings that automate key procurement processes and enable virtual cards and integrated payments options"

Basically, aside from payment fees collected for every transaction settled, the company receives additional streams of revenue for providing a suite of "value-added services" to facilitate and improve the whole payment experience.

Non-Exposure to Credit Risks

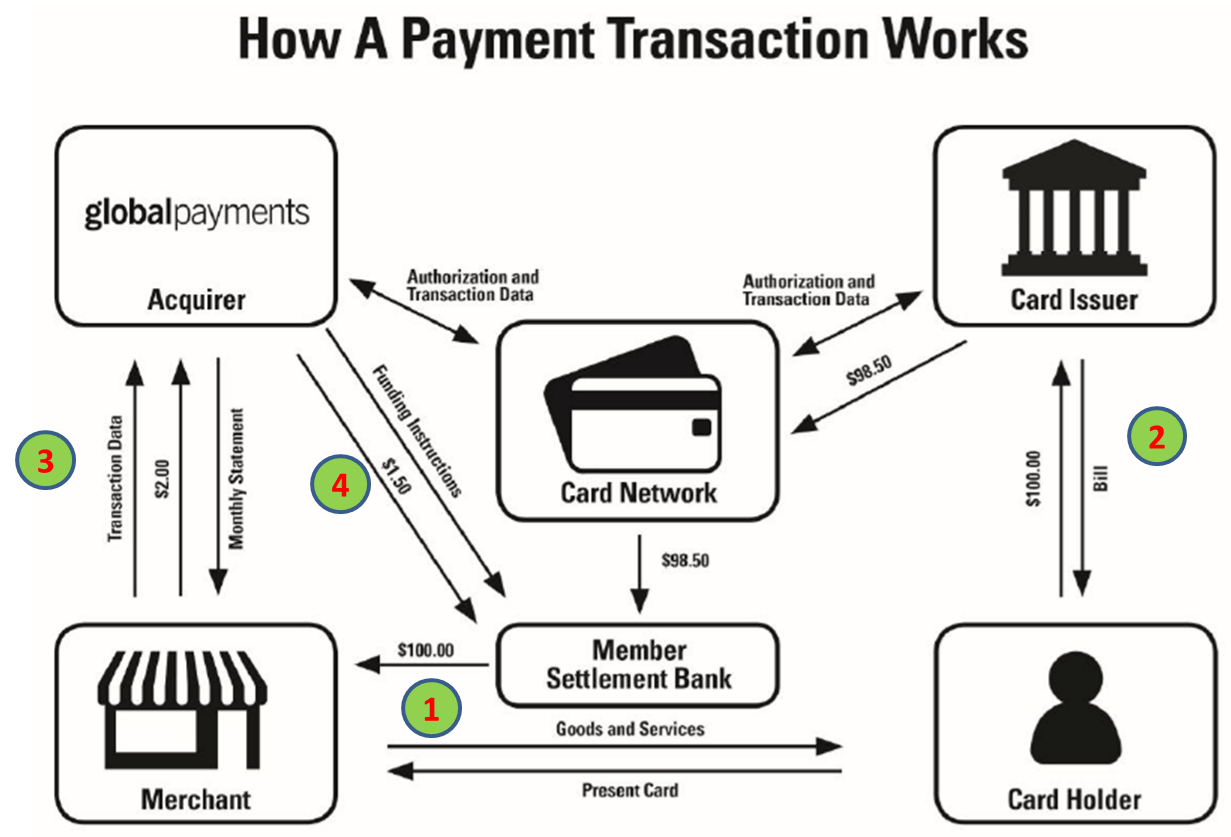

To better understand the role GPN plays in a typical cashless transaction, we can analyze a mock transaction scenario described in the latest annual report.

Annual Report 2021

In this mock transaction:

- A transaction of $100 is made using GPN's payment processing network. After the transaction is approved and settled, the participating merchant gets $100

- The card issuer bills the cardholder $100 for the purchase made in point 1.

- The acquirer, GPN in this case, charges a merchant discount rate (or MDR) of 2%, which amounts to $2.

- From the MDR amount, the "member settlement bank", which is also the credit-issuing company, gets $1.50 as an "interchange fee". Eventually, GPN gets $0.50 for the $100 transaction amount.

The interchange fee is based on the interchange rate set by the member settlement bank which is usually also the card issuer. This is to compensate the settlement bank (credit issuer) for incurring the credit risks and other charges associated with typical payment transactions.

We can see from this example that GPN is primarily taking on the role of the merchant acquirer and interacting with other players in the transaction process through its payment processing network. The credit risk will be born by the credit issuer, GPN does not. That means GPN is not exposed to the risk of credit payers defaulting on their payments. From an investment perspective, this is a positive sign.

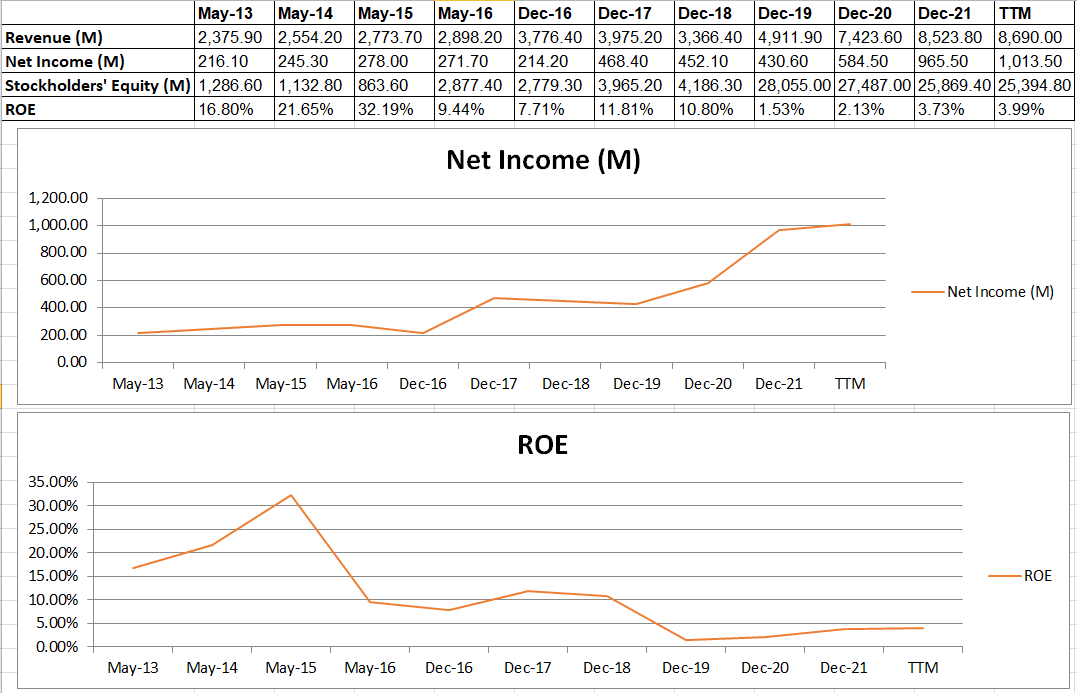

The divergence between Net Income and ROE

GPN is very profitable with top and bottom lines generally increasing for the last 10 years. While its net income is increasing year after year, the ROE, in contrast, is decreasing during the same period creating a very stark visual divergence when displayed on the chart.

Plotted by Author using Seeking Alpha data

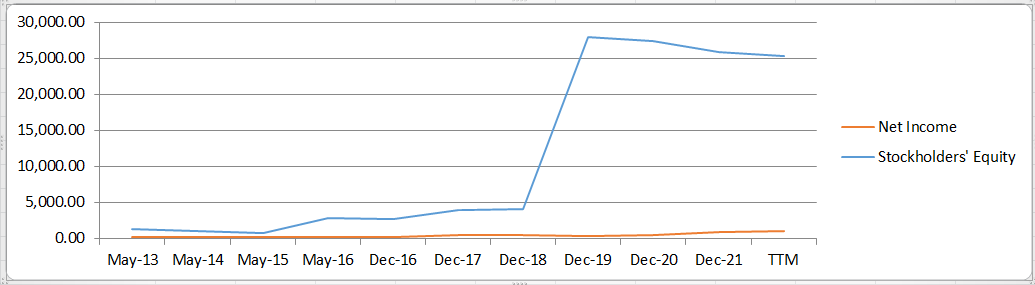

ROE is generally derived from net income but denominated by shareholder's equity. That means the company has been selling/issuing a lot of shares which dilutes shareholders' returns. Indeed, if we overlay the stockholders' equity trend with Net Income, the greatest increase in equity was in 2019. This is a concern for investors and needs to be explored further.

Plotted by Author using Seeking Alpha data

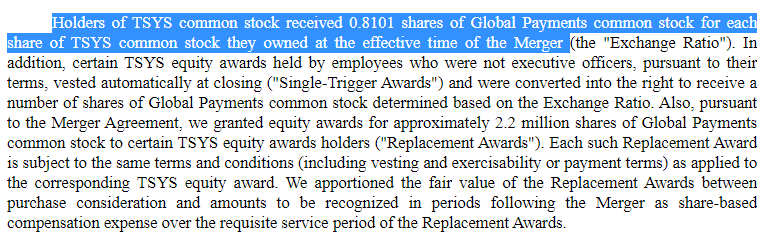

We can infer from the latest annual report that GPN acquired Total System Services, Inc in 2019 for about $24.5 billion, and holders of TSYS were issued shares of GPN, resulting in the greatest rise in total stockholders' equity for GPN.

Annual Report 2021

I also noted that:

- Before the acquisition, TSYS was the largest third-party payment processor in North America.

- After the acquisition, GPN has now taken on this market leading status as stated in its latest annual report: "As of December 31, 2021, we believe that we were the largest third-party processor for credit card issuers in North America and one of the largest in Europe based on net revenue from solutions provided to credit card issuers."

While I agreed that this acquisition is the right strategic decision for GPN to significantly expand its competitive advantage, ideally, it would have been more financially prudent (for the benefit of investors) if GPN has acquired TSYS using cash instead of company shares.

Competitor Analysis

The company list the following as the main competitors in its latest annual report:

- Fiserv, Inc. (FISV)

- Fidelity National Information Services, Inc. (FIS)

- Chase Paymentech Solutions, owned by JPMorgan Chase, an investment bank

- Elavon, Inc owned by U.S. Bancorp (a "US Bank")

- Wells Fargo Bank (a "US Bank")

I believe it is more meaningful to exclude banks and just compare GPN with other "third-party payment companies" of FISV and FIS.

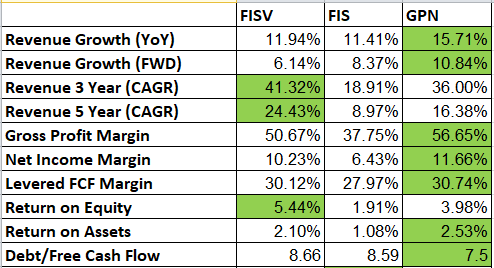

Seeking Alpha Data

From this table, we can infer that:

- In terms of revenue growth, FISV appears to be growing faster in the long run of 3 and 5 years, but GPN appears to be growing faster in recent and in the projected "forward-looking" years. Overall, I consider all 3 competitors to have roughly the same growth momentum around 20% depending on the time frame you are looking at.

- As we drill down further to observe the gross, net, and FCF margins, GPN appears to have at most just a "razor-thin" edge over FISV, which in my opinion, is not significant.

- All 3 competitors appear to have generally low ROE and ROA of roughly low-single to mid-single in percentage value. This suggests all 3 competitors are likely engaged in a similar strategy of growth using massive sale/issuance of shares to acquire other businesses.

- All 3 competitors have debt volume that is roughly 8 times their FCF.

Financial comparisons between competitors suggest GPN is just on-par with its peers in terms of overall financial profile. Generally, the whole payment industry is in a state of consolidation. From this comparison of financial performance, we are not able to pinpoint a player with a clear advantage that will likely dominate the industry after the consolidation.

To get a sense of how prevalent mergers and acquisitions (M&A) are in the payment industry, here are some notable mergers in the last 18 months before the end of 2021:

- Global Payments bought TSYS (as discussed earlier)

- FIS acquired Worldpay

- FISV acquired First Data

GPN had the intention to merge with FIS in 2020 but the plan was eventually called off without any official reasons. Given that such M&A allows all parties to greatly benefit from reduced operating costs, it is likely GPN and/or its other peers will be planning for another M&A of a similar capacity sooner rather than later.

Investors should closely monitor the financial impact of these recent and future M&As before deciding whether the resulting merged/acquiring companies are still worthy of an investment.

Valuation

This is the trend of the company's FCF over the last 5 years:

Calculated by Author using Seeking Alpha data

We can observe that:

- After the acquisition of TSYS in 2019, GPN experienced an explosive growth of more than 100% from 2019 to 2020.

- This growth is not sustainable and the growth normalized to slightly more than 20%. That means assuming GPN stops acquiring any new companies, the normalized growth rate should be around 20%

- Moreover, in the previous section, I made this observation about revenue growth: "I consider all 3 competitors to have roughly the same growth momentum around 20% depending on the time frame you are looking at".

Hence, it appears that generally, 20% of growth is a reasonable range to use in our valuation model.

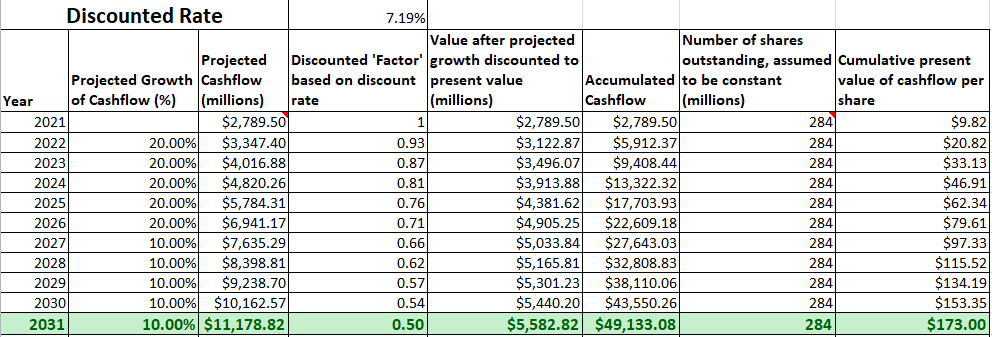

We will make the following additional assumption when evaluating the intrinsic value of the company:

- GPN will grow at 20% for the next 5 years.

- GPN tapers in growth by half, therefore, growing at 10% from year 6 to year 10.

- Since the payment industry is currently undergoing massive consolidation, I will assume GPN will only exist for the next 10 years and terminal value will not be considered for my valuation.

- The value of levered free cash flow to be projected is $2789.5 million, taken from the end of 2021.

- The discount rate is estimated to be 7.19%.

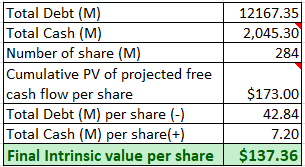

- The total debt of the company is the sum of "Short Term Debt" and "Long Term Debt" which works out to be $12167.35 million.

Calculated by Author

Based on the above inputs, the present value ("PV") of projected free cash flow per share for GPN is $173.

Calculated by Author

Taking into account the total debt and cash that the company is holding, the final intrinsic value is $137.36.

The current price of around $122 implied the stock is currently undervalued.

Investment Risks

GPN is mostly growing as a result of massive acquisitions instead of investing in organic growth. The payment industry appears to be going through a period of consolidation with lots of mergers and acquisitions in the next few years. GPN's future growth depends very much on who will be the eventual dominant players at the end of this consolidation. Until the dominant players become clearly visible, my rating for GPN shall remain as 'hold'.

Conclusions and Key Takeaway for Investors

As the largest third-party payment processor in North America, GPN has a respectable competitive advantage over its competitor for now. It is also undervalued. However, the industry is in a state of massive consolidation. I believe the most prudent decision for investors is to wait and see the outcome of these consolidations before deciding whether GPN is a worthy investment.