kuriputosu/iStock via Getty Images

We recommend investors buy Texas Instruments Incorporated (NASDAQ:TXN) at current levels as the company has already lowered estimates, and the stock is pricing in some bad news. Our optimistic outlook on the stock is based on TXN's exposure to diverse high-growth market sectors. With the recent market sell-off, TXN stock is close to bottoming, and analysts' estimates on the stock have already been lowered. We believe TXN's large size and reach into all sectors of semiconductor markets will sustain it and position it for growth in the coming quarters.

TXN is playing the long game

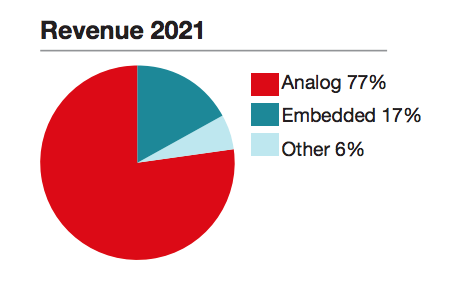

TXN's size and reach did not appear out of thin air; the company's been in the semis field for decades and plans on staying in it for decades to come with a culture focused on "long-term ambitions." TXN designs and manufactures semiconductors that are sold to electronic designers and OEMs (Original Equipment Manufacturers). The company mainly operates in two segments: analog and embedded processing. TXN makes 77% of its revenue from analog devices, 17% from embedded devices, and the remaining from the other segments. The top two segments are forecasted for significant growth in the coming years, and we expect TXN to benefit from this growth. This graph shows the revenue breakdown at TXN in 2021.

TXN

The Analog Integrated Circuits (ICs) market is expected to grow at a CAGR of 5.5% from 2021 until 2026. We are confident about analog's growth because there is a growing need for analog chips to provide power management to run devices.

In the most recent quarterly earnings of 1Q22, TXN analog sales grew 1.5% Q/Q to $3.82B, and the embedded processing sector is also up 2% to $782M on steady demand. 1Q22 earnings report a 19% increase in revenue compared to 1Q21, driven by strengthened demand in industrial and automotive markets. Analog revenue grew 20% Y/Y, and embedded processing grew 6% Y/Y. TXN holds a growing position within the semiconductor field, and we believe its exposure to analog business, specifically power management, will maintain its stronghold and advance TXN's long-term strategy.

TXN is the 800-pound gorilla in the market

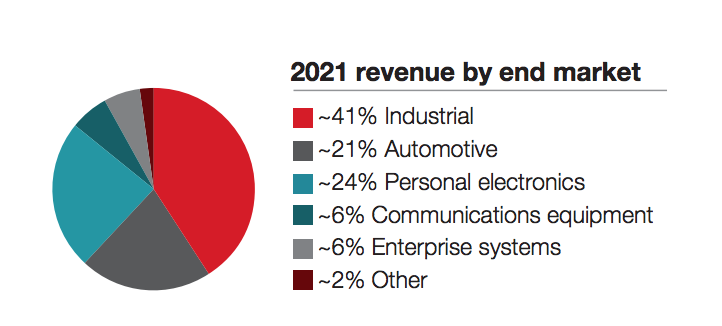

TXN has deep roots in the semiconductor market. TXN's appeal is that it leaves no stone in the semis field unturned. TXN has exposed itself to all industry sectors and capitalized on the high-growth markets within analog semiconductors, mainly industrial and automotive. The industrial market is TXN's largest and most diverse growth market. The industrial market reaches 13 sectors (including power delivery, motor drives, lighting, industrial transport, etc.).

TXN

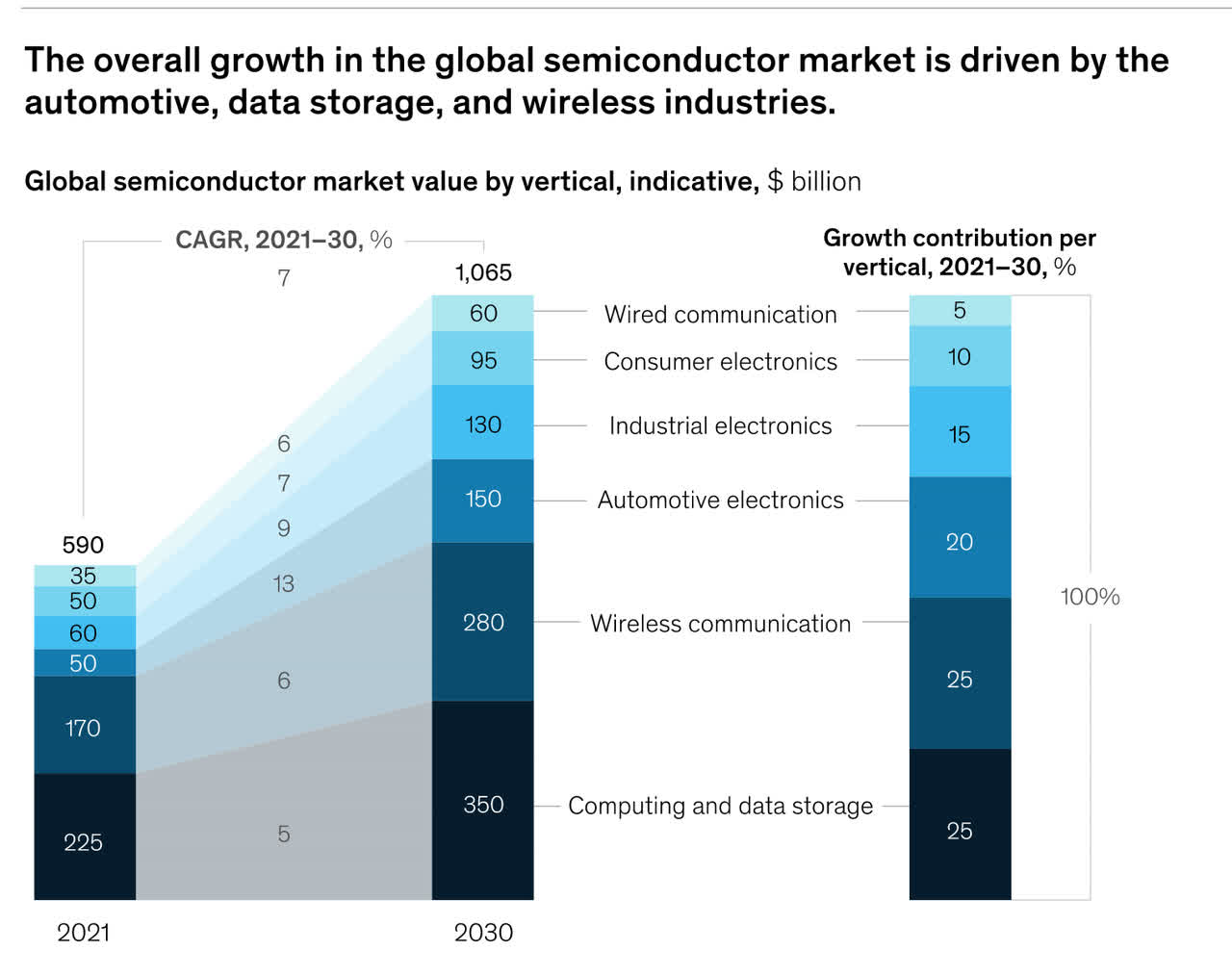

With its broad and diverse exposure, investing in TXN is equivalent to investing in the semiconductor industry. We are excited about TXN because it is exposed to many high-growth sectors. We strongly believe TXN's growth is tied to the industry's growth and, in turn, are optimistic about the company and the stock's performance. The following graph shows global semiconductor growth drivers.

McKinsey

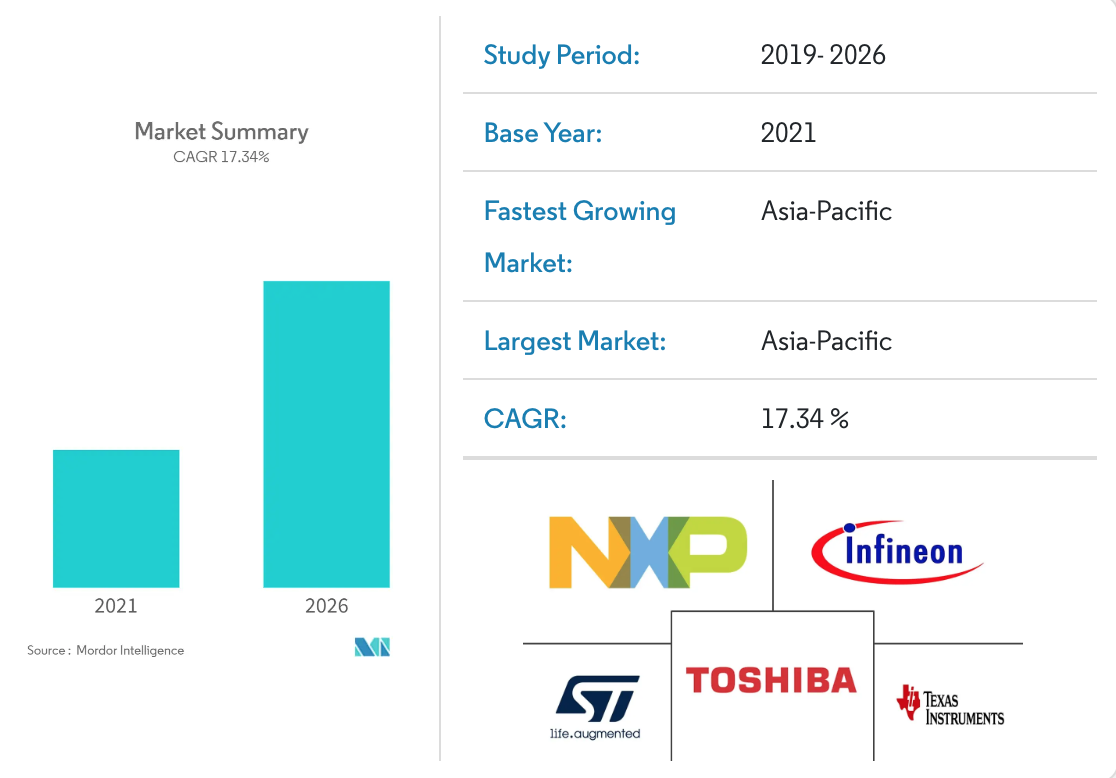

Automotive is currently the fastest-growing market, and we expect it to become an increasingly profitable segment for TXN. The following table shows the market's expected growth with TXN as a market leader. We expect automotives are on their way to being the next big thing for TXN. We believe TXN is well-equipped to cater to the growth in automotive and other markets, given its consistent focus on the industry.

Mordor Intelligence

TXN has already lowered estimates

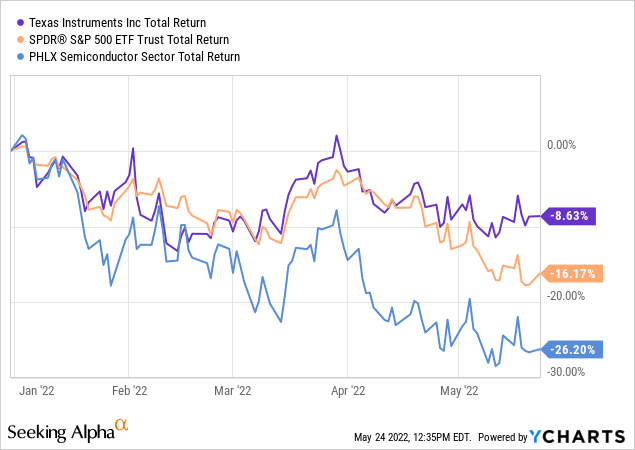

TXN is not a risk-free investment, despite the recent sell-off. Anticipating demand destruction, TXN has already lowered its forecasts for 2Q22. TXN forecasts 2Q22 revenue to be down 2 - 14% Q/Q, while competitors have not adjusted their estimates: Analog Devices (ADI)+3%; ON Semiconductor Corporation (ON) +1 - 6%; STMicroelectronics (STM) +6%; NXP Semiconductors (NXPI) +1 - 8%; Microchip Technology (MCHP) +4 - 8%; Infineon Technologies (OTCQX:IFNNY) (OTCQX:IFNNF) +3%. We believe TXN stock has a lower downside than other semiconductor stocks, given that it already lowered estimates. The following graph shows TXN outperforming industry indices:

YCharts

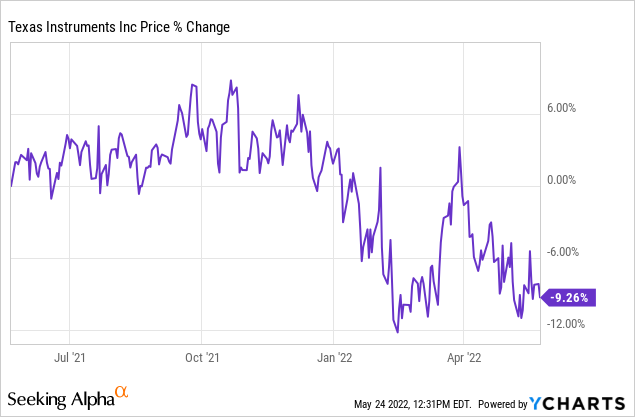

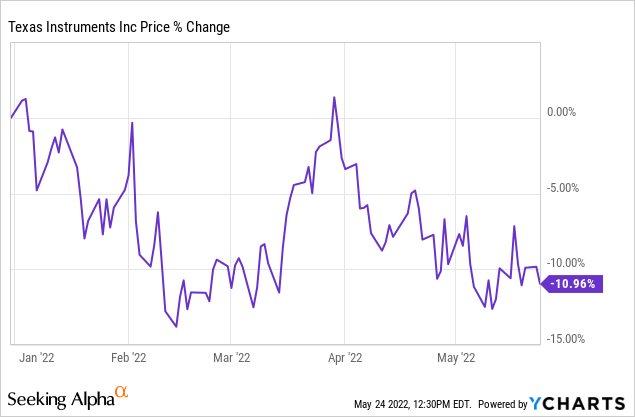

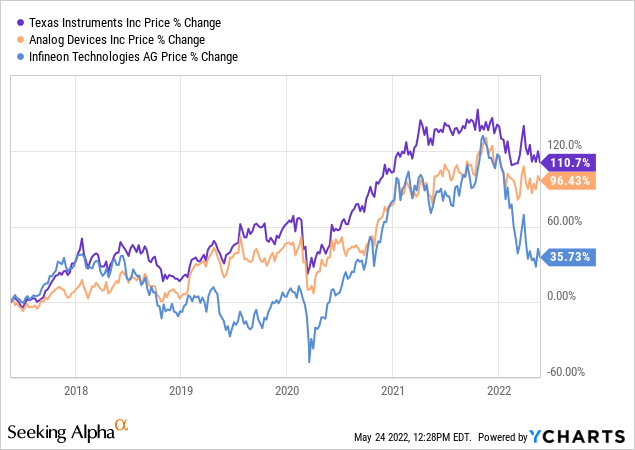

Due to the recent supply chain challenges, we believe TXN revenue is at risk of double ordering from customers. TXN has a large footprint in China. The company's exposure to China-based customers represents around 25% of its revenue. We remain concerned about the short-term impact of the Chinese lockdown on demand. Nevertheless, we do not believe the restrictions will have a long-term material impact on the company. We believe the company's size and market exposure will balance the ups and downs in demand and sustain the company's position in the industry. The following charts illustrate TXN's recent stock performance

YCharts YCharts YCharts

Stock Performance

TI stock had a decent run over the past decade. The stock rose 111% over the last five years compared to competitors Analog Devices at 96% and Infineon Tech at 36% during the same period. Like most of its peer group, TXN stock surged around March 2020 with the spread of the pandemic. Yet over the past year, the stock dropped 9%. The stock is also down 11% on YTD. We believe the downward draft is due to demand normalization and the global semiconductor market sell-off that is not specific to TXN. We believe long-term Industrial and Automotive demand will carry the stock in the coming quarters, and we recommend TXN as a long-term investment.

Valuation

TXN is not a cheap stock, trading at around $167. However, the stock is still not wildly expensive and produces a lot of cash flow. On the P/E basis, TXN is trading at 18.5x C2023 EPS of $9 compared to 14.3x for the semiconductor peer group. The stock is trading at 7.8x EV/C2023 sales versus the peer group average of 4.6x. Adjusted for growth, TXN is trading at 2.9x C2023 compared to the group average of 0.7x. The following chart illustrates the semiconductor peer group valuation table.

Refinitiv

Word on Wall Street

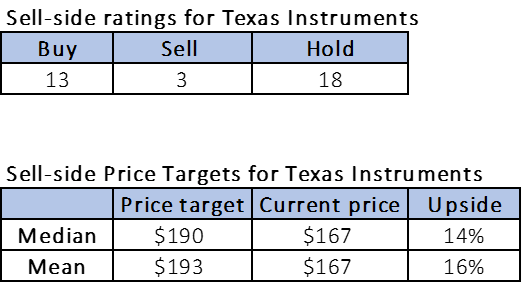

The overall market sentiment on TXN is a hold. Out of the 34 analysts, 13 are buy-rated, three our sell-rated, and the remaining 18 are hold-rated. TXN is currently trading at around $167. The sell-side median price target is $190, and the mean is $193, for an upside of 14-16%. The following chart indicates TXN sell-side ratings and price targets:

Refinitiv

What to do with the stock

TXN is not for short-term investors; it's for the long-term investor who wants in on the semiconductor industry. TXN is one of the biggest suppliers of analog and embedded processing, and we believe the company's best days are still ahead of it. In our opinion, TXN is doing everything right to prepare for better days by capitalizing on high-margin Automotive and industrial verticals and switching to cost-efficient 300 mm manufacturing fabs. We believe the company offers exposure to the semiconductor industry with limited downside. We recommend investors buy TXN for market exposure, size, and long-term potential.